Nasdaq

Nasdaq 华尔街日报

华尔街日报3 Asian Growth Companies With Insider Ownership Expecting 26% Revenue Growth

The Asian markets have been navigating a complex economic landscape, with Japan's recent interest rate hike marking the highest level in 30 years and China's mixed economic indicators highlighting ongoing growth challenges. In this environment, companies with strong insider ownership can be particularly appealing as they often signal confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| UTI (KOSDAQ:A179900) | 25% | 120.7% |

| Streamax Technology (SZSE:002970) | 32.5% | 33.1% |

| Sineng ElectricLtd (SZSE:300827) | 36% | 29.8% |

| Seers Technology (KOSDAQ:A458870) | 33.9% | 78.8% |

| Novoray (SHSE:688300) | 23.6% | 31.4% |

| Loadstar Capital K.K (TSE:3482) | 31% | 23.6% |

| Laopu Gold (SEHK:6181) | 34.8% | 34.3% |

| J&V Energy Technology (TWSE:6869) | 17.5% | 31.6% |

| Gold Circuit Electronics (TWSE:2368) | 31.4% | 37.2% |

| Fulin Precision (SZSE:300432) | 10.6% | 55.2% |

Let's uncover some gems from our specialized screener.

Smoore International Holdings (SEHK:6969)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Smoore International Holdings Limited is an investment holding company that provides vaping technology solutions, with a market cap of HK$76.31 billion.

Operations: Smoore International Holdings Limited generates revenue through its vaping technology solutions.

Insider Ownership: 39.7%

Revenue Growth Forecast: 13.6% p.a.

Smoore International Holdings demonstrates potential as a growth company with substantial insider ownership, despite facing challenges. The company's earnings are projected to grow significantly at 37.2% annually, outpacing the Hong Kong market. However, recent results show declining profit margins and net income compared to last year. Trading at 42.5% below estimated fair value suggests potential undervaluation, while revenue is expected to grow faster than the market average but slower than desired for high-growth companies.

- Navigate through the intricacies of Smoore International Holdings with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Smoore International Holdings shares in the market.

