Nasdaq

Nasdaq 华尔街日报

华尔街日报Is Pega Stock Pricing In Too Much Growth After Its 233.7% Three Year Surge?

- Wondering if Pegasystems at around $59.63 is a smart buy or if the big gains are already behind it? You are not alone, and that is exactly what we are going to unpack here.

- The stock is up 28.3% year to date and 26.3% over the last year, but with a modest 4.9% gain over 30 days and a slight 0.8% dip in the last week, momentum is starting to look more nuanced.

- Investors have been reacting to a mix of product innovation, strategic customer wins, and ongoing buzz around AI driven workflow automation. All of these factors feed into expectations about Pegasystems long term growth runway. At the same time, renewed interest in software and cloud names has pulled more attention back to quality platform providers like Pegasystems, helping explain those strong multi year returns, including a 233.7% gain over three years.

- Despite that history, Pegasystems only scores a 2/6 valuation score, so we will walk through what different valuation methods are really saying about the stock, and then finish by looking at a more holistic way to judge whether the current price truly makes sense.

Pegasystems scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Pegasystems Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and then discounting those back to today, to reflect risk and the time value of money.

Pegasystems currently generates about $424.6 million in free cash flow, and analysts expect this to stay solid but gradually taper over time. Under Simply Wall St’s 2 Stage Free Cash Flow to Equity model, free cash flow is projected to be around $240.5 million by 2035, with earlier years (2026 to 2029) in the $308 million to $558 million range as growth normalizes. These longer dated figures are partly based on analyst estimates and then extrapolated further out.

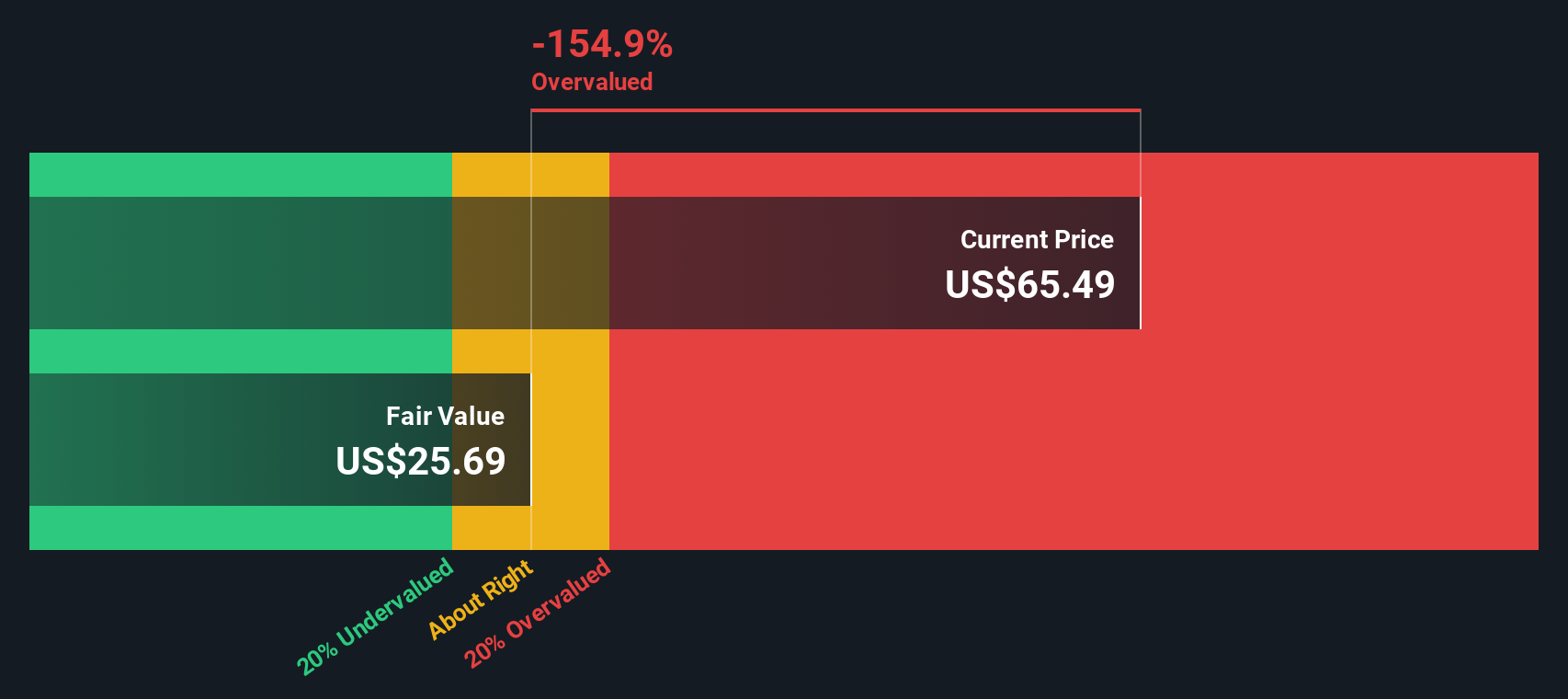

When all those future cash flows are discounted back, the model arrives at an intrinsic value of roughly $26.16 per share. Compared with today’s share price of approximately $59.63, the DCF suggests the stock is about 127.9% overvalued on this cash flow view.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pegasystems may be overvalued by 127.9%. Discover 908 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Pegasystems Price vs Earnings

For companies that are consistently profitable, the price to earnings (PE) ratio is often the go to yardstick because it directly links what you pay for the business to the profits it is already generating. A higher PE can be justified when investors expect faster earnings growth or see the business as relatively low risk, while slower growth or higher uncertainty usually calls for a lower, more conservative PE.

