Nasdaq

Nasdaq 华尔街日报

华尔街日报Is JPMorgan Still Attractive After Its Strong 2025 Share Price Rally?

- If you are wondering whether JPMorgan Chase is still a buy after its huge run, you are not alone. This article is going to unpack whether the current price really makes sense.

- The stock has climbed 1.5% over the last week, 5.4% over the past month, and is now up an impressive 33.3% year to date, with a 36.4% gain over the last year and almost tripling over three and five years.

- Much of this strength has been underpinned by JPMorgan's role as a bellwether for the US banking sector, as investors keep rewarding its scale, balance sheet resilience, and dominant position in everything from consumer banking to investment banking. More broadly, the market has been rotating toward large, well capitalized financials in anticipation of a more stable rate environment and a still resilient US economy. Both of these support JPMorgan's premium status.

- Yet, despite its track record, JPMorgan only scores 2 out of 6 on our valuation checks, suggesting the story is more nuanced than "great bank, great stock". We will walk through different valuation methods, then finish with a more intuitive way to think about what the market is really pricing in.

JPMorgan Chase scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

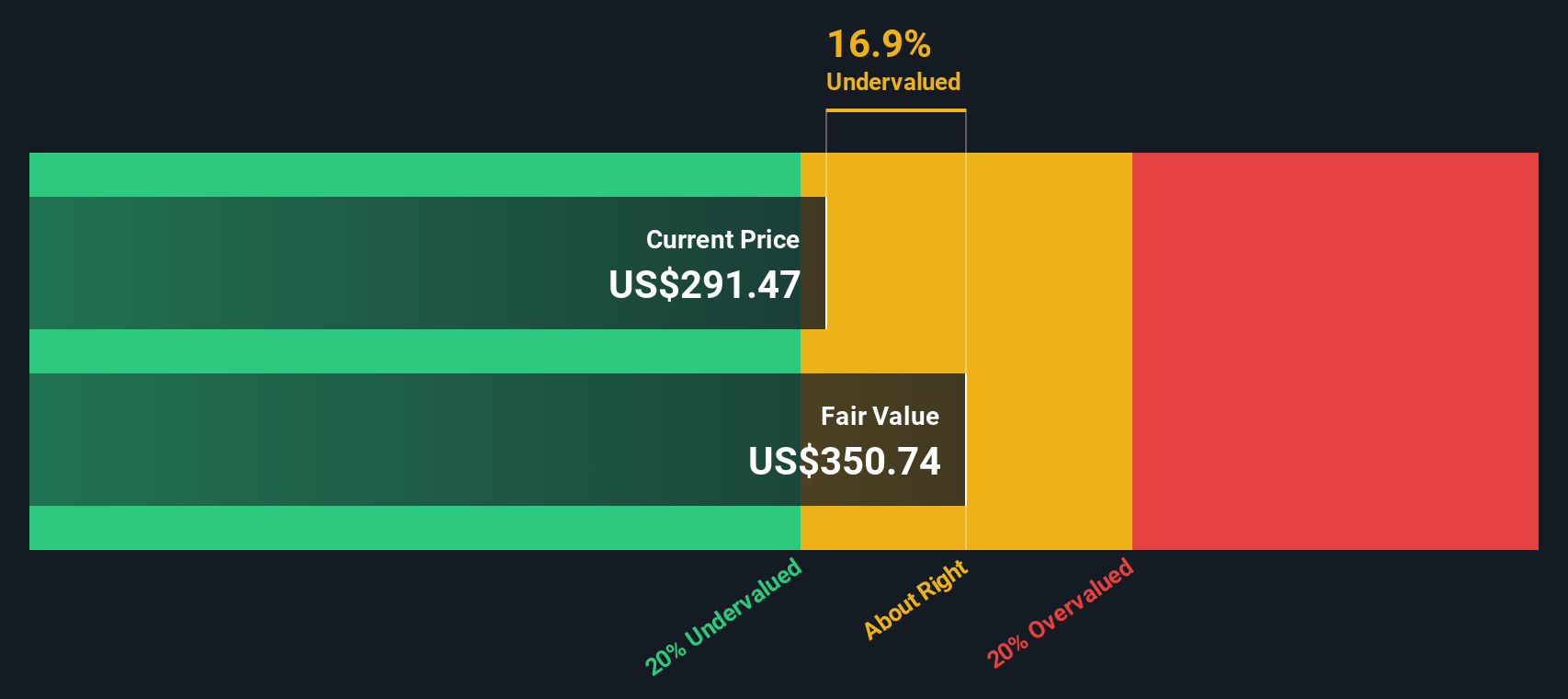

Approach 1: JPMorgan Chase Excess Returns Analysis

The Excess Returns model asks a simple question: how much value can JPMorgan Chase create above the return that shareholders require on their capital? It looks at the bank's book value, the profits it can sustainably earn on that equity, and the spread over its cost of equity.

For JPMorgan, the starting Book Value is $124.96 per share, with a Stable EPS of $22.45 per share, based on weighted future Return on Equity estimates from 13 analysts. That implies an Average Return on Equity of 16.59%, comfortably above the Cost of Equity of $11.09 per share. The difference, an Excess Return of $11.36 per share, is then projected forward using a Stable Book Value of $135.36 per share, also anchored on analyst forecasts.

When these excess returns are capitalized, the model produces an intrinsic value of about $365.59 per share. Compared with the current market price, this suggests the stock is roughly 12.5% undervalued.

Result: UNDERVALUED

Our Excess Returns analysis suggests JPMorgan Chase is undervalued by 12.5%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

