Nasdaq

Nasdaq 华尔街日报

华尔街日报Returns On Capital Are Showing Encouraging Signs At Pan Asia Environmental Protection Group (HKG:556)

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So when we looked at Pan Asia Environmental Protection Group (HKG:556) and its trend of ROCE, we really liked what we saw.

Return On Capital Employed (ROCE): What Is It?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Pan Asia Environmental Protection Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

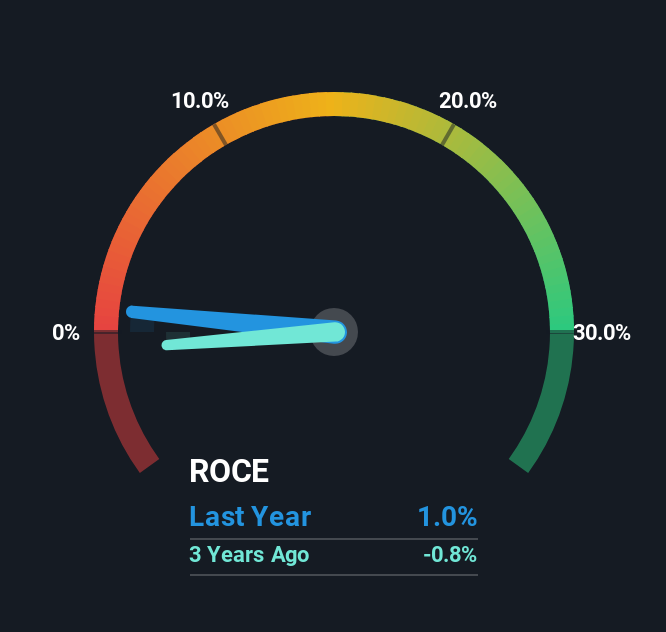

0.0095 = CN¥11m ÷ (CN¥1.3b - CN¥133m) (Based on the trailing twelve months to June 2025).

So, Pan Asia Environmental Protection Group has an ROCE of 1.0%. Ultimately, that's a low return and it under-performs the Commercial Services industry average of 7.1%.

See our latest analysis for Pan Asia Environmental Protection Group

Historical performance is a great place to start when researching a stock so above you can see the gauge for Pan Asia Environmental Protection Group's ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Pan Asia Environmental Protection Group.

The Trend Of ROCE

We're delighted to see that Pan Asia Environmental Protection Group is reaping rewards from its investments and has now broken into profitability. While the business was unprofitable in the past, it's now turned things around and is earning 1.0% on its capital. While returns have increased, the amount of capital employed by Pan Asia Environmental Protection Group has remained flat over the period. So while we're happy that the business is more efficient, just keep in mind that could mean that going forward the business is lacking areas to invest internally for growth. After all, a company can only become a long term multi-bagger if it continually reinvests in itself at high rates of return.

The Key Takeaway

In summary, we're delighted to see that Pan Asia Environmental Protection Group has been able to increase efficiencies and earn higher rates of return on the same amount of capital. Given the stock has declined 11% in the last five years, this could be a good investment if the valuation and other metrics are also appealing. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

One more thing to note, we've identified 2 warning signs with Pan Asia Environmental Protection Group and understanding these should be part of your investment process.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.