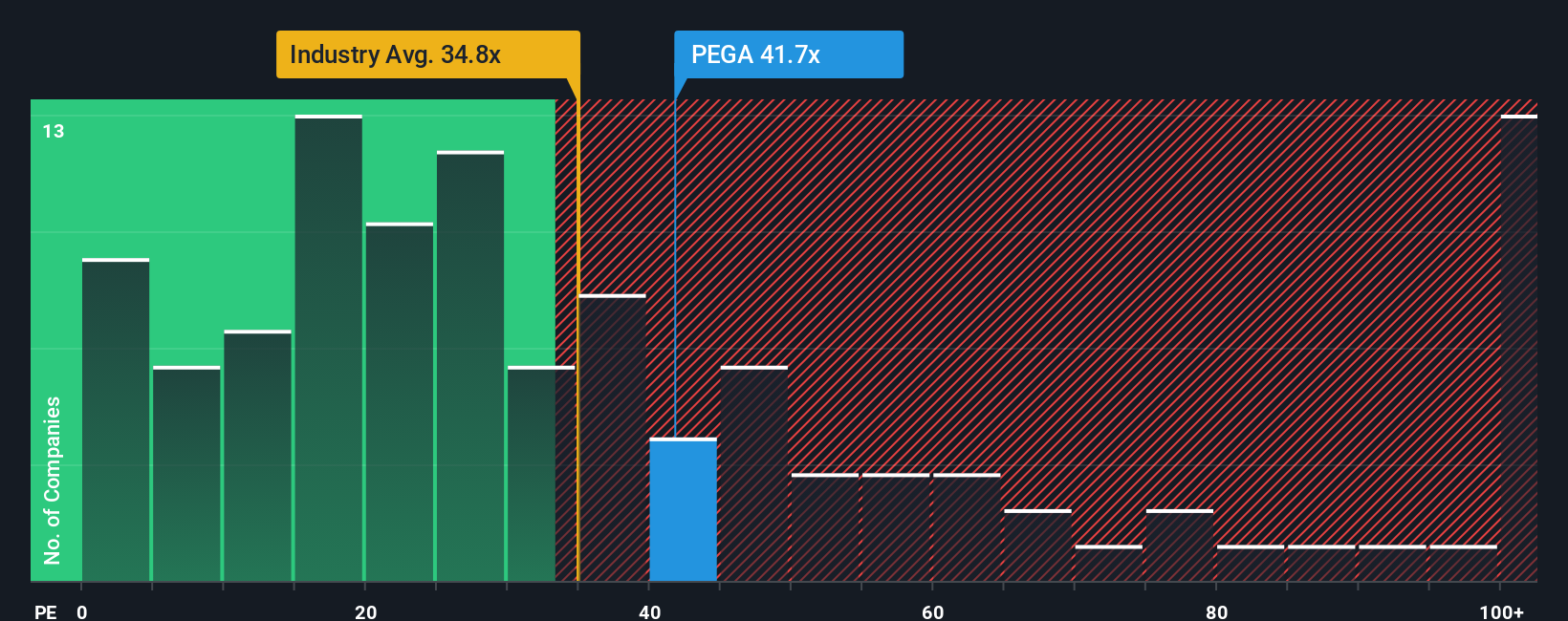

Pegasystems currently trades on a PE of about 36.4x. That is above the broader Software industry average of roughly 32.9x, but actually below the 42.7x average of closer listed peers. Simply Wall St also calculates a Fair Ratio of 28.8x for Pegasystems, which is the PE you might expect once you factor in its earnings growth outlook, profitability, risk profile, industry positioning and market cap.

This Fair Ratio is more tailored than a simple industry or peer comparison because it adjusts for Pegasystems specific strengths and weaknesses rather than assuming all software names deserve the same multiple. When set against the current 36.4x, the 28.8x Fair Ratio suggests Pegasystems is trading rich relative to what its fundamentals support, pointing to some valuation stretch.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1445 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pegasystems Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of the Pegasystems story with the numbers behind its future revenue, earnings, margins, and ultimately what you think the stock is worth.

A Narrative on Simply Wall St is your own story for a company. You spell out why you think its products, strategy, and industry position will play out a certain way, and the platform turns that perspective into a linked financial forecast and fair value estimate.

Narratives live on the Simply Wall St Community page, are easy to create and compare, and they help you make decisions by lining up each Narrative s Fair Value against today s share price. This makes it easier to see whether a given story suggests buy, hold, or sell.

Because Narratives update dynamically when new information such as earnings or product news is released, you can watch how bullish views on Pegasystems, such as those targeting around $78 per share, compare with more cautious perspectives closer to $40, and decide which story and valuation you find most convincing.

Do you think there's more to the story for Pegasystems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com