Nasdaq

Nasdaq 华尔街日报

华尔街日报After Leaping 42% Sunlight (1977) Holdings Limited (HKG:8451) Shares Are Not Flying Under The Radar

Sunlight (1977) Holdings Limited (HKG:8451) shareholders have had their patience rewarded with a 42% share price jump in the last month. Looking further back, the 15% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

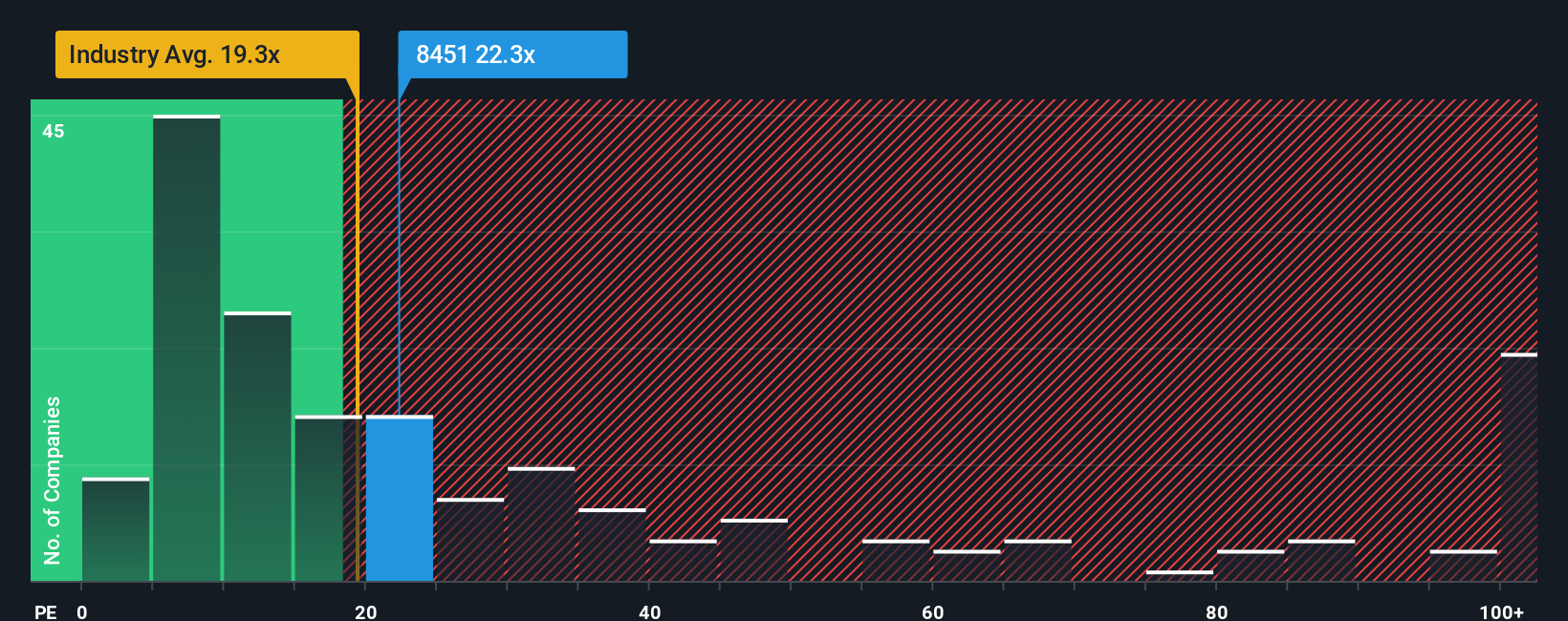

Following the firm bounce in price, given close to half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") below 12x, you may consider Sunlight (1977) Holdings as a stock to avoid entirely with its 22.3x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

For example, consider that Sunlight (1977) Holdings' financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

Check out our latest analysis for Sunlight (1977) Holdings

How Is Sunlight (1977) Holdings' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Sunlight (1977) Holdings' is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 31% decrease to the company's bottom line. Even so, admirably EPS has lifted 95% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 21% shows it's noticeably more attractive on an annualised basis.

In light of this, it's understandable that Sunlight (1977) Holdings' P/E sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From Sunlight (1977) Holdings' P/E?

Sunlight (1977) Holdings' P/E is flying high just like its stock has during the last month. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Sunlight (1977) Holdings maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 3 warning signs for Sunlight (1977) Holdings (1 is significant!) that we have uncovered.

Of course, you might also be able to find a better stock than Sunlight (1977) Holdings. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.