Nasdaq

Nasdaq 华尔街日报

华尔街日报MiMedx (MDXG): Fresh Clinical Evidence Spurs a Closer Look at the Stock’s Valuation and Long-Term Upside Potential

MiMedx Group (MDXG) just added fresh peer reviewed backing for its placental allograft products, with a new Journal of Inflammation study underscoring their immunomodulatory role in complex wound healing and longer term competitive positioning.

See our latest analysis for MiMedx Group.

Even with this new clinical validation, MiMedx Group’s $7.05 share price sits well below its highs, with a year-to-date share price return of negative 24.03 percent and a powerful three-year total shareholder return of 154.51 percent suggesting longer term momentum is still very much intact.

If this kind of evidence driven growth story has your attention, it is worth widening the lens and seeing which other healthcare stocks are quietly building similar momentum.

With shares still trading at a steep discount to analyst targets despite double digit revenue and profit growth, the key question now is whether MiMedx is genuinely undervalued or if the market is already pricing in its next leg of expansion.

Most Popular Narrative Narrative: 42.2% Undervalued

With MiMedx Group’s fair value set well above the recent 7.05 close, the most followed narrative leans firmly toward a compelling long term opportunity.

The company's strong clinical evidence base and focus on product efficacy position it to gain market share as Medicare reimbursement reforms shift the market away from price competition and toward clinical and cost effectiveness, likely supporting revenue and protecting/increasing net margins.

Curious how sustained double digit growth, rising margins and a premium future earnings multiple can all align under a single discount rate story? Click through.

Result: Fair Value of $12.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, looming Medicare reimbursement shifts and potential market contraction for skin substitutes could quickly challenge the growth and valuation assumptions behind this bullish case.

Find out about the key risks to this MiMedx Group narrative.

Another View: Valuation Signals Clash

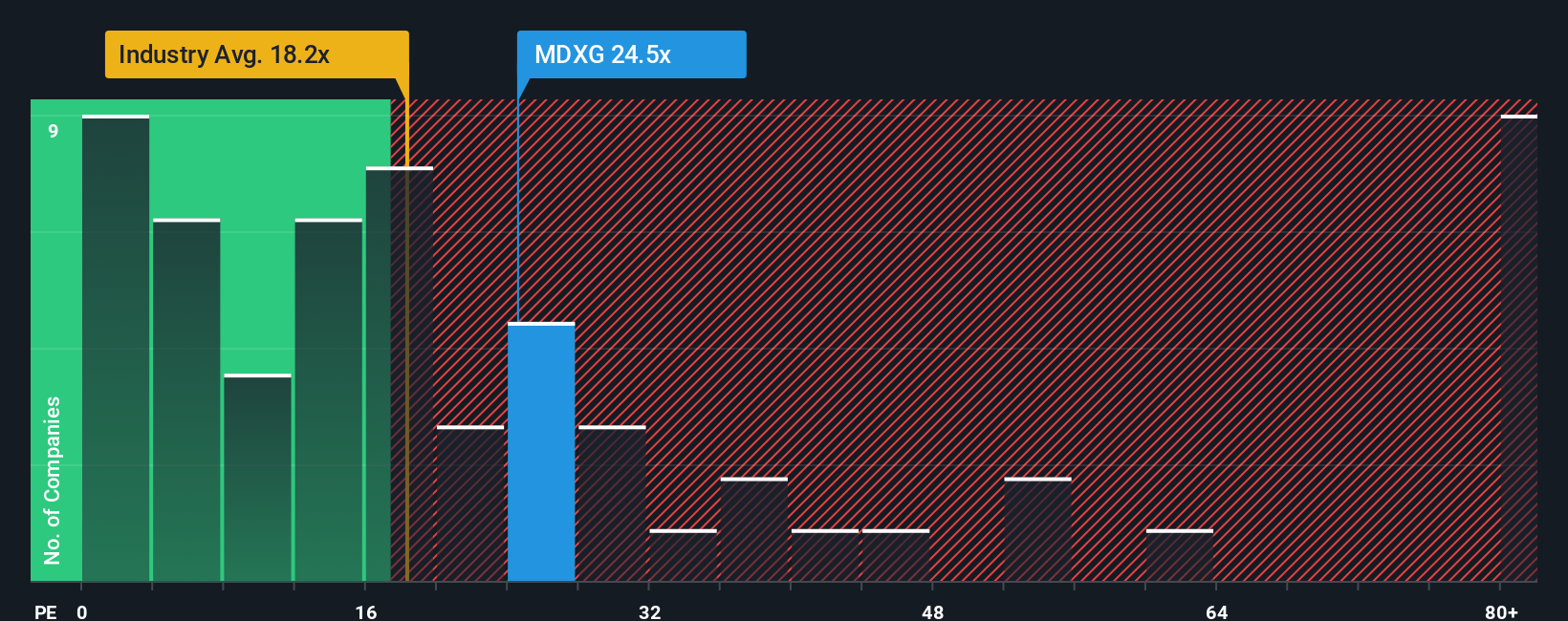

Despite the narrative pointing to a fair value of 12.20, the earnings based lens sends a very different message. At 25.6 times earnings versus a fair ratio of 18.2 times and an industry average of 20.7 times, MiMedx screens expensive, raising the question of who is right: the story or the multiple.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own MiMedx Group Narrative

If you see the story differently or want to test your own assumptions against the numbers, you can build a complete narrative in under three minutes: Do it your way.

A great starting point for your MiMedx Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, put Simply Wall Street’s powerful screener to work so you do not miss the next wave of high conviction opportunities beyond MiMedx.

- Capture early stage potential by reviewing these 3633 penny stocks with strong financials that pair smaller market caps with surprisingly resilient financial profiles.

- Position your portfolio for the next productivity surge by targeting these 24 AI penny stocks reshaping industries with real world artificial intelligence applications.

- Focus on these 12 dividend stocks with yields > 3% that provide consistent cash payouts if you are seeking income and stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com