Nasdaq

Nasdaq 华尔街日报

华尔街日报Zoom (TSE:6694) Is Increasing Its Dividend To ¥32.00

The board of Zoom Corporation (TSE:6694) has announced that it will be paying its dividend of ¥32.00 on the 30th of March, an increased payment from last year's comparable dividend. This makes the dividend yield 4.8%, which is above the industry average.

Zoom's Distributions May Be Difficult To Sustain

A big dividend yield for a few years doesn't mean much if it can't be sustained. Zoom is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. We generally think that cash flow is more important than accounting measures of profit, so we are fairly comfortable with the dividend at this level.

EPS has fallen by an average of 52.1% in the past, so this could continue over the next year. While this means that the company will be unprofitable, we generally believe cash flows are more important, and the current cash payout ratio is quite healthy, which gives us comfort.

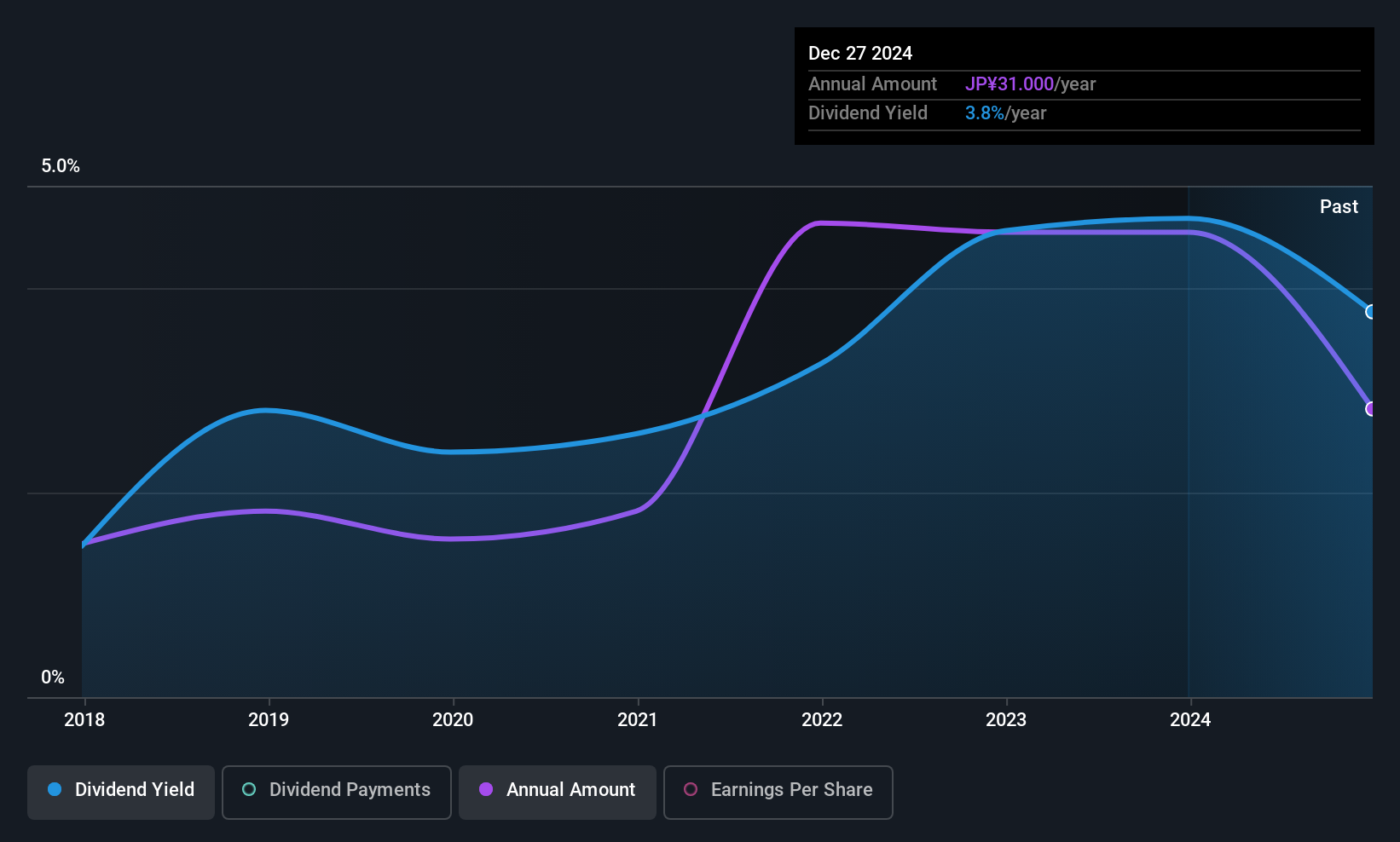

See our latest analysis for Zoom

Zoom's Dividend Has Lacked Consistency

Looking back, Zoom's dividend hasn't been particularly consistent. This suggests that the dividend might not be the most reliable. Since 2016, the dividend has gone from ¥16.50 total annually to ¥32.00. This works out to be a compound annual growth rate (CAGR) of approximately 7.6% a year over that time. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Zoom might have put its house in order since then, but we remain cautious.

The Dividend Has Limited Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Over the past five years, it looks as though Zoom's EPS has declined at around 52% a year. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future.

The Dividend Could Prove To Be Unreliable

Overall, we always like to see the dividend being raised, but we don't think Zoom will make a great income stock. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 4 warning signs for Zoom (of which 2 are a bit concerning!) you should know about. Is Zoom not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.