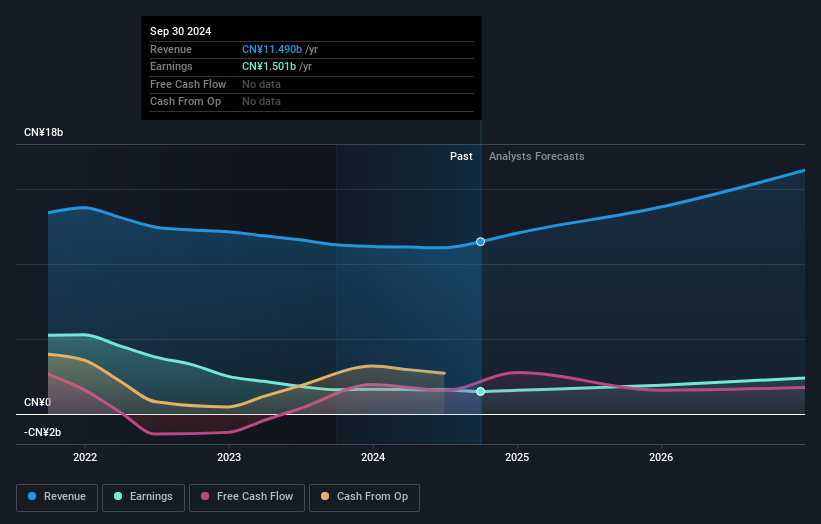

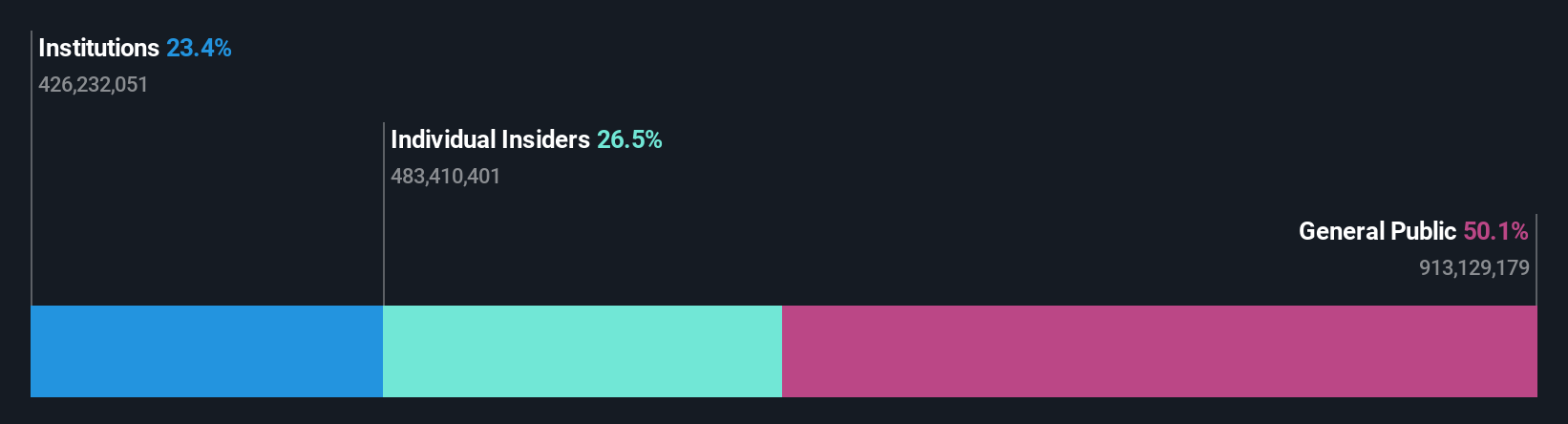

Suzhou Dongshan Precision Manufacturing (SZSE:002384)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Suzhou Dongshan Precision Manufacturing Co., Ltd. operates in the electronics manufacturing sector, focusing on precision components and assemblies, with a market cap of CN¥153.30 billion.

Operations: Suzhou Dongshan Precision Manufacturing Co., Ltd.'s revenue segments are not specified in the provided text.

Insider Ownership: 26.5%

Revenue Growth Forecast: 19.1% p.a.

Suzhou Dongshan Precision Manufacturing shows promise with high insider ownership and robust growth forecasts. Earnings are expected to grow significantly at 52.5% annually, surpassing the Chinese market average. Revenue is projected to increase by 19.1% per year, though slightly below ideal high-growth rates. Recent earnings results indicate improved performance, with net income rising to CNY 1.22 billion from CNY 1.07 billion a year ago, despite share price volatility and low future return on equity forecasts of 16.2%.

- Take a closer look at Suzhou Dongshan Precision Manufacturing's potential here in our earnings growth report.

- Our valuation report unveils the possibility Suzhou Dongshan Precision Manufacturing's shares may be trading at a premium.

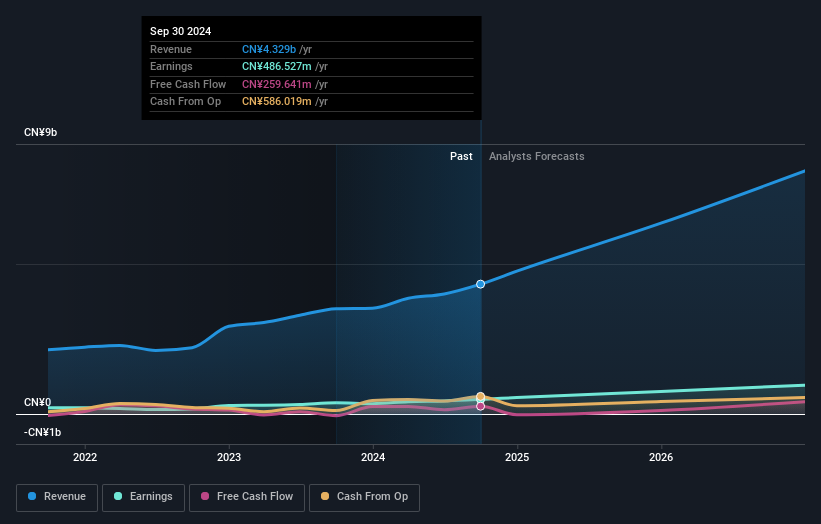

Shenzhen Envicool Technology (SZSE:002837)

Simply Wall St Growth Rating: ★★★★★★

Overview: Shenzhen Envicool Technology Co., Ltd. specializes in producing and selling temperature control and energy-saving solutions in China, with a market cap of CN¥108.56 billion.

Operations: The company's revenue from Precision Temperature Control Energy Saving Equipment is CN¥5.74 billion.

Insider Ownership: 18.1%

Revenue Growth Forecast: 26.7% p.a.

Shenzhen Envicool Technology demonstrates strong growth potential with significant insider ownership. The company reported a substantial increase in sales to CNY 4.03 billion for the first nine months of 2025, up from CNY 2.87 billion the previous year, alongside net income growth to CNY 399.07 million. Earnings and revenue are forecasted to grow significantly above market averages at rates of 30.9% and 26.7% annually, respectively, despite recent share price volatility and no recent insider trading activity noted.

- Unlock comprehensive insights into our analysis of Shenzhen Envicool Technology stock in this growth report.

- Our expertly prepared valuation report Shenzhen Envicool Technology implies its share price may be too high.

Next Steps

- Take a closer look at our Fast Growing Asian Companies With High Insider Ownership list of 631 companies by clicking here.

- Ready For A Different Approach? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com