Nasdaq

Nasdaq 华尔街日报

华尔街日报Is Vistra Stock a Buy Now?

Key Points

Vistra shares have surged as investors price in the rising energy needs from data centers.

As a merchant power producer, Vistra sells electricity directly into competitive markets.

Vistra trades at a premium valuation, but analysts project strong growth in the years ahead.

In recent years, Vistra (NYSE: VST) has evolved from a traditional utility to a player in the development of artificial intelligence (AI) infrastructure. The stock has surged 321% since the start of 2024 as investors have piled into it due to its ability to meet the growing energy needs of power-hungry data centers.

As an independent power producer, Vistra has secured predictable revenue while leaving open the possibility of upside in the years ahead. However, investors must also contend with the fact that the utility stock has gotten quite expensive.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

If you're considering an investment in Vistra, here's what you should know first.

Vistra's merchant power business model

Vistra operates as a merchant power company, selling electricity directly into competitive wholesale markets across 18 states and Washington, D.C., on a short-term basis rather than through power purchase agreements. The utility provider serves 5 million residential, commercial, and industrial customers.

As a wholesale provider, Vistra doesn't rely on any single power plant, geographic market, or customer segment. This enables Vistra to combine its retail business with its generation fleet and wholesale commodity risk-management capabilities through the use of hedging derivatives. In other words, its business model helps mitigate the impact of commodity price movements and supports cash flow stability.

Image source: Getty Images.

As of Oct. 31, Vistra had hedged approximately 96% of its expected generation volumes for 2026 and approximately 70% for 2027. In other words, Vistra has committed to pricing nearly all of its output next year, locking in revenue and reducing its exposure to volatility in natural gas and electricity prices. By leaving 30% of its 2027 generation volumes "open," it locks in a large portion of revenue while giving it upside potential if energy prices spike.

This business model positions Vistra to benefit from rising wholesale power prices, particularly in regions like the Northeast and Midwest U.S., where supply constraints and surging demand are reshaping dynamics across the energy complex.

Vistra is building on its strong position

Wholesale electricity prices are highly volatile due to supply and demand imbalances, especially in day-ahead and spot markets. In the Pennsylvania-New Jersey-Maryland (PJM) market, one of the regions where Vistra provides energy, markets remain tight, with wholesale power prices trending upward.

Meanwhile, PJM and other markets it serves face a sluggish pace of new power plant construction, regulatory bottlenecks, and retirements of older coal and nuclear facilities. Supply chain constraints and labor shortages have reduced equipment availability and increased lead times for materials required for new construction and maintenance.

To ensure capacity and expand its reach, Vistra acquired seven natural gas plants from Lotus Infrastructure Partners for $1.9 million. This significantly expands its reach in high-demand regions, such as PJM, New England, and California. Natural gas is compelling because it provides dispatchable power that can ramp up instantly to stabilize the grid when weather-dependent wind and solar generation drops.

Additionally, Vistra is securing major deals to lock in long-term visibility into revenue. In September, it signed a 20-year power purchase agreement with a "large, investment-grade" company for 1,200 MW of carbon-free power. This deal converts a significant portion of its nuclear output into a long-term, predictable revenue stream.

Vistra is expensive. Is the stock a buy?

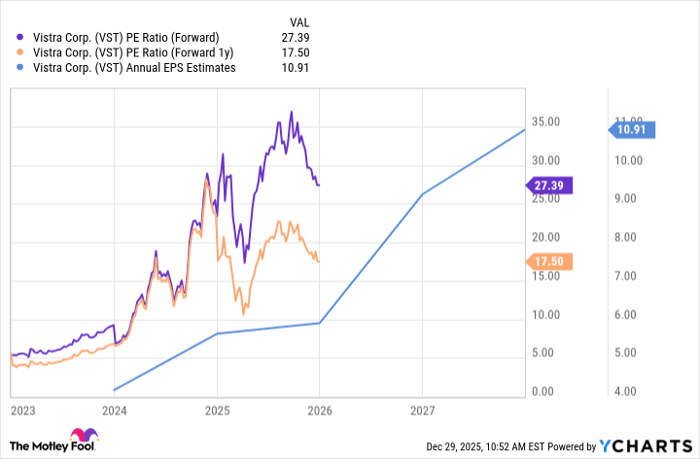

Vistra has surged over the last couple of years and now trades at a premium valuation with the stock priced at 27.4 times this year's projected earnings, which is high for a utility provider.

VST PE Ratio (Forward) data by YCharts

However, analysts project robust growth in 2026 and 2027, with earnings per share projected to surge 68% and 22%, respectively. Using those forward earnings per share estimates, Vistra is priced at 17.5 times its projected earnings next year and 14.8 times its projected 2027 earnings.

Vistra stock is on the pricey side, but it has declined 26% from its September peak. If you believe in the opportunities ahead, driven by energy demand from the data center buildout and the proliferation of AI, Vistra is one stock poised to benefit.

Courtney Carlsen has positions in Vistra. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.