Nasdaq

Nasdaq 华尔街日报

华尔街日报Companhia Siderúrgica Nacional (BVMF:CSNA3) Not Lagging Industry On Growth Or Pricing

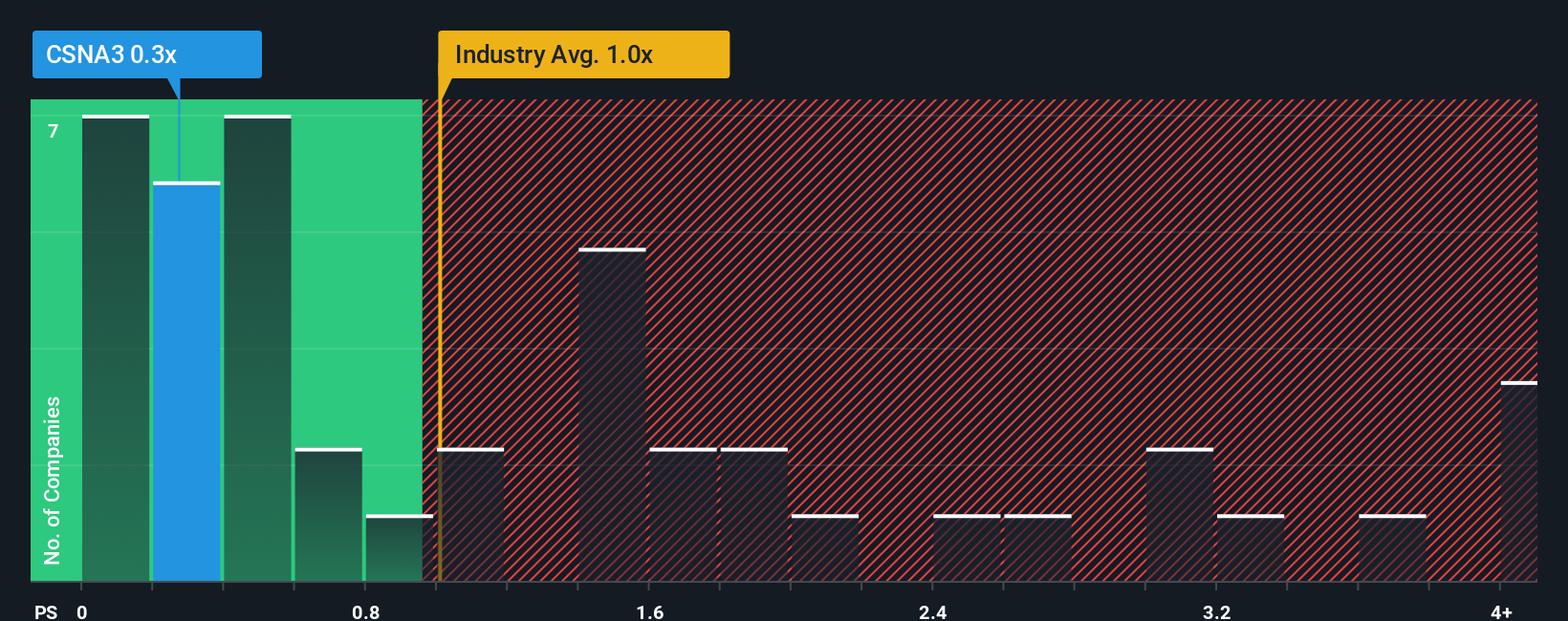

With a median price-to-sales (or "P/S") ratio of close to 0.5x in the Metals and Mining industry in Brazil, you could be forgiven for feeling indifferent about Companhia Siderúrgica Nacional's (BVMF:CSNA3) P/S ratio of 0.3x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

See our latest analysis for Companhia Siderúrgica Nacional

How Has Companhia Siderúrgica Nacional Performed Recently?

Recent revenue growth for Companhia Siderúrgica Nacional has been in line with the industry. It seems that many are expecting the mediocre revenue performance to persist, which has held the P/S ratio back. Those who are bullish on Companhia Siderúrgica Nacional will be hoping that revenue performance can pick up, so that they can pick up the stock at a slightly lower valuation.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Companhia Siderúrgica Nacional.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Companhia Siderúrgica Nacional's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.0% last year. Still, revenue has barely risen at all in aggregate from three years ago, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 2.1% each year as estimated by the twelve analysts watching the company. With the industry predicted to deliver 1.7% growth per annum, the company is positioned for a comparable revenue result.

With this information, we can see why Companhia Siderúrgica Nacional is trading at a fairly similar P/S to the industry. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Bottom Line On Companhia Siderúrgica Nacional's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

A Companhia Siderúrgica Nacional's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Metals and Mining industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

Having said that, be aware Companhia Siderúrgica Nacional is showing 2 warning signs in our investment analysis, you should know about.

If you're unsure about the strength of Companhia Siderúrgica Nacional's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.