Nasdaq

Nasdaq 华尔街日报

华尔街日报There Is A Reason SolarMax Technology, Inc.'s (NASDAQ:SMXT) Price Is Undemanding

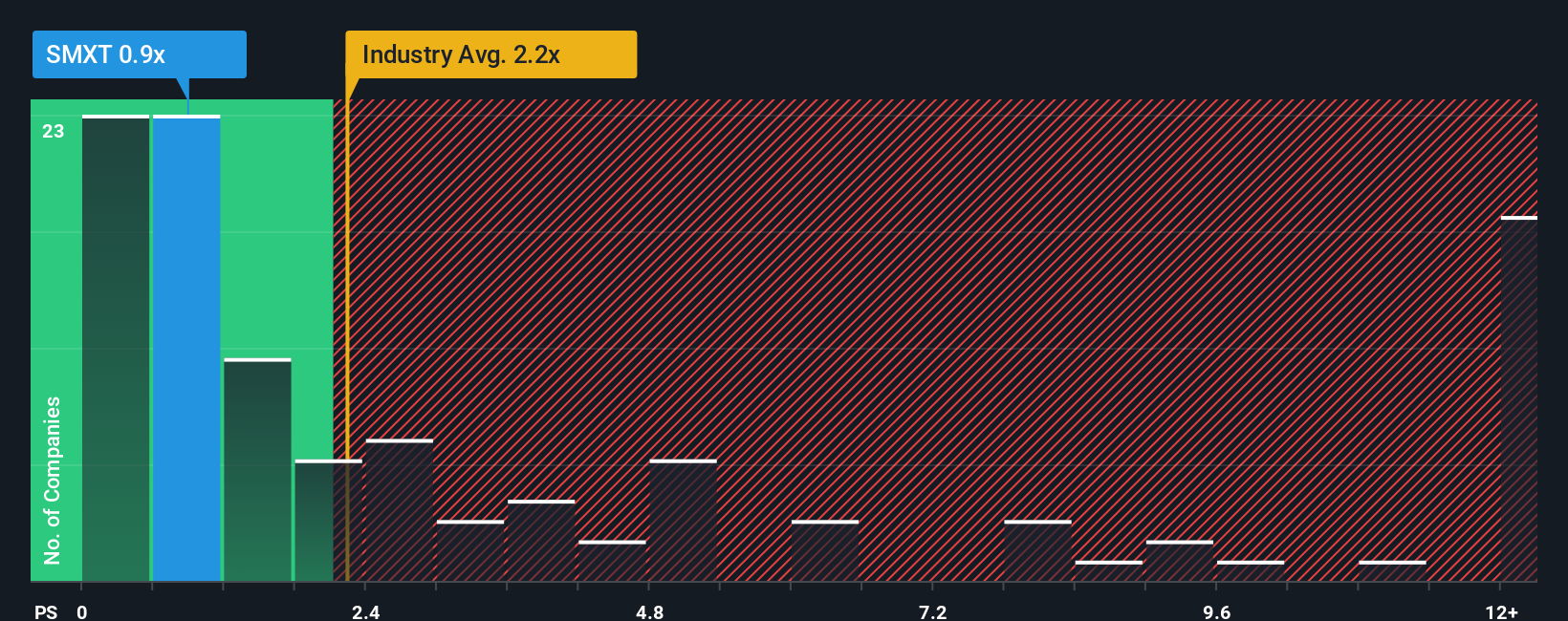

You may think that with a price-to-sales (or "P/S") ratio of 0.9x SolarMax Technology, Inc. (NASDAQ:SMXT) is a stock worth checking out, seeing as almost half of all the Electrical companies in the United States have P/S ratios greater than 2.2x and even P/S higher than 6x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for SolarMax Technology

How Has SolarMax Technology Performed Recently?

Recent times have been quite advantageous for SolarMax Technology as its revenue has been rising very briskly. Perhaps the market is expecting future revenue performance to dwindle, which has kept the P/S suppressed. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on SolarMax Technology will help you shine a light on its historical performance.Is There Any Revenue Growth Forecasted For SolarMax Technology?

There's an inherent assumption that a company should underperform the industry for P/S ratios like SolarMax Technology's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 77% last year. The strong recent performance means it was also able to grow revenue by 31% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 12% shows it's noticeably less attractive.

With this in consideration, it's easy to understand why SolarMax Technology's P/S falls short of the mark set by its industry peers. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

What We Can Learn From SolarMax Technology's P/S?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of SolarMax Technology revealed its three-year revenue trends are contributing to its low P/S, given they look worse than current industry expectations. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for SolarMax Technology (2 can't be ignored) you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.