Nasdaq

Nasdaq 华尔街日报

华尔街日报Take Care Before Diving Into The Deep End On Ushanti Colour Chem Limited (NSE:UCL)

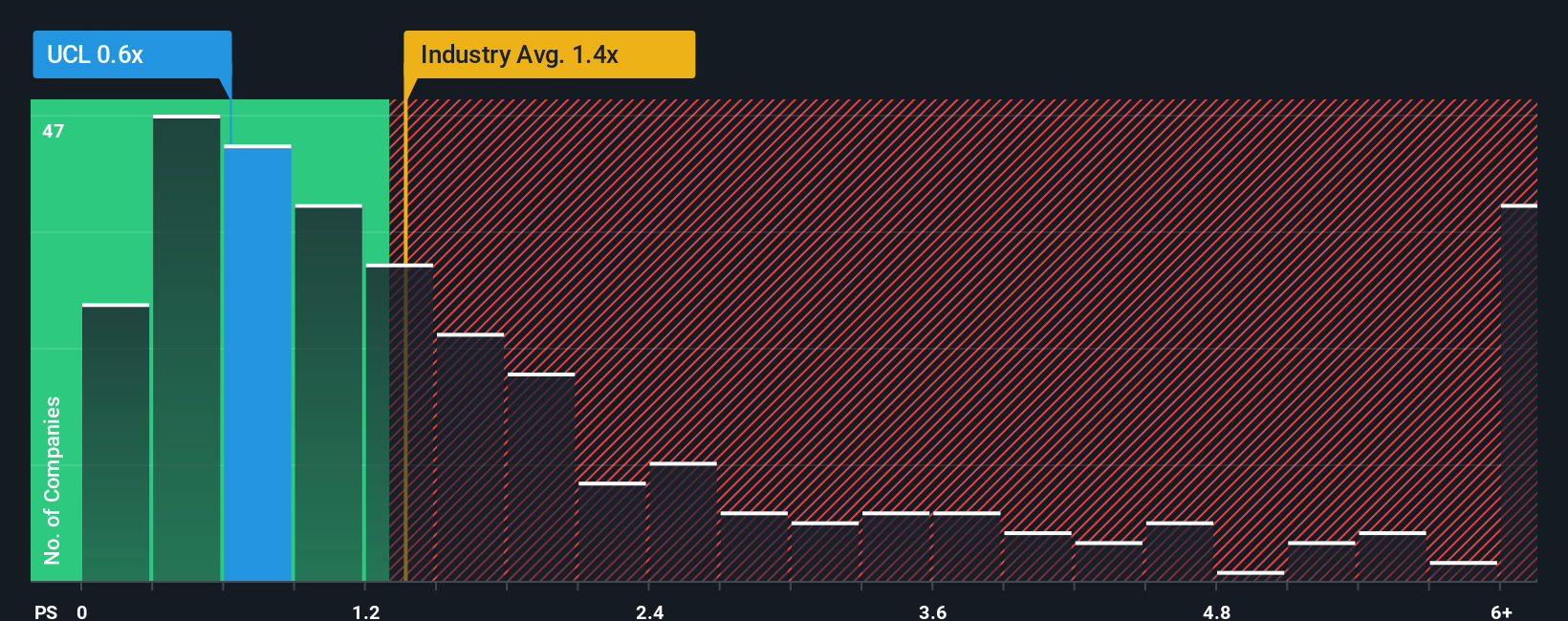

Ushanti Colour Chem Limited's (NSE:UCL) price-to-sales (or "P/S") ratio of 0.6x may look like a pretty appealing investment opportunity when you consider close to half the companies in the Chemicals industry in India have P/S ratios greater than 1.4x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Ushanti Colour Chem

What Does Ushanti Colour Chem's Recent Performance Look Like?

Ushanti Colour Chem certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. One possibility is that the P/S ratio is low because investors think this strong revenue growth might actually underperform the broader industry in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Although there are no analyst estimates available for Ushanti Colour Chem, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Ushanti Colour Chem?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Ushanti Colour Chem's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 44%. The latest three year period has also seen an excellent 79% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 15% shows it's noticeably more attractive.

With this information, we find it odd that Ushanti Colour Chem is trading at a P/S lower than the industry. It looks like most investors are not convinced the company can maintain its recent growth rates.

What We Can Learn From Ushanti Colour Chem's P/S?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Ushanti Colour Chem revealed its three-year revenue trends aren't boosting its P/S anywhere near as much as we would have predicted, given they look better than current industry expectations. Potential investors that are sceptical over continued revenue performance may be preventing the P/S ratio from matching previous strong performance. It appears many are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

Having said that, be aware Ushanti Colour Chem is showing 4 warning signs in our investment analysis, you should know about.

If you're unsure about the strength of Ushanti Colour Chem's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.