Nasdaq

Nasdaq 华尔街日报

华尔街日报European Growth Stocks With Insider Ownership Growing Earnings Up To 103%

As the pan-European STOXX Europe 600 Index rises by 1.60% amid signs of steady economic growth and looser monetary policy, investors are keenly observing opportunities within the region's market landscape. In this context, stocks with high insider ownership can be particularly appealing, as they often indicate strong confidence from those closest to the company—an important factor when considering potential growth in a fluctuating economic environment.

Top 10 Growth Companies With High Insider Ownership In Europe

| Name | Insider Ownership | Earnings Growth |

| Warimpex Finanz- und Beteiligungs (WBAG:WXF) | 25.9% | 100.6% |

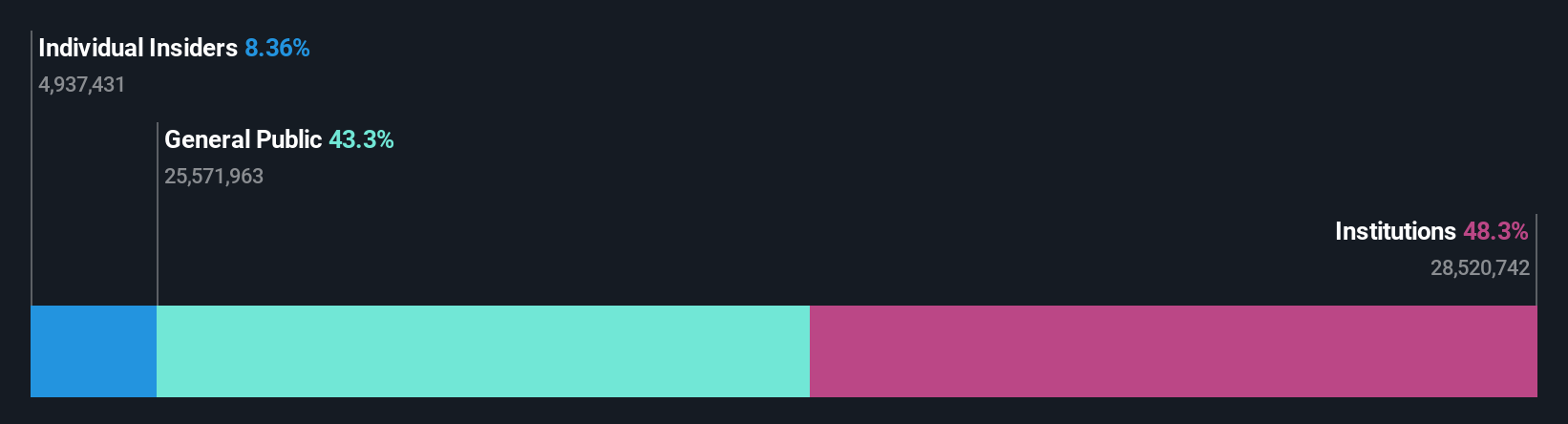

| S.M.A.I.O (ENXTPA:ALSMA) | 16.1% | 72.8% |

| Skolon (OM:SKOLON) | 32.3% | 126.5% |

| MilDef Group (OM:MILDEF) | 13.7% | 83% |

| Magnora (OB:MGN) | 10.4% | 75.1% |

| KebNi (OM:KEBNI B) | 36.3% | 61.2% |

| DNO (OB:DNO) | 13.5% | 97.5% |

| CTT Systems (OM:CTT) | 17.5% | 52% |

| Circus (XTRA:CA1) | 24.1% | 66.1% |

| Bonesupport Holding (OM:BONEX) | 10.4% | 49.6% |

Here's a peek at a few of the choices from the screener.

P/F Bakkafrost (OB:BAKKA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: P/F Bakkafrost, along with its subsidiaries, is engaged in the production and sale of salmon products across North America, Western Europe, Eastern Europe, Asia, and other international markets, with a market cap of NOK30.76 billion.

Operations: The company's revenue segments include Sales and Other (DKK 9.78 billion), Fishmeal, Oil and Feed (DKK 2.48 billion), Farming Faroe Islands (DKK 3.78 billion), Farming Scotland (DKK 1.11 billion), Freshwater Faroe Islands (DKK 901.81 million), Freshwater Scotland (DKK 133.57 million), and Services (DKK 878.36 million).

Insider Ownership: 24%

Earnings Growth Forecast: 71.7% p.a.

P/F Bakkafrost demonstrates potential as a growth company with high insider ownership in Europe. Despite a modest decline in third-quarter sales to DKK 1.69 billion, the company turned around its net income to DKK 76.53 million from a loss last year, reflecting operational improvements. Forecasts indicate significant earnings growth of over 71% annually, outpacing the Norwegian market's average. However, revenue growth is projected at 14.4%, slower than some high-growth benchmarks but still above market averages.

- Dive into the specifics of P/F Bakkafrost here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential undervaluation of P/F Bakkafrost shares in the market.

Sdiptech (OM:SDIP B)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sdiptech AB (publ) offers technical services for infrastructure across multiple countries, including Sweden, the UK, Germany, and the US, with a market cap of SEK7.29 billion.

Operations: The company generates revenue through its provision of technical services for infrastructure in various countries, including Sweden, the United Kingdom, Germany, Denmark, Italy, the Netherlands, Austria, Norway, Finland, and the United States.

Insider Ownership: 10.3%

Earnings Growth Forecast: 103.7% p.a.

Sdiptech AB is exploring M&A opportunities to enhance growth, supported by a strong internal team and proactive outreach. Despite a recent net loss of SEK 452 million for Q3 2025, the company remains undervalued, trading at 56% below its estimated fair value. Insider buying has occurred recently, albeit not in substantial volumes. Revenue growth is forecast at 4.6% annually, slightly above the Swedish market average but slower than high-growth benchmarks.

- Click here to discover the nuances of Sdiptech with our detailed analytical future growth report.

- Our valuation report unveils the possibility Sdiptech's shares may be trading at a discount.

Vimian Group (OM:VIMIAN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Vimian Group AB (publ) operates in the global animal health industry and has a market capitalization of approximately SEK15.80 billion.

Operations: The company generates revenue from several segments, including Medtech (€153.80 million), Diagnostics (€22.70 million), Specialty Pharma (€181.60 million), and Veterinary Services (€63.10 million).

Insider Ownership: 12.7%

Earnings Growth Forecast: 39.1% p.a.

Vimian Group is actively pursuing acquisitions to bolster its growth strategy, aiming for EUR 300 million in revenue by 2030 without exceeding a leverage of 3.0x. The company reported Q3 sales of EUR 104.30 million, up from EUR 87.60 million the previous year, with net income rising to EUR 6.50 million from a loss of EUR 2.10 million. Analysts expect earnings to grow significantly at an annual rate of over 20%, outpacing the Swedish market average.

- Take a closer look at Vimian Group's potential here in our earnings growth report.

- According our valuation report, there's an indication that Vimian Group's share price might be on the cheaper side.

Turning Ideas Into Actions

- Investigate our full lineup of 211 Fast Growing European Companies With High Insider Ownership right here.

- Interested In Other Possibilities? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com