Nasdaq

Nasdaq 华尔街日报

华尔街日报PSQ Holdings, Inc. (NYSE:PSQH) May Have Run Too Fast Too Soon With Recent 27% Price Plummet

Unfortunately for some shareholders, the PSQ Holdings, Inc. (NYSE:PSQH) share price has dived 27% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 78% share price decline.

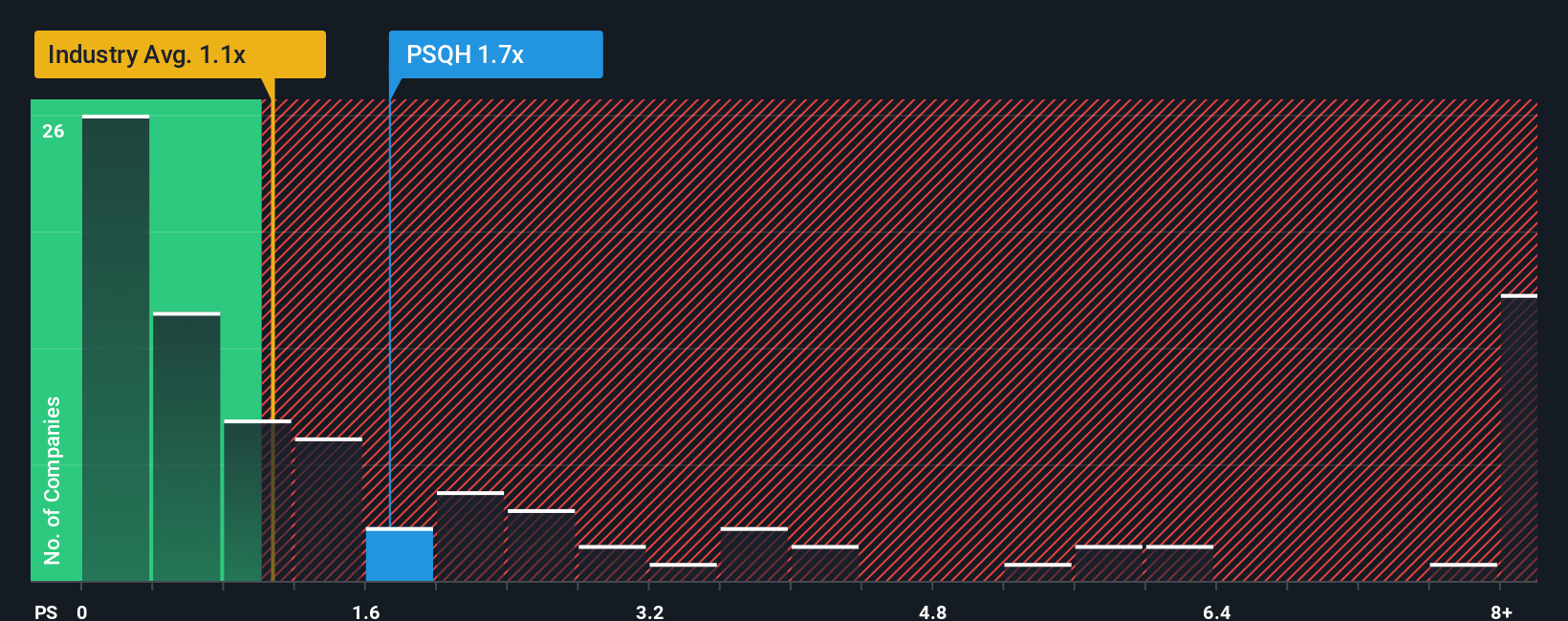

Although its price has dipped substantially, given close to half the companies operating in the United States' Interactive Media and Services industry have price-to-sales ratios (or "P/S") below 1.1x, you may still consider PSQ Holdings as a stock to potentially avoid with its 1.7x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

View our latest analysis for PSQ Holdings

How PSQ Holdings Has Been Performing

With revenue growth that's superior to most other companies of late, PSQ Holdings has been doing relatively well. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on PSQ Holdings will help you uncover what's on the horizon.How Is PSQ Holdings' Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as PSQ Holdings' is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company grew revenue by an impressive 196% last year. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 1.1% during the coming year according to the two analysts following the company. That's shaping up to be materially lower than the 16% growth forecast for the broader industry.

With this information, we find it concerning that PSQ Holdings is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

Despite the recent share price weakness, PSQ Holdings' P/S remains higher than most other companies in the industry. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Despite analysts forecasting some poorer-than-industry revenue growth figures for PSQ Holdings, this doesn't appear to be impacting the P/S in the slightest. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You always need to take note of risks, for example - PSQ Holdings has 4 warning signs we think you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.