Nasdaq

Nasdaq 华尔街日报

华尔街日报Is EA’s Strong 2025 Rally Justified After Go Private Deal Speculation?

- Wondering if Electronic Arts at around $203 a share is still a smart buy, or if the easy money has already been made? Let us unpack whether the current price really matches the long term value story.

- EA has quietly delivered a 39.6% gain year to date, with the stock up 29.9% over the last year and roughly 70.1% over three years, even if the last month has been a more modest 1.3% move and the last week has dipped slightly.

- Recently, investors have been digesting a mix of headlines around EA's live service franchises, new content updates for key sports titles, and evolving expectations for its pipeline of blockbuster releases. At the same time, broader market conversations about the resilience of gaming and interactive entertainment have helped frame EA as a relatively durable growth and cash flow story.

- Despite that strength, EA scores just 1/6 on our valuation checks, suggesting the stock does not screen as obviously undervalued on most traditional metrics right now. In the next sections, we will walk through different valuation approaches to see what they are missing, and finish with a more holistic way to think about EA's true worth.

Electronic Arts scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

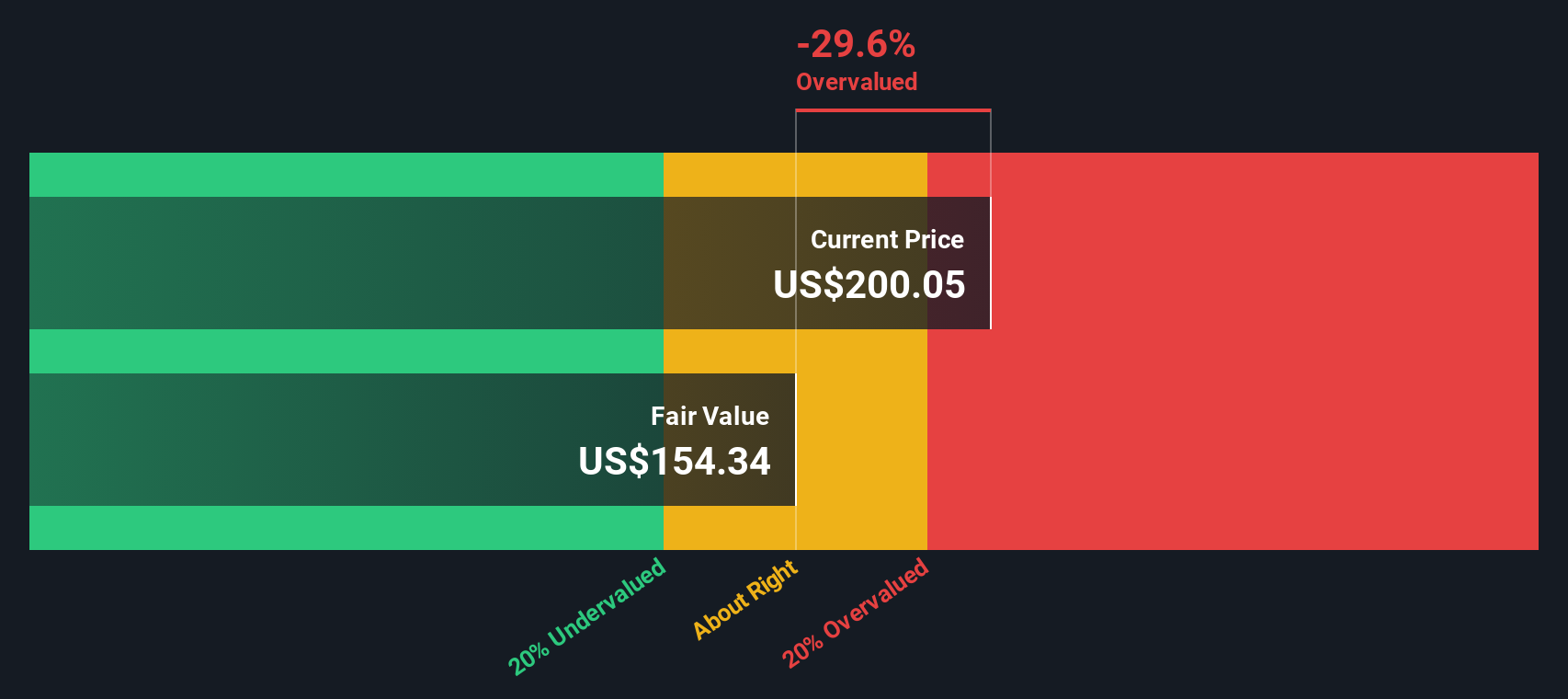

Approach 1: Electronic Arts Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in $ terms.

For Electronic Arts, the latest twelve month Free Cash Flow is about $1.67 billion. Analysts and the model project this to grow steadily, with forecast Free Cash Flow reaching around $2.89 billion by 2035, based on a 2 Stage Free Cash Flow to Equity approach that blends analyst estimates for the next few years with longer term extrapolations by Simply Wall St.

