Nasdaq

Nasdaq 华尔街日报

华尔街日报Is It Too Late to Consider Pitney Bowes After Its 216% Three Year Surge?

- Wondering if Pitney Bowes is still a bargain after its big run, or if the easy money has already been made? You are not alone, and that is exactly what we are going to unpack here.

- The stock is now trading around $10.62, up 3.8% over the last week, 12.0% over the past month, and 47.1% year to date, building on 51.3% returns over 1 year and 216.0% over 3 years.

- Those gains have come as investors have warmed to Pitney Bowes transformation story and shifting mix toward higher margin, tech enabled services. This has helped reset expectations for what this legacy mailing name can be worth. At the same time, ongoing strategic reviews and portfolio moves have kept speculation alive about how much more value could be unlocked if management continues to streamline the business.

- Despite that backdrop, Pitney Bowes only scores a 4/6 valuation score, suggesting there may still be mispricing that traditional metrics only partly capture. Next we will walk through the standard valuation approaches and then finish with a more holistic way to think about what this stock might really be worth.

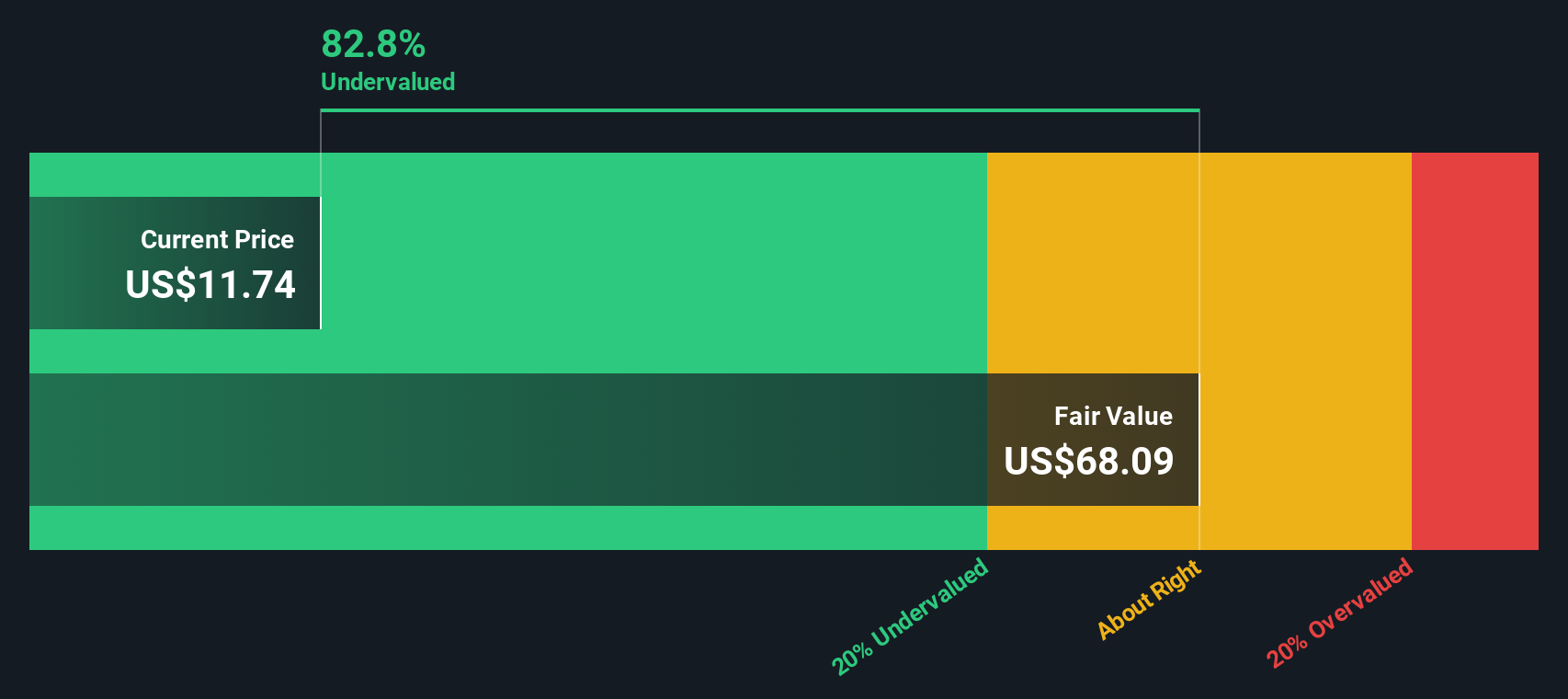

Approach 1: Pitney Bowes Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms.

For Pitney Bowes, the 2 Stage Free Cash Flow to Equity model starts with last twelve month free cash flow of about $228.8 million and then incorporates analyst forecasts through 2027, followed by more gradual growth estimates beyond that period. By 2027, free cash flow is projected to reach roughly $372.6 million, and the extended 10-year projections rise toward the mid-$400 million range as the business matures.

When those future cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about $38.43 per share. Compared with a recent share price around $10.62, the DCF suggests the stock is roughly 72.4% below this intrinsic value estimate, indicating that investors may be pricing in a high degree of pessimism relative to the modeled cash flow outlook.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pitney Bowes is undervalued by 72.4%. Track this in your watchlist or portfolio, or discover 913 more undervalued stocks based on cash flows.

