Nasdaq

Nasdaq 华尔街日报

华尔街日报US Market Undiscovered Gems For December 2025

As the U.S. market navigates a landscape marked by surging tech shares and volatile index movements, investors are keenly observing how these dynamics impact small-cap stocks, particularly within the S&P 600. With major indices like the Nasdaq and S&P 500 experiencing gains driven by AI-related optimism, identifying lesser-known stocks with strong fundamentals can be key to capitalizing on potential growth opportunities amidst broader market shifts.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 57.63% | 1.47% | -2.43% | ★★★★★★ |

| Southern Michigan Bancorp | 113.59% | 8.48% | 3.73% | ★★★★★★ |

| Tri-County Financial Group | 102.20% | -2.69% | -15.63% | ★★★★★★ |

| Franklin Financial Services | 127.01% | 5.48% | -4.56% | ★★★★★★ |

| Epsilon Energy | NA | 2.43% | -4.36% | ★★★★★★ |

| Affinity Bancshares | 43.06% | 2.84% | 3.44% | ★★★★★★ |

| Metalpha Technology Holding | NA | 75.66% | 28.60% | ★★★★★★ |

| FineMark Holdings | 114.54% | 2.38% | -28.53% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 13.18% | 16.77% | ★★★★★☆ |

| FRMO | 0.10% | 35.28% | 40.61% | ★★★★★☆ |

Let's dive into some prime choices out of from the screener.

Bankwell Financial Group (BWFG)

Simply Wall St Value Rating: ★★★★★★

Overview: Bankwell Financial Group, Inc. is the bank holding company for Bankwell Bank, offering a range of banking services to individual and commercial clients, with a market capitalization of $383.89 million.

Operations: Bankwell Financial Group generates revenue primarily through its banking segment, which reported $94.28 million in revenue.

Bankwell Financial Group, with assets totaling US$3.2 billion and equity of US$292.8 million, is making strides in the banking sector by expanding its deposit teams and investing in digital efficiencies to cut funding costs. The bank's total deposits stand at US$2.8 billion, while loans are US$2.7 billion, reflecting a robust lending portfolio supported by a sufficient bad loan allowance of 0.6% of total loans. Earnings growth over the past year has been impressive at 91.7%, outpacing the industry average significantly, which speaks to its strong performance amidst challenges such as rising operational costs and competition from larger banks and fintechs.

Investors Title (ITIC)

Simply Wall St Value Rating: ★★★★★★

Overview: Investors Title Company provides title insurance services for residential, institutional, commercial, and industrial properties with a market cap of $485.33 million.

Operations: Investors Title generates revenue primarily from its title insurance segment, which accounts for $267.13 million, with additional contributions from exchange services at $13.55 million.