When all those future cash flows are discounted back to the present, the model arrives at an intrinsic value of roughly $150.40 per share. With the stock trading near $203, the DCF output implies EA is about 35.5% overvalued on this basis, indicating that investors today are paying a premium to the cash flows that can reasonably be expected.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Electronic Arts may be overvalued by 35.5%. Discover 908 undervalued stocks or create your own screener to find better value opportunities.

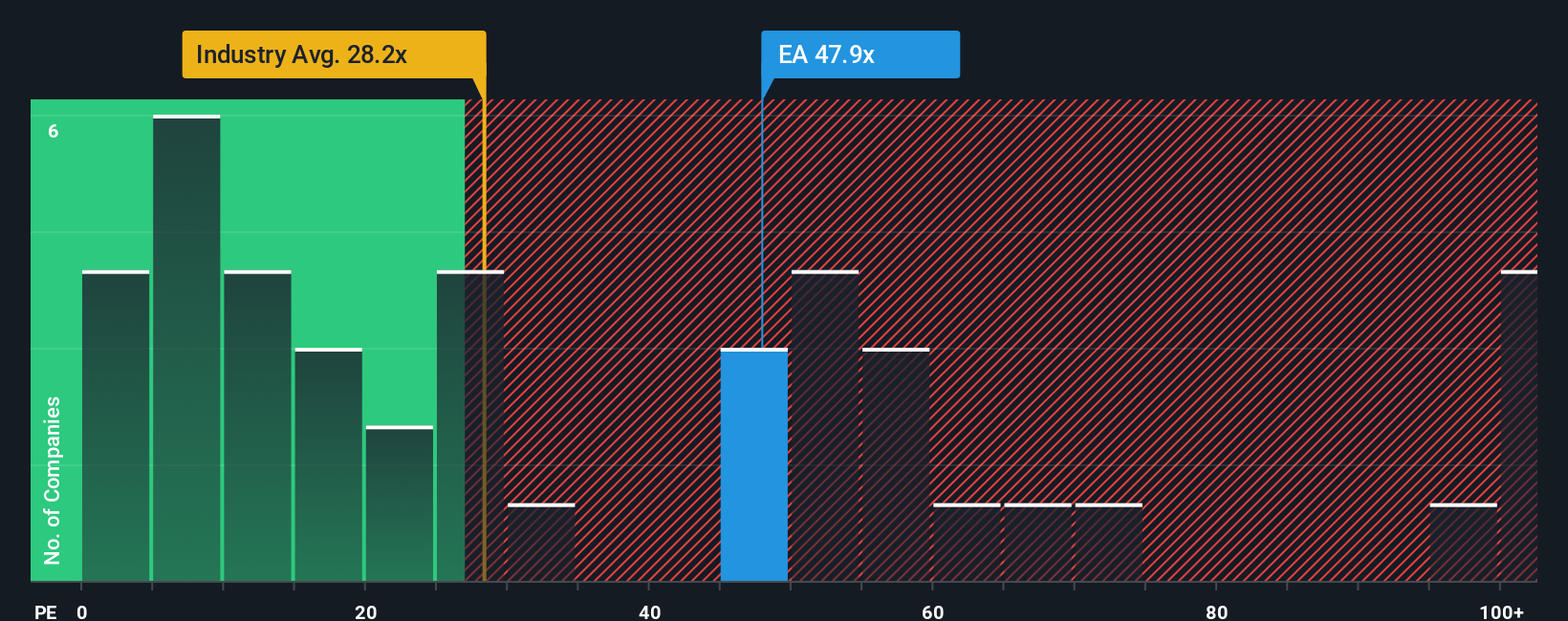

Approach 2: Electronic Arts Price vs Earnings

For profitable, established businesses like Electronic Arts, the Price to Earnings ratio is often the cleanest shorthand for what investors are willing to pay for each dollar of current profits. It naturally captures how the market weighs a company’s growth prospects against the risks in its business model and cash flows.

In general, faster and more predictable earnings growth can justify a higher PE multiple, while slower growth or higher uncertainty should pull that multiple down. Today, EA trades at about 57.4x earnings, above both the wider Entertainment industry average of roughly 20.3x and the peer group average of around 73.1x. This suggests investors are already pricing in solid growth and resilience.

Simply Wall St’s Fair Ratio framework refines this comparison by estimating what a reasonable PE should be for EA specifically, given its earnings growth outlook, profitability, size, industry positioning and risk profile. That Fair Ratio comes out at about 25.8x, which is much lower than EA’s current 57.4x. On this more tailored basis, the stock screens as richly valued rather than merely in line with peers.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1445 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Electronic Arts Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simple stories that investors build on Simply Wall St’s Community page to connect their view of a company’s future revenue, earnings and margins to a concrete forecast and Fair Value. Investors can then constantly update those views as fresh news or earnings arrive and compare them to the live share price to decide whether to buy, hold or sell. For Electronic Arts, that could mean one Narrative assuming the go private deal at around $210 sets a firm ceiling on upside, while another assumes the current Fair Value of roughly $202.36 already captures long term growth. The power of Narratives is that both perspectives can coexist side by side, quantified and transparent, giving you an easy, dynamic and accessible way to see how your own story about EA stacks up against other investors and whether today’s price really matches the future you believe in.

Do you think there's more to the story for Electronic Arts? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com