Nasdaq

Nasdaq 华尔街日报

华尔街日报Check Point (CHKP): Assessing Valuation After Steady Outperformance of Cybersecurity Peers

Check Point Software Technologies (CHKP) has been quietly outpacing the broader cybersecurity space this month, with shares up about 3% despite a mixed backdrop for tech and security names.

See our latest analysis for Check Point Software Technologies.

That steady 2.13% year to date share price return, alongside a 50.92% three year total shareholder return, suggests Check Point’s cybersecurity story is more about enduring compounding than short term excitement. Momentum has cooled slightly after a strong multi year run.

If Check Point’s resilient performance has you thinking about where else growth and innovation might show up next, it is worth exploring high growth tech and AI stocks for more potential standouts in this space.

With shares not far off record levels yet trading at a double digit discount to analyst targets, despite modest top line growth and softer earnings, the key question now is whether Check Point is undervalued or if the market is already pricing in its next leg of growth.

Most Popular Narrative: 17.5% Undervalued

With Check Point shares last closing at $188.52 versus a narrative fair value of about $228.40, the story leans toward steady compounding at a discounted price.

The Infinity platform continues to gain traction, with strong double digit revenue growth and increased customer adoption, now accounting for over 15% of total revenue. This supports expectations for revenue growth through enhanced customer retention and cross-selling opportunities.

Want to see what kind of revenue climb, margin resilience, and future earnings multiple are baked into this outlook? The valuation hinges on a surprisingly assertive growth runway and a premium style earnings profile that still sits below many software peers. Curious which assumptions really drive that gap between today’s price and the projected fair value? Dive in to unpack the full narrative model.

Result: Fair Value of $228.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside relies on billings momentum proving durable, with competitive SASE and AI spend or macro driven deal delays quickly challenging the current growth narrative.

Find out about the key risks to this Check Point Software Technologies narrative.

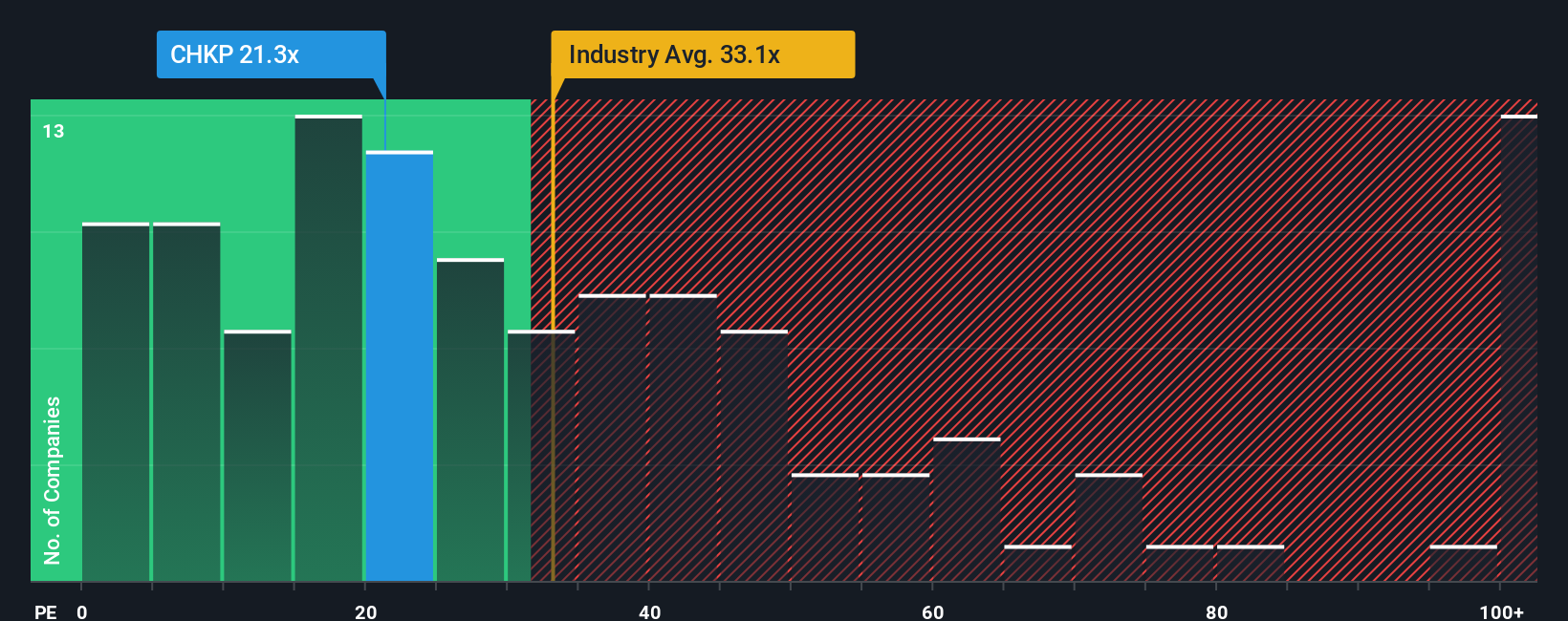

Another View, Market Multiple Versus Fair Ratio

On our numbers, Check Point trades on about 20 times earnings, well below both the US software pack at roughly 31.9 times and its own fair ratio near 25.8 times. That discount hints at opportunity, but it raises a question: is the market prudently pricing in slower growth, or simply being too cautious on quality security cash flows?

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Check Point Software Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 901 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Check Point Software Technologies Narrative

If you would rather dig into the numbers yourself and challenge this outlook, you can build a personalized Check Point view in just minutes: Do it your way.

A great starting point for your Check Point Software Technologies research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing edge?

Do not stop with just one opportunity. Use the Simply Wall Street Screener to quickly pinpoint fresh ideas that match your goals before the market moves on.

- Capture turnaround potential as you scan these 901 undervalued stocks based on cash flows. These may be mispriced by the market despite strong underlying cash flows.

- Ride the next wave of innovation by targeting these 24 AI penny stocks that are positioned at the front line of artificial intelligence growth.

- Explore potential income streams by focusing on these 10 dividend stocks with yields > 3% that may strengthen your portfolio’s yield without sacrificing quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com