Nasdaq

Nasdaq 华尔街日报

华尔街日报A Piece Of The Puzzle Missing From Reitar Logtech Holdings Limited's (NASDAQ:RITR) 44% Share Price Climb

Reitar Logtech Holdings Limited (NASDAQ:RITR) shareholders are no doubt pleased to see that the share price has bounced 44% in the last month, although it is still struggling to make up recently lost ground. But the last month did very little to improve the 65% share price decline over the last year.

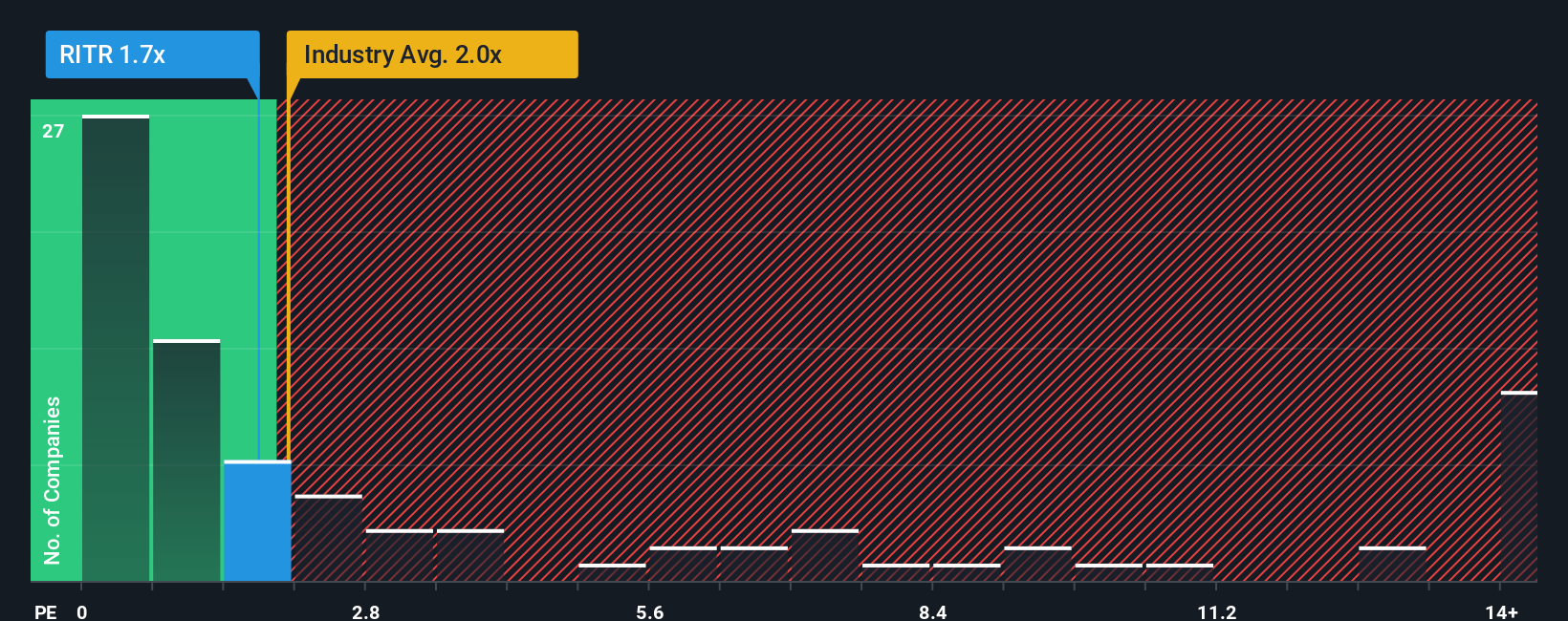

Although its price has surged higher, you could still be forgiven for feeling indifferent about Reitar Logtech Holdings' P/S ratio of 1.7x, since the median price-to-sales (or "P/S") ratio for the Real Estate industry in the United States is also close to 2x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Reitar Logtech Holdings

What Does Reitar Logtech Holdings' P/S Mean For Shareholders?

With revenue growth that's exceedingly strong of late, Reitar Logtech Holdings has been doing very well. The P/S is probably moderate because investors think this strong revenue growth might not be enough to outperform the broader industry in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Reitar Logtech Holdings' earnings, revenue and cash flow.How Is Reitar Logtech Holdings' Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Reitar Logtech Holdings' to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 50% last year. The strong recent performance means it was also able to grow revenue by 162% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

This is in contrast to the rest of the industry, which is expected to grow by 12% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's curious that Reitar Logtech Holdings' P/S sits in line with the majority of other companies. It may be that most investors are not convinced the company can maintain its recent growth rates.

What Does Reitar Logtech Holdings' P/S Mean For Investors?

Reitar Logtech Holdings appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Reitar Logtech Holdings currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

We don't want to rain on the parade too much, but we did also find 4 warning signs for Reitar Logtech Holdings (2 are a bit unpleasant!) that you need to be mindful of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.