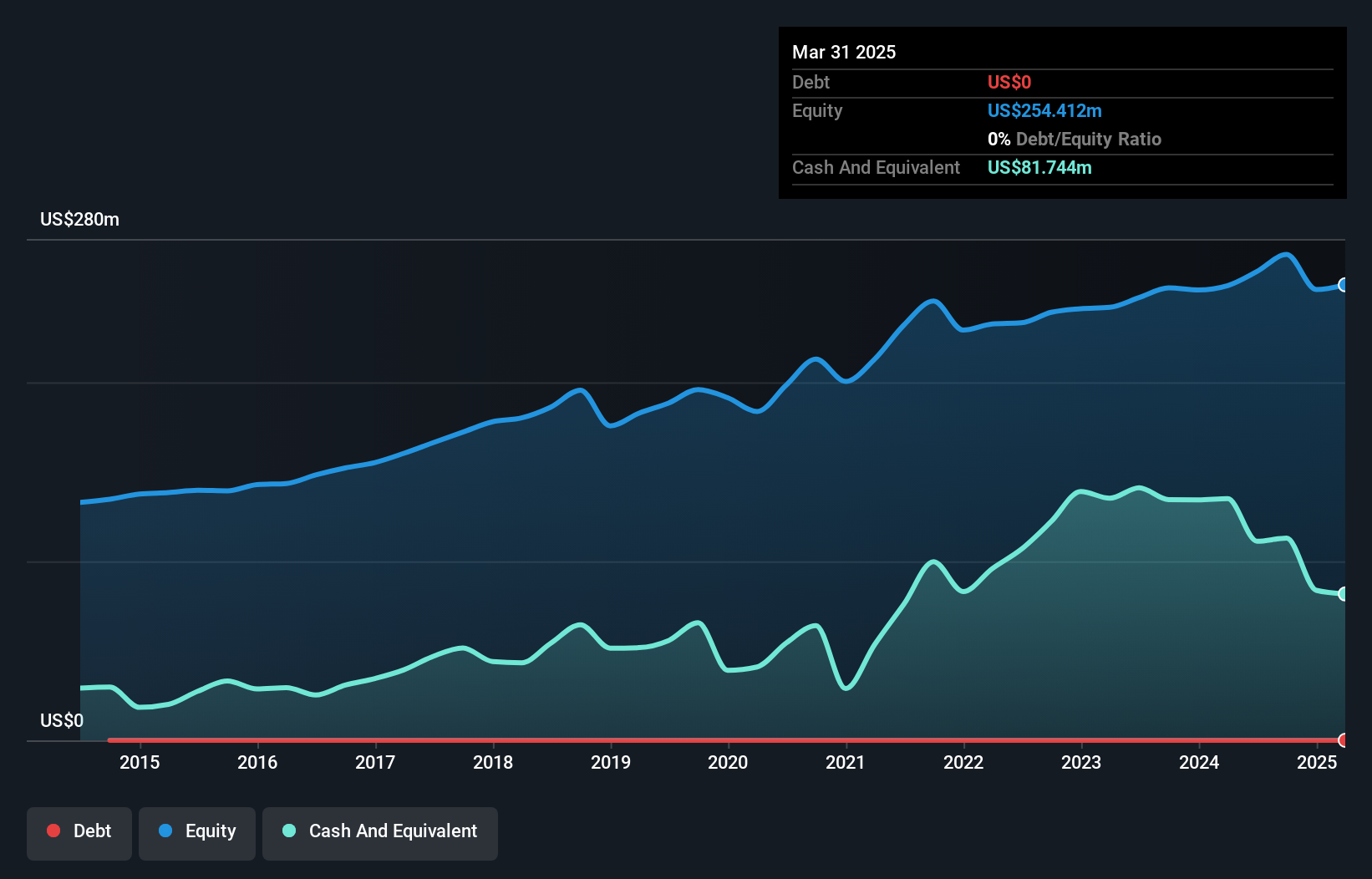

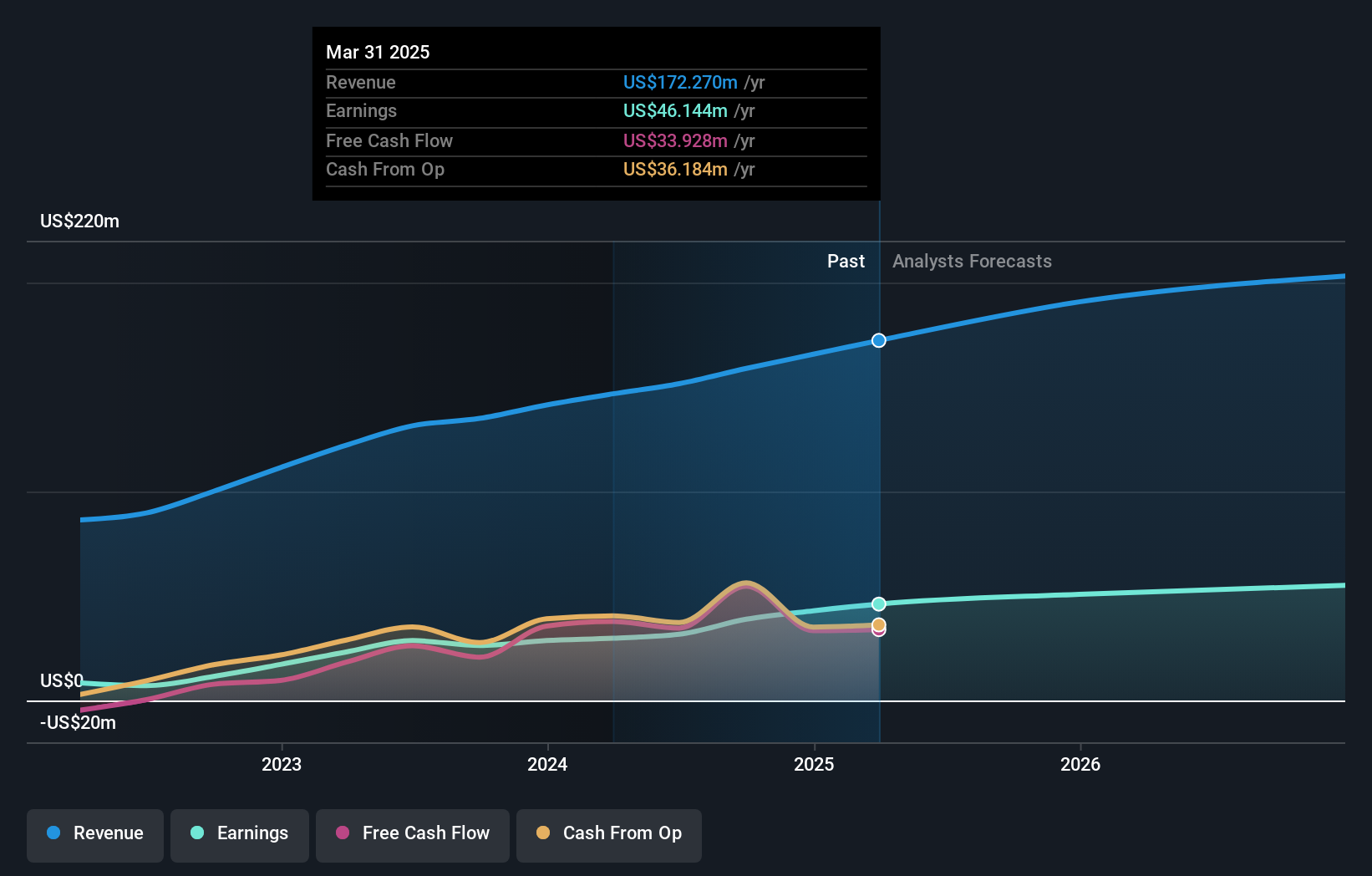

Investors Title, a nimble player in the insurance space, has showcased impressive earnings growth of 26% over the past year, outpacing its industry peers. Despite a 16% annual decline over five years, recent results are promising with third-quarter revenue at US$73.02 million and net income climbing to US$12.21 million from US$9.32 million last year. The company is debt-free and trades slightly below its estimated fair value, suggesting potential upside for investors seeking value in this sector. Recent announcements include a special dividend of US$8.72 per share and regular quarterly dividends affirming shareholder returns focus.

- Take a closer look at Investors Title's potential here in our health report.

Evaluate Investors Title's historical performance by accessing our past performance report.

Third Coast Bancshares (TCBX)

Simply Wall St Value Rating: ★★★★★★

Overview: Third Coast Bancshares, Inc. is a bank holding company for Third Coast Bank, offering a range of commercial banking services to small and medium-sized businesses and professionals in the United States, with a market cap of $575.01 million.

Operations: Third Coast Bancshares generates revenue primarily through its community banking segment, which reported $192.22 million. The company's market capitalization stands at approximately $575 million.

Third Coast Bancshares, with assets totaling US$5.1 billion and equity of US$513.8 million, is making waves in the banking sector. Its earnings growth last year was a robust 47.6%, significantly outpacing the industry average of 18.5%. This bank boasts a solid foundation with customer deposits comprising 96% of its liabilities, minimizing risk compared to external borrowing. With total loans at US$4.1 billion and deposits at US$4.4 billion, it maintains an appropriate bad loan ratio of just 0.5%. Trading nearly 20% below estimated fair value, Third Coast seems poised for potential upside despite recent index exclusion setbacks.

- Dive into the specifics of Third Coast Bancshares here with our thorough health report.

Understand Third Coast Bancshares' track record by examining our Past report.

Seize The Opportunity

- Get an in-depth perspective on all 298 US Undiscovered Gems With Strong Fundamentals by using our screener here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com