Nasdaq

Nasdaq 华尔街日报

华尔街日报Middle Eastern Dividend Stocks Featuring Abu Dhabi Islamic Bank PJSC And Two More

As geopolitical tensions between major Gulf nations like Saudi Arabia and the UAE escalate, many Middle Eastern stock markets have experienced a downturn, with indices in Dubai and Abu Dhabi showing notable declines. In such a volatile environment, dividend stocks can offer investors stability and potential income streams, making them an appealing choice for those looking to navigate uncertain market conditions.

Top 10 Dividend Stocks In The Middle East

| Name | Dividend Yield | Dividend Rating |

| Yeni Gimat Gayrimenkul Yatirim Ortakligi (IBSE:YGGYO) | 5.52% | ★★★★★★ |

| Saudi Awwal Bank (SASE:1060) | 6.23% | ★★★★★☆ |

| Riyad Bank (SASE:1010) | 6.44% | ★★★★★☆ |

| National General Insurance (P.J.S.C.) (DFM:NGI) | 7.64% | ★★★★★☆ |

| Emaar Properties PJSC (DFM:EMAAR) | 7.19% | ★★★★★☆ |

| Computer Direct Group (TASE:CMDR) | 7.24% | ★★★★★☆ |

| Commercial Bank of Dubai PSC (DFM:CBD) | 5.46% | ★★★★★☆ |

| Banque Saudi Fransi (SASE:1050) | 6.49% | ★★★★★☆ |

| Arab National Bank (SASE:1080) | 6.05% | ★★★★★☆ |

| Anadolu Hayat Emeklilik Anonim Sirketi (IBSE:ANHYT) | 5.93% | ★★★★★☆ |

Click here to see the full list of 64 stocks from our Top Middle Eastern Dividend Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

Abu Dhabi Islamic Bank PJSC (ADX:ADIB)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Abu Dhabi Islamic Bank PJSC offers banking, financing, and investing services across the United Arab Emirates, the Middle East, and internationally with a market cap of AED75.11 billion.

Operations: Abu Dhabi Islamic Bank PJSC generates revenue from several segments, including Treasury (AED597.70 million), Real Estate (AED99.17 million), Private Banking (AED253.06 million), Global Retail Banking (AED5.45 billion), Global Wholesale Banking (AED2.01 billion), and Associates & Subsidiaries (AED1.71 billion).

Dividend Yield: 4%

Abu Dhabi Islamic Bank PJSC has experienced volatile dividend payments over the past decade, with a current yield of 4.03%, which is lower than the top quartile in the AE market. Despite this, dividends are well covered by earnings due to a low payout ratio of 50%. Recent financials show strong growth in net income and interest income, indicating potential stability. However, challenges include a high level of bad loans at 2.8% and historically unreliable dividend growth.

- Delve into the full analysis dividend report here for a deeper understanding of Abu Dhabi Islamic Bank PJSC.

- Our valuation report unveils the possibility Abu Dhabi Islamic Bank PJSC's shares may be trading at a premium.

National Bank of Ras Al-Khaimah (P.S.C.) (ADX:RAKBANK)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: The National Bank of Ras Al-Khaimah (P.S.C.) offers retail, Islamic, and commercial banking services to individuals and businesses in the UAE, with a market cap of AED16.92 billion.

Operations: The National Bank of Ras Al-Khaimah (P.S.C.) generates its revenue from Retail Banking (AED1.35 billion), Business Banking (AED1.82 billion), and Wholesale Banking (AED1.41 billion) segments in the UAE.

Dividend Yield: 5.9%

National Bank of Ras Al-Khaimah (P.S.C.) offers a dividend yield of 5.95%, below the top quartile in the AE market. Despite a low payout ratio of 40.9%, dividends have been volatile over the past decade, though they remain covered by earnings and are forecast to stay sustainable with a future payout ratio of 49.1%. Recent financials reveal growth in net income and interest income, but upcoming business line disposals could impact financial stability and share price.

- Click here and access our complete dividend analysis report to understand the dynamics of National Bank of Ras Al-Khaimah (P.S.C.).

- Our valuation report here indicates National Bank of Ras Al-Khaimah (P.S.C.) may be overvalued.

