Nasdaq

Nasdaq 华尔街日报

华尔街日报Assessing Select Water Solutions (WTTR) Valuation After CEO John Schmitz’s Notable Insider Share Sale

Investors in Select Water Solutions (WTTR) are parsing a fresh insider move, as President and CEO John Schmitz just unloaded roughly 281,000 shares for about 3.1 million dollars, raising questions around management sentiment and timing.

See our latest analysis for Select Water Solutions.

That insider selling comes as the latest share price of $10.85 sits below earlier highs, with a 1 month share price return of 8.72 percent but a year to date share price return of negative 21.15 percent. At the same time, the 5 year total shareholder return of 175.27 percent still points to meaningful long term value creation, suggesting momentum has cooled recently rather than fully breaking the longer trend.

If this kind of insider activity has you reassessing your ideas, it could be a good moment to explore fast growing stocks with high insider ownership as a source of fresh, high conviction candidates.

With shares trading at a steep discount to analyst targets, but growth cooling and insiders cashing out, is Select Water Solutions quietly undervalued, or is the market already pricing in everything its future pipeline can deliver?

Most Popular Narrative Narrative: 24.3% Undervalued

Compared with the last close at $10.85, the most widely followed narrative argues that Select Water Solutions is worth materially more, setting up a tension between cautious earnings forecasts and a richer long term story.

The company has secured a substantial and growing backlog of long term, acreage dedicated water infrastructure contracts in the Northern Delaware Basin, providing high predictability on revenue and cash flows over multiple years, with further upside as undedicated and ROFR acreage is converted positioning Select to achieve significant Water Infrastructure revenue growth above $400 million annual exit run rate in 2026. This is likely to support sustainable top line growth and improved earnings visibility.

Curious how flat headline revenue expectations can still support a higher valuation and lower 7 point something discount rate, plus a richer future earnings multiple? The full narrative unpacks how margin expansion, contract visibility and a premium earnings multiple interact to justify a fair value well above today’s price.

Result: Fair Value of $14.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy exposure to oil and gas and large capital expenditure commitments could pressure cash flows and margins if demand or new contracts fall short.

Find out about the key risks to this Select Water Solutions narrative.

Another Way to Look at Value

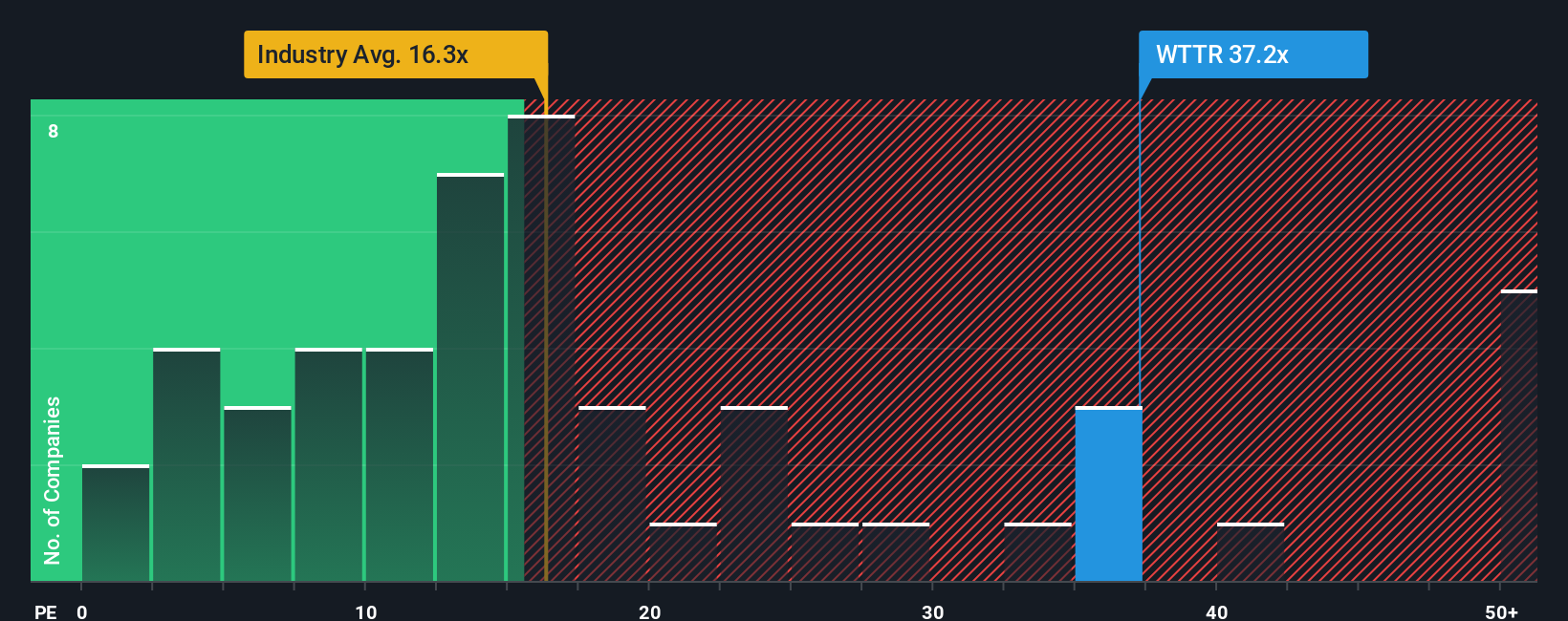

On earnings, the picture flips. WTTR trades on a steep 57.1 times price to earnings ratio, far above the US Energy Services average of 18.4 times and a fair ratio of 15.5 times, hinting at rich expectations. Is this a quality premium or valuation risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Select Water Solutions Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalized view in just minutes, Do it your way.

A great starting point for your Select Water Solutions research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next potential opportunity by checking focused stock ideas that can sharpen your watchlist and keep you ahead of the crowd.

- Capture powerful cash flow opportunities by targeting companies trading below their intrinsic value with these 908 undervalued stocks based on cash flows.

- Ride the wave of intelligent automation by zeroing in on breakthrough innovators using these 26 AI penny stocks.

- Strengthen your income stream by filtering for reliable payers through these 13 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com