Nasdaq

Nasdaq 华尔街日报

华尔街日报Atrem S.A. (WSE:ATR) Stocks Shoot Up 30% But Its P/E Still Looks Reasonable

Atrem S.A. (WSE:ATR) shareholders would be excited to see that the share price has had a great month, posting a 30% gain and recovering from prior weakness. The annual gain comes to 281% following the latest surge, making investors sit up and take notice.

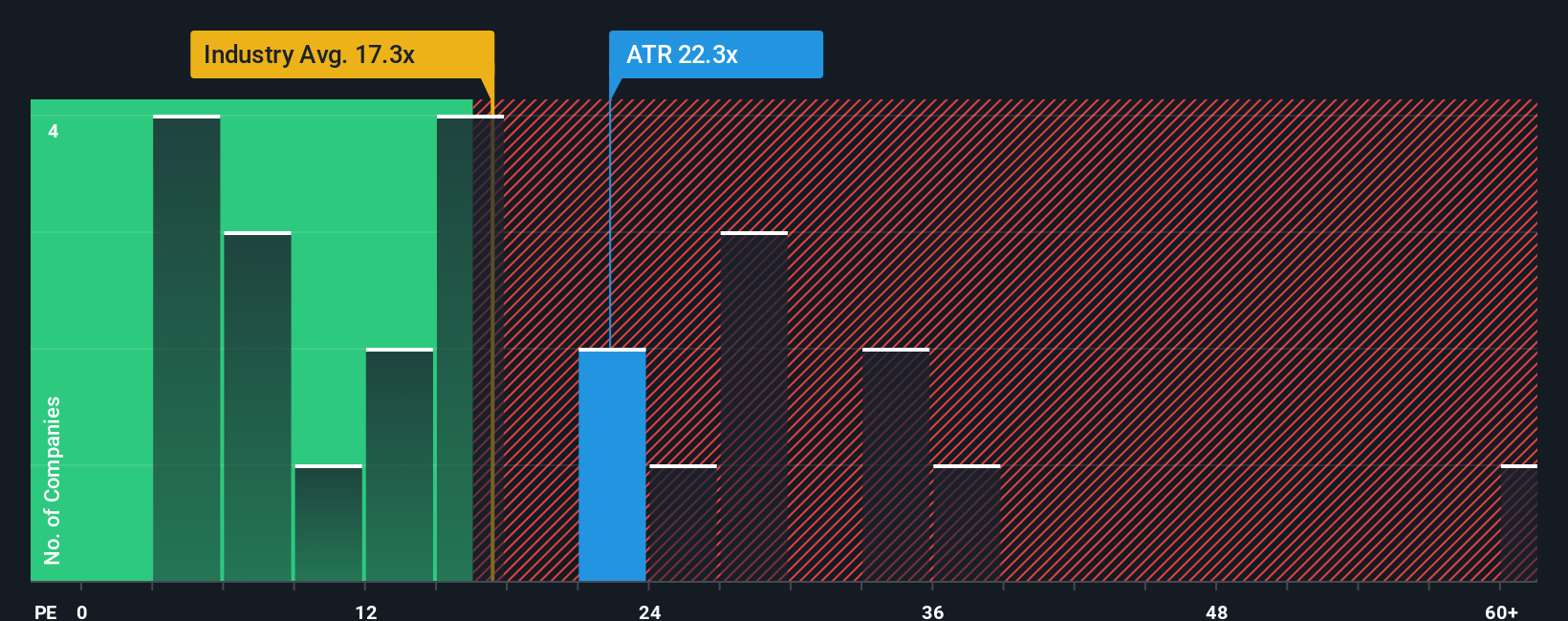

Following the firm bounce in price, given close to half the companies in Poland have price-to-earnings ratios (or "P/E's") below 12x, you may consider Atrem as a stock to avoid entirely with its 22.3x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's exceedingly strong of late, Atrem has been doing very well. It seems that many are expecting the strong earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Atrem

Does Growth Match The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as Atrem's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered an exceptional 56% gain to the company's bottom line. The latest three year period has also seen an excellent 165% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Comparing that to the market, which is only predicted to deliver 18% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we can see why Atrem is trading at such a high P/E compared to the market. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Bottom Line On Atrem's P/E

The strong share price surge has got Atrem's P/E rushing to great heights as well. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Atrem maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

You always need to take note of risks, for example - Atrem has 2 warning signs we think you should be aware of.

Of course, you might also be able to find a better stock than Atrem. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.