Nasdaq

Nasdaq 华尔街日报

华尔街日报Getting In Cheap On Super Group (SGHC) Limited (NYSE:SGHC) Is Unlikely

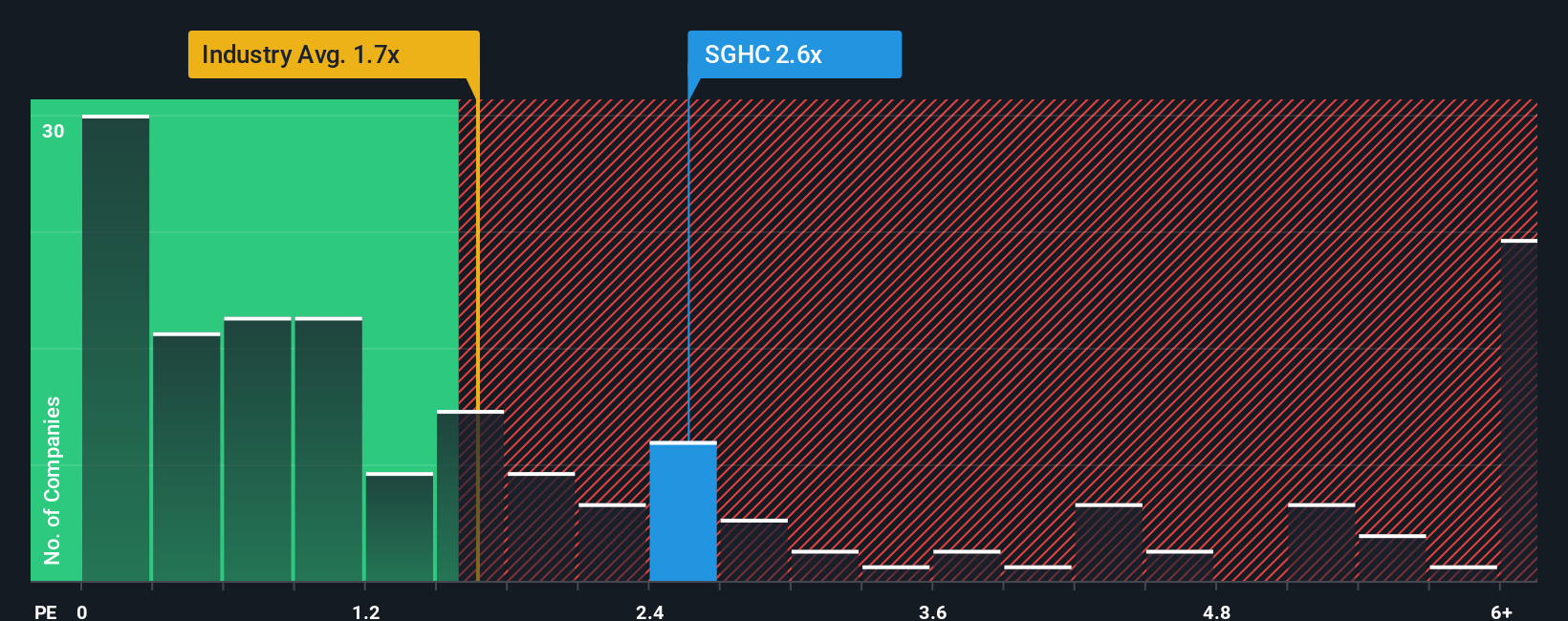

When you see that almost half of the companies in the Hospitality industry in the United States have price-to-sales ratios (or "P/S") below 1.7x, Super Group (SGHC) Limited (NYSE:SGHC) looks to be giving off some sell signals with its 2.6x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

See our latest analysis for Super Group (SGHC)

How Has Super Group (SGHC) Performed Recently?

Recent times have been advantageous for Super Group (SGHC) as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Super Group (SGHC)'s future stacks up against the industry? In that case, our free report is a great place to start.How Is Super Group (SGHC)'s Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as Super Group (SGHC)'s is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company grew revenue by an impressive 35% last year. The strong recent performance means it was also able to grow revenue by 83% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 8.7% per annum as estimated by the eight analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 14% per year, which is noticeably more attractive.

With this in consideration, we believe it doesn't make sense that Super Group (SGHC)'s P/S is outpacing its industry peers. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Despite analysts forecasting some poorer-than-industry revenue growth figures for Super Group (SGHC), this doesn't appear to be impacting the P/S in the slightest. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. At these price levels, investors should remain cautious, particularly if things don't improve.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Super Group (SGHC) with six simple checks will allow you to discover any risks that could be an issue.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.