Nasdaq

Nasdaq 华尔街日报

华尔街日报Imperial Oil Limited's (TSE:IMO) Popularity With Investors Is Under Threat From Overpricing

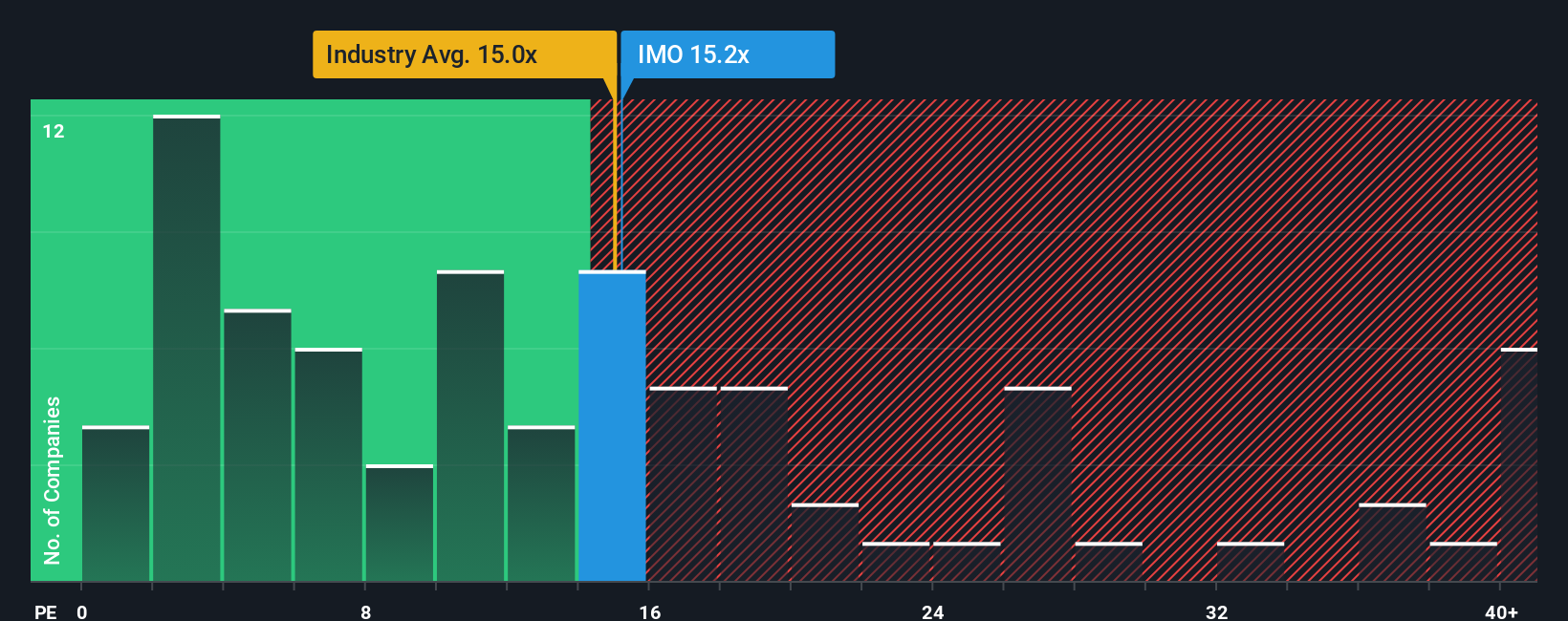

It's not a stretch to say that Imperial Oil Limited's (TSE:IMO) price-to-earnings (or "P/E") ratio of 15.2x right now seems quite "middle-of-the-road" compared to the market in Canada, where the median P/E ratio is around 16x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

While the market has experienced earnings growth lately, Imperial Oil's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

View our latest analysis for Imperial Oil

How Is Imperial Oil's Growth Trending?

The only time you'd be comfortable seeing a P/E like Imperial Oil's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered a frustrating 14% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 17% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Shifting to the future, estimates from the eight analysts covering the company suggest earnings should grow by 1.7% per year over the next three years. That's shaping up to be materially lower than the 11% each year growth forecast for the broader market.

With this information, we find it interesting that Imperial Oil is trading at a fairly similar P/E to the market. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Imperial Oil's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Imperial Oil's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

You always need to take note of risks, for example - Imperial Oil has 1 warning sign we think you should be aware of.

If these risks are making you reconsider your opinion on Imperial Oil, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.