Nasdaq

Nasdaq 华尔街日报

华尔街日报Morningstar (MORN) Valuation Check as the Stock Drops Roughly 36% Year to Date

Recent Performance Sets the Stage

Morningstar (MORN) has been quietly lagging the market this year, with the share price down about 36% year to date and roughly 39% over the past year, inviting a closer look at what investors might be missing.

See our latest analysis for Morningstar.

After a tough stretch that has pushed the share price down sharply year to date, recent 1 month share price stability hints that sentiment may be stabilizing, even as the 1 year total shareholder return remains firmly negative. This suggests fading momentum but potential mispricing for patient investors.

If Morningstar's reset has you rethinking where to hunt for returns, it could be a good moment to explore fast growing stocks with high insider ownership for other compelling ideas.

With shares sharply off their highs despite steady revenue and earnings growth, investors now face a key question: Is Morningstar trading at a meaningful discount to its fundamentals, or is the market already pricing in its future expansion?

Price-to-Earnings of 23.4x: Is it justified?

Morningstar's latest close at $214.10 implies a price-to-earnings ratio of 23.4x, which screens as modestly cheap versus peers but rich against its own fair multiple.

The price-to-earnings ratio compares the current share price to the company’s earnings per share, making it a core yardstick for valuing profitable capital markets businesses like Morningstar. A lower P E can hint that the market is not fully crediting earnings power, while a higher one implies investors are paying up for growth, quality, or both.

Against the US Capital Markets industry average of 25.4x and a broader peer average of 28x, Morningstar’s 23.4x multiple looks restrained, suggesting the market is not assigning a premium despite high quality earnings and strong return on equity of 24.8 percent. However, compared with the estimated fair P E of 14.2x implied by our regression based fair ratio work, the current 23.4x stands well above the level valuation could migrate toward if sentiment or growth expectations cool.

Explore the SWS fair ratio for Morningstar

Result: Price-to-Earnings of 23.4x (OVERVALUED)

However, slower revenue growth or a prolonged derating in high multiple tech and data names could pressure Morningstar’s premium valuation and delay multiple expansion.

Find out about the key risks to this Morningstar narrative.

