Nasdaq

Nasdaq 华尔街日报

华尔街日报Investor Optimism Abounds HBX Group International plc (BME:HBX) But Growth Is Lacking

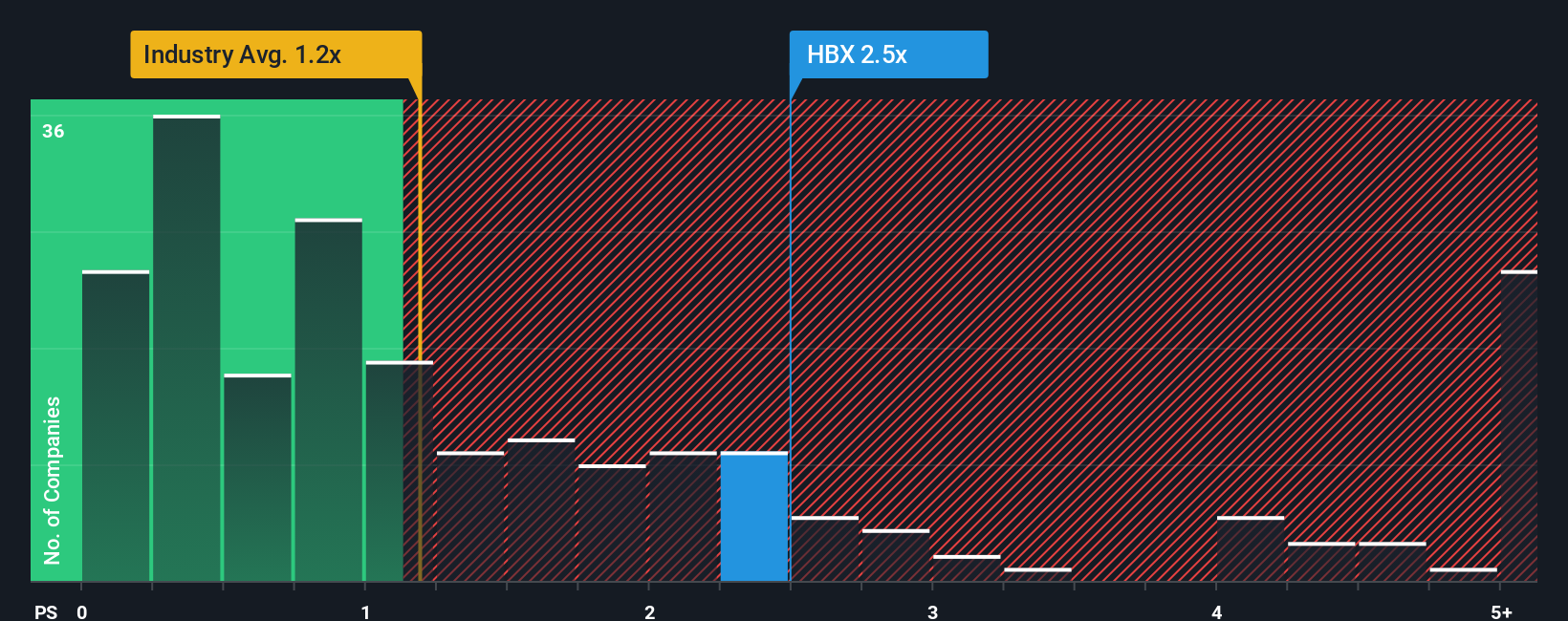

When you see that almost half of the companies in the Hospitality industry in Spain have price-to-sales ratios (or "P/S") below 1.1x, HBX Group International plc (BME:HBX) looks to be giving off some sell signals with its 2.5x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for HBX Group International

What Does HBX Group International's Recent Performance Look Like?

HBX Group International could be doing better as it's been growing revenue less than most other companies lately. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on HBX Group International.Is There Enough Revenue Growth Forecasted For HBX Group International?

There's an inherent assumption that a company should outperform the industry for P/S ratios like HBX Group International's to be considered reasonable.

Retrospectively, the last year delivered a decent 3.9% gain to the company's revenues. Pleasingly, revenue has also lifted 66% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 5.0% per year during the coming three years according to the ten analysts following the company. That's shaping up to be similar to the 6.9% each year growth forecast for the broader industry.

With this in consideration, we find it intriguing that HBX Group International's P/S is higher than its industry peers. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

What We Can Learn From HBX Group International's P/S?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Given HBX Group International's future revenue forecasts are in line with the wider industry, the fact that it trades at an elevated P/S is somewhat surprising. When we see revenue growth that just matches the industry, we don't expect elevates P/S figures to remain inflated for the long-term. Unless the company can jump ahead of the rest of the industry in the short-term, it'll be a challenge to maintain the share price at current levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with HBX Group International, and understanding should be part of your investment process.

If you're unsure about the strength of HBX Group International's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.