Nasdaq

Nasdaq 华尔街日报

华尔街日报Market Cool On BRAIN Biotech AG's (ETR:BNN) Revenues Pushing Shares 28% Lower

BRAIN Biotech AG (ETR:BNN) shares have retraced a considerable 28% in the last month, reversing a fair amount of their solid recent performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 24% share price drop.

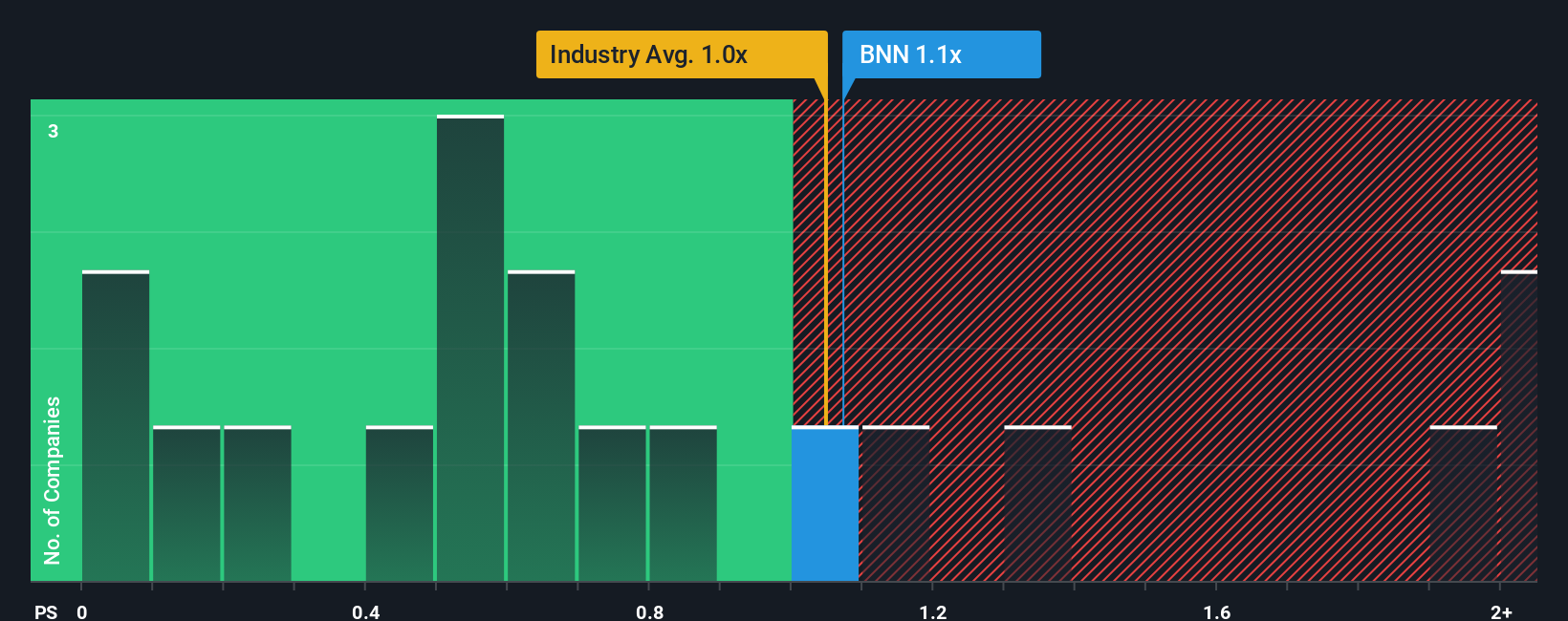

Even after such a large drop in price, it's still not a stretch to say that BRAIN Biotech's price-to-sales (or "P/S") ratio of 1.1x right now seems quite "middle-of-the-road" compared to the Chemicals industry in Germany, where the median P/S ratio is around 0.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for BRAIN Biotech

What Does BRAIN Biotech's P/S Mean For Shareholders?

BRAIN Biotech could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. One possibility is that the P/S ratio is moderate because investors think this poor revenue performance will turn around. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on BRAIN Biotech.Is There Some Revenue Growth Forecasted For BRAIN Biotech?

There's an inherent assumption that a company should be matching the industry for P/S ratios like BRAIN Biotech's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 4.7%. Regardless, revenue has managed to lift by a handy 13% in aggregate from three years ago, thanks to the earlier period of growth. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

Turning to the outlook, the next three years should generate growth of 10% each year as estimated by the four analysts watching the company. Meanwhile, the rest of the industry is forecast to only expand by 1.7% each year, which is noticeably less attractive.

With this information, we find it interesting that BRAIN Biotech is trading at a fairly similar P/S compared to the industry. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From BRAIN Biotech's P/S?

With its share price dropping off a cliff, the P/S for BRAIN Biotech looks to be in line with the rest of the Chemicals industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Looking at BRAIN Biotech's analyst forecasts revealed that its superior revenue outlook isn't giving the boost to its P/S that we would've expected. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. This uncertainty seems to be reflected in the share price which, while stable, could be higher given the revenue forecasts.

Before you take the next step, you should know about the 2 warning signs for BRAIN Biotech that we have uncovered.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.