Nasdaq

Nasdaq 华尔街日报

华尔街日报3 Asian Dividend Stocks Yielding Up To 4.7%

As Asian markets experience fluctuations driven by global economic shifts and local policy changes, investors are increasingly looking towards dividend stocks as a source of stable income. In this dynamic environment, identifying stocks with reliable dividend yields can be a prudent strategy for those seeking to balance potential market volatility with consistent returns.

Top 10 Dividend Stocks In Asia

| Name | Dividend Yield | Dividend Rating |

| Yamato Kogyo (TSE:5444) | 3.74% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 5.42% | ★★★★★★ |

| Torigoe (TSE:2009) | 4.15% | ★★★★★★ |

| NCD (TSE:4783) | 3.99% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.00% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 4.21% | ★★★★★★ |

| Changjiang Publishing & MediaLtd (SHSE:600757) | 4.62% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.86% | ★★★★★★ |

| Business Brain Showa-Ota (TSE:9658) | 3.74% | ★★★★★★ |

| Binggrae (KOSE:A005180) | 4.43% | ★★★★★★ |

Click here to see the full list of 1023 stocks from our Top Asian Dividend Stocks screener.

Let's uncover some gems from our specialized screener.

Mega Lifesciences (SET:MEGA)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Mega Lifesciences Public Company Limited, along with its subsidiaries, is involved in the manufacturing and sale of health food supplements, pharmaceuticals, over-the-counter products, herbal products, vitamins, and fast-moving consumer goods across Southeast Asia and Sub-Saharan Africa; it has a market cap of approximately THB29.21 billion.

Operations: Mega Lifesciences generates revenue through its Brands segment (THB8.64 billion), Distribution segment (THB5.24 billion), and Original Equipment Manufacture (OEM) segment (THB284.99 million).

Dividend Yield: 4.8%

Mega Lifesciences' dividend payout is sustainable, with a payout ratio of 70.7% covered by earnings and a cash payout ratio of 69%. However, its dividend yield of 4.78% is below the top tier in Thailand's market. Despite an increase in dividends over the past decade, payments have been volatile. Recent earnings show improved net income for Q3 at THB 494.19 million but a slight decline for the nine months period compared to last year.

- Get an in-depth perspective on Mega Lifesciences' performance by reading our dividend report here.

- Our comprehensive valuation report raises the possibility that Mega Lifesciences is priced lower than what may be justified by its financials.

Kita-Nippon Bank (TSE:8551)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: The Kita-Nippon Bank, Ltd., along with its subsidiaries, offers commercial banking products and services in Japan and has a market capitalization of ¥37.59 billion.

Operations: Kita-Nippon Bank's revenue segments include ¥23.76 billion from Banking, ¥3.58 billion from Leasing Business, and ¥672 million from Credit Card Business and Credit Guarantee Business.