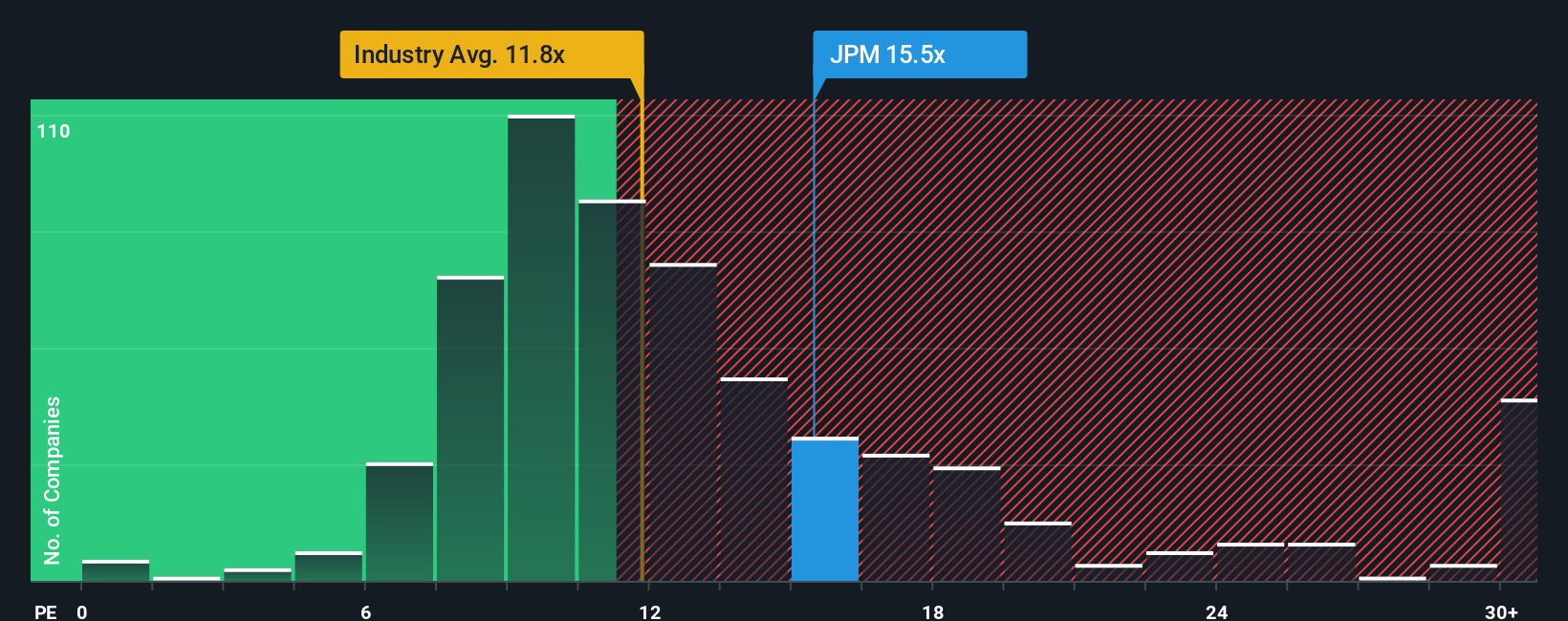

Approach 2: JPMorgan Chase Price vs Earnings

For a consistently profitable bank like JPMorgan, the price to earnings ratio is a sensible way to gauge value because it directly links what investors are paying to the profits the company is generating today. In general, faster earnings growth and lower perceived risk justify a higher PE ratio, while slower growth or higher uncertainty usually warrant a lower, more conservative multiple.

JPMorgan currently trades on about 15.4x earnings, which is meaningfully above the broader Banks industry average of 12.0x and also above the 14.0x average of its large cap peers. On the surface, that premium suggests investors are already paying up for JPMorgan's scale, resilience, and quality.

Simply Wall St's Fair Ratio for JPMorgan comes in at 15.5x, a proprietary estimate of what the PE should be after accounting for its earnings growth outlook, profitability, risk profile, industry, and market cap. This is more informative than a simple peer or industry comparison because it adjusts for JPMorgan's specific fundamentals rather than assuming all banks deserve the same multiple. With the actual PE of 15.4x sitting very close to the Fair Ratio, the stock appears fairly priced on this metric.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your JPMorgan Chase Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of JPMorgan Chase’s future to a concrete set of numbers and a fair value.

A Narrative is your story for the company, where you spell out how you think revenue, earnings, and profit margins will evolve, and the platform turns that story into a financial forecast and a Fair Value estimate.

On Simply Wall St, Narratives live in the Community page and are designed to be easy to use, so you can compare your Fair Value to today’s share price and decide whether JPMorgan looks like a buy, hold, or sell.

Because Narratives are updated dynamically as new earnings, news, or guidance arrives, they stay relevant and help you quickly see whether fresh information supports or contradicts your original story.