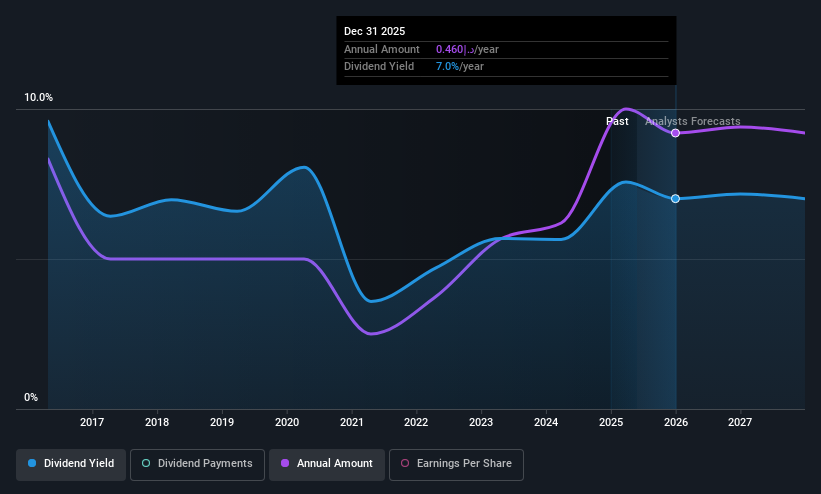

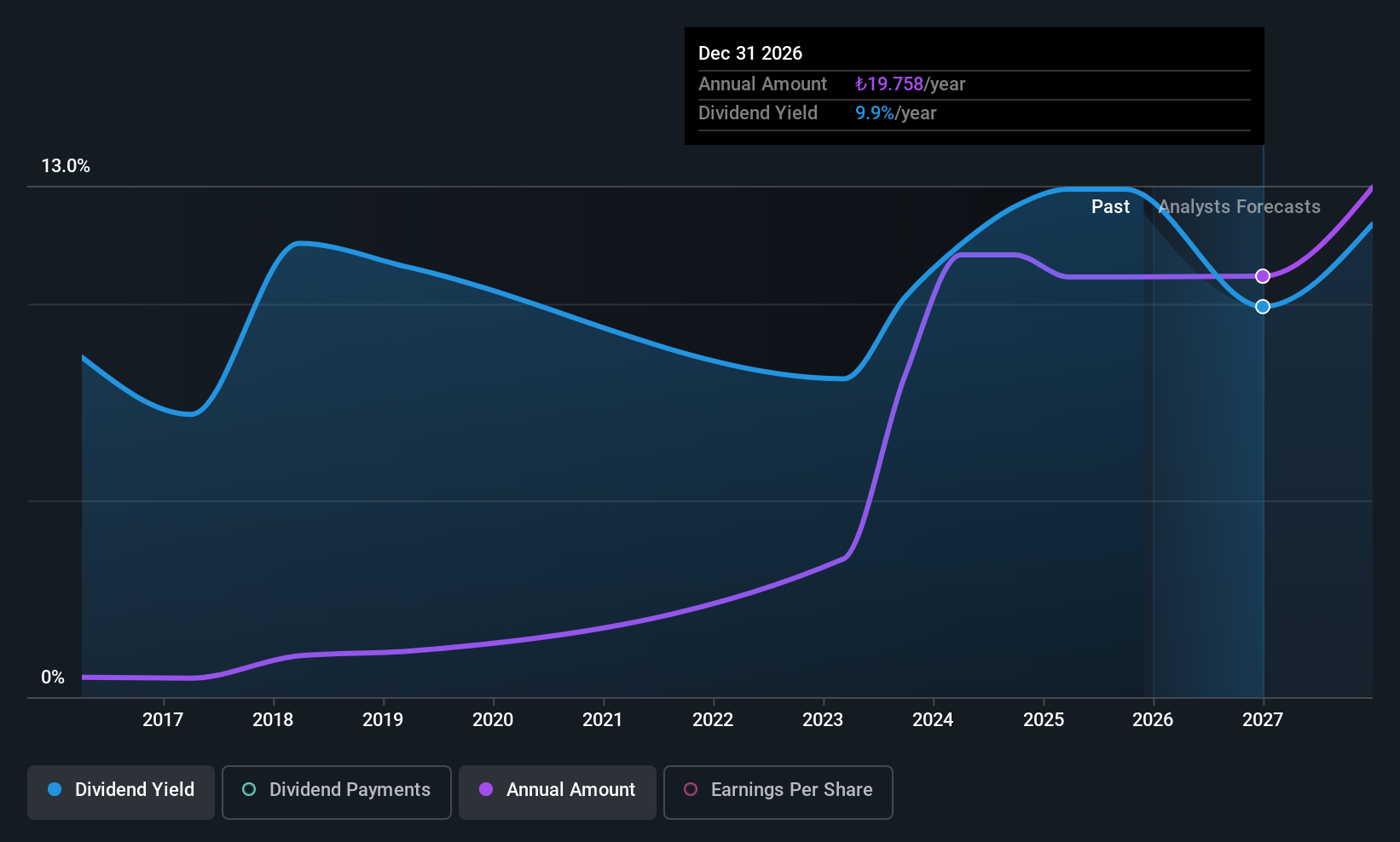

Türkiye Petrol Rafinerileri (IBSE:TUPRS)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Türkiye Petrol Rafinerileri A.S., along with its subsidiaries, operates in the refining of crude oil, petroleum, and chemical products both in Turkey and internationally, with a market cap of TRY359.15 billion.

Operations: Türkiye Petrol Rafinerileri A.S. generates revenue primarily from its refining segment, which accounts for TRY601.58 billion, and also from its electric segment, contributing TRY8.28 billion.

Dividend Yield: 10.6%

Türkiye Petrol Rafinerileri's dividend yield of 10.58% ranks in the top quartile of the Turkish market, supported by a payout ratio of 68%, indicating dividends are covered by earnings. Despite recent earnings growth, with net income rising to TRY 12.16 billion in Q3 2025, dividends have been volatile over the past decade. The cash payout ratio at 88.6% suggests coverage by cash flows, though profit margins have decreased from last year’s levels.

- Click to explore a detailed breakdown of our findings in Türkiye Petrol Rafinerileri's dividend report.

- The valuation report we've compiled suggests that Türkiye Petrol Rafinerileri's current price could be inflated.

Summing It All Up

- Explore the 64 names from our Top Middle Eastern Dividend Stocks screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com