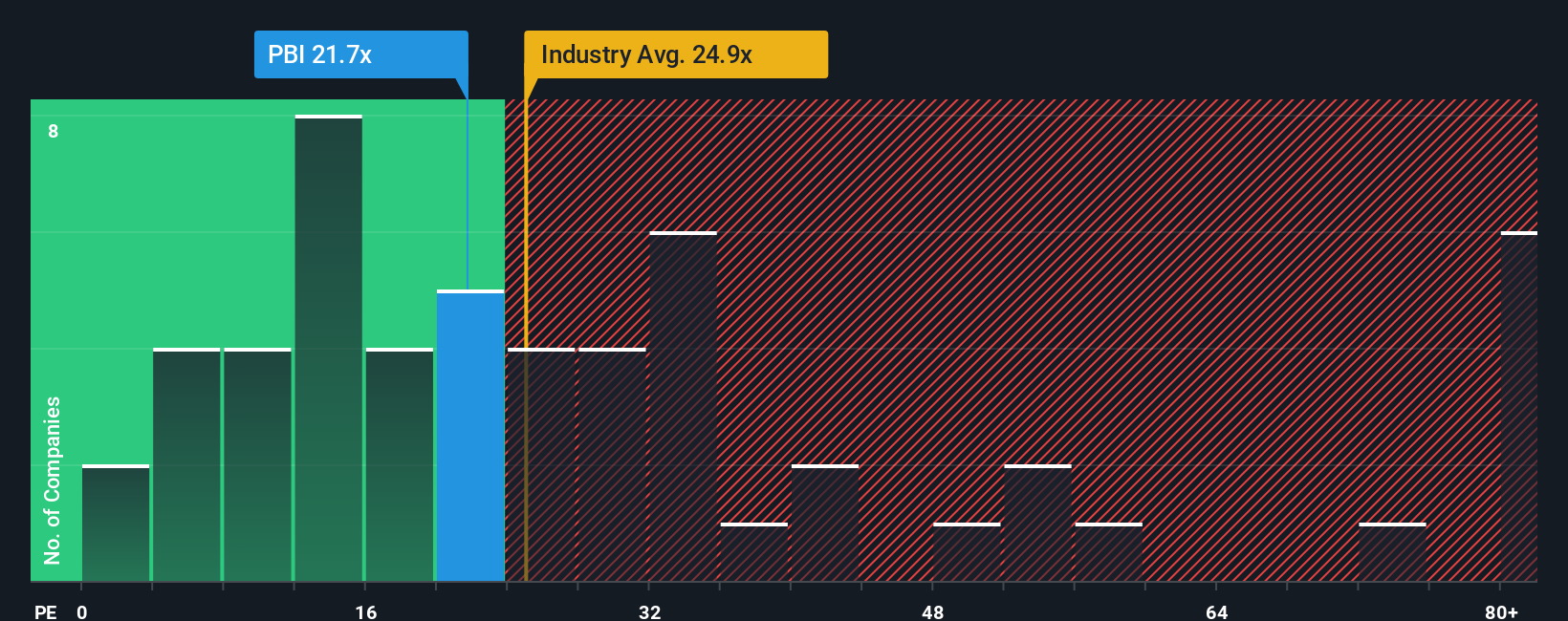

Approach 2: Pitney Bowes Price vs Earnings

For profitable companies like Pitney Bowes, the price to earnings (PE) ratio is a useful way to gauge how much investors are willing to pay today for each dollar of current earnings. In general, companies with stronger growth prospects and lower perceived risk can justify a higher PE, while slower growing or riskier businesses tend to deserve a lower, more conservative multiple.

Pitney Bowes currently trades on a PE of about 22.7x, which is roughly in line with the broader Commercial Services industry average of around 22.9x, but above the peer group average of about 14.7x. To go a step further, Simply Wall St calculates a proprietary Fair Ratio of 29.0x, reflecting what the PE might reasonably be given Pitney Bowes earnings growth profile, margins, industry, size and specific risk factors.

This Fair Ratio can be more insightful than a simple comparison with peers or the industry, because it adjusts for the company’s own fundamentals rather than assuming it should look like the average stock. With Pitney Bowes trading at 22.7x versus a Fair Ratio of 29.0x, the multiple suggests the market is still undervaluing its earnings power.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pitney Bowes Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Pitney Bowes business with a concrete forecast and Fair Value estimate. A Narrative is your story behind the numbers, where you spell out how you expect revenue, earnings and margins to evolve, and Simply Wall St turns that story into a financial forecast and Fair Value that you can compare with today’s share price. Narratives are available on the Pitney Bowes Community page on Simply Wall St, used by millions of investors, and they update dynamically as new information like earnings reports or news on buybacks and dividends comes in. This can make it easier to decide when to buy or sell because you can see at a glance whether your Fair Value is above or below the current price, and how that compares with other investors whose Narratives might imply, for example, a more cautious $13 per share outcome or a more optimistic view based on stronger margin expansion and capital returns.

Do you think there's more to the story for Pitney Bowes? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com