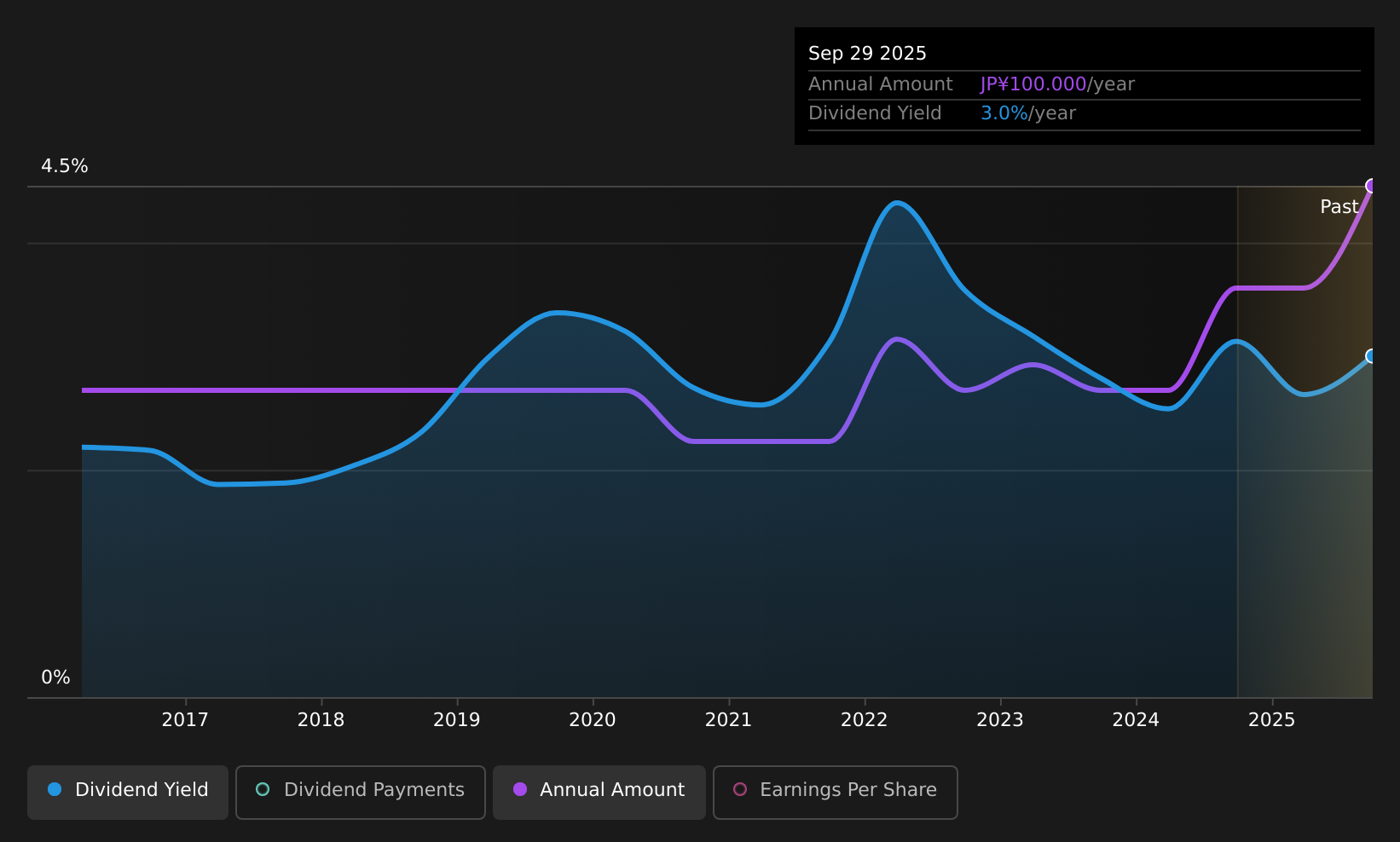

Dividend Yield: 3.7%

Kita-Nippon Bank's dividend yield of 3.72% is competitive in Japan's market, with a low payout ratio of 31.3%, indicating dividends are well covered by earnings. However, the bank's dividend history shows volatility, though recent increases suggest a positive trend. The bank has completed a share buyback worth ¥499.67 million to enhance shareholder returns and revised its annual dividend forecast to ¥84 per share, reflecting an improved shareholder return policy aiming for a higher payout ratio by 2030.

- Take a closer look at Kita-Nippon Bank's potential here in our dividend report.

- Our valuation report unveils the possibility Kita-Nippon Bank's shares may be trading at a premium.

Konoike TransportLtd (TSE:9025)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Konoike Transport Co., Ltd. operates in the logistics sector both within Japan and internationally, with a market cap of ¥174.17 billion.

Operations: Konoike Transport Co., Ltd.'s revenue is derived from three main segments: Domestic Logistics Business at ¥58.66 billion, Integrated Solutions Business at ¥225.66 billion, and International Logistics Business at ¥73.17 billion.

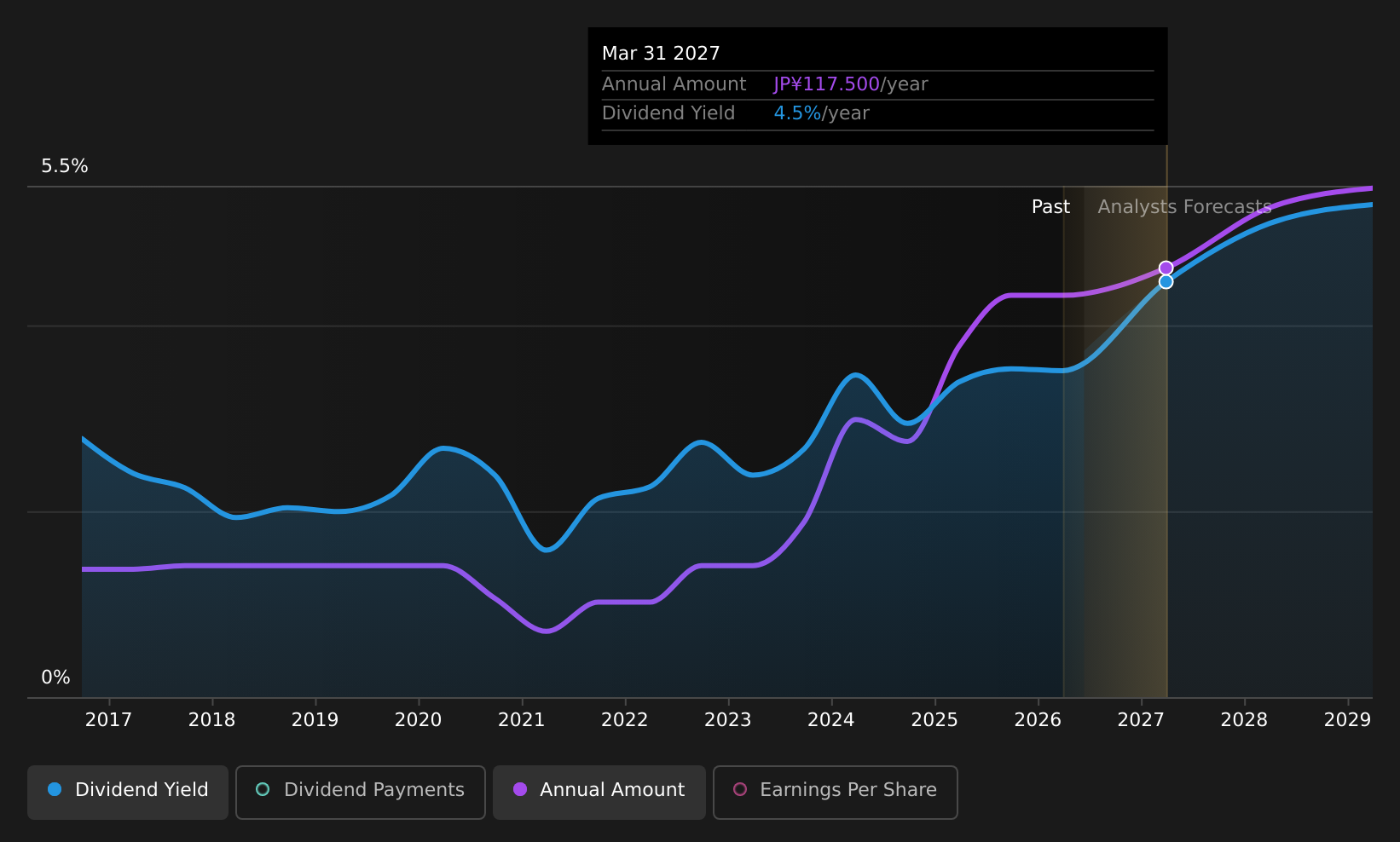

Dividend Yield: 3.4%

Konoike Transport's dividends have been volatile over the past decade, despite recent increases. The dividend is well-covered by earnings and cash flows, with a payout ratio of 49.4% and a cash payout ratio of 57.7%. Currently trading below estimated fair value, analysts anticipate stock price growth. Recent guidance revised net sales downward but increased operating profit expectations; the company announced a significant dividend increase to ¥55 per share for Q2 FY2026, payable December 1, 2025.

- Click here to discover the nuances of Konoike TransportLtd with our detailed analytical dividend report.

- In light of our recent valuation report, it seems possible that Konoike TransportLtd is trading behind its estimated value.

Next Steps

- Delve into our full catalog of 1023 Top Asian Dividend Stocks here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com