For example, one investor might have a bullish JPMorgan Narrative with a Fair Value near 350 dollars, based on strong digital growth and payments leadership. Another might take a more cautious view closer to 247 dollars, assuming slower revenue growth and margin pressure. The gap between those two stories is exactly what Narratives make clear.

For JPMorgan Chase, however, we will make it really easy for you with previews of two leading JPMorgan Chase Narratives:

Fair Value: $328.09 per share

Implied Upside vs Current Price: approximately 2.4% undervalued

Forecast Revenue Growth: 6.09%

- Analysts expect steady revenue growth and only modest margin compression, with earnings and EPS both rising into 2028, supported by diversified fee income and strong ROTCE.

- Management's ongoing investment in digital platforms, tokenization, and new business lines is seen as reinforcing JPMorgan's competitive moat and supporting structurally higher long term earnings.

- Consensus targets cluster in the low to mid $300s, suggesting the stock is close to fairly valued today but still offers some upside if execution remains strong and sector tailwinds persist.

Fair Value: $247.02 per share

Implied Downside vs Current Price: approximately 22.8% overvalued

Forecast Revenue Growth: 4.08%

- Higher credit loss allowances, rising operating expenses, and reserve builds point to mounting pressure on net and operating margins, which could weigh on future earnings.

- Expected rate cuts and a cautious investment banking outlook may constrain net interest income and advisory revenues, limiting profitability despite a solid recent performance.

- On these assumptions, the bearish fair value of about $247 sits well below the current share price. This implies that the market is pricing in more optimistic growth and margin resilience than this scenario allows.

Do you think there's more to the story for JPMorgan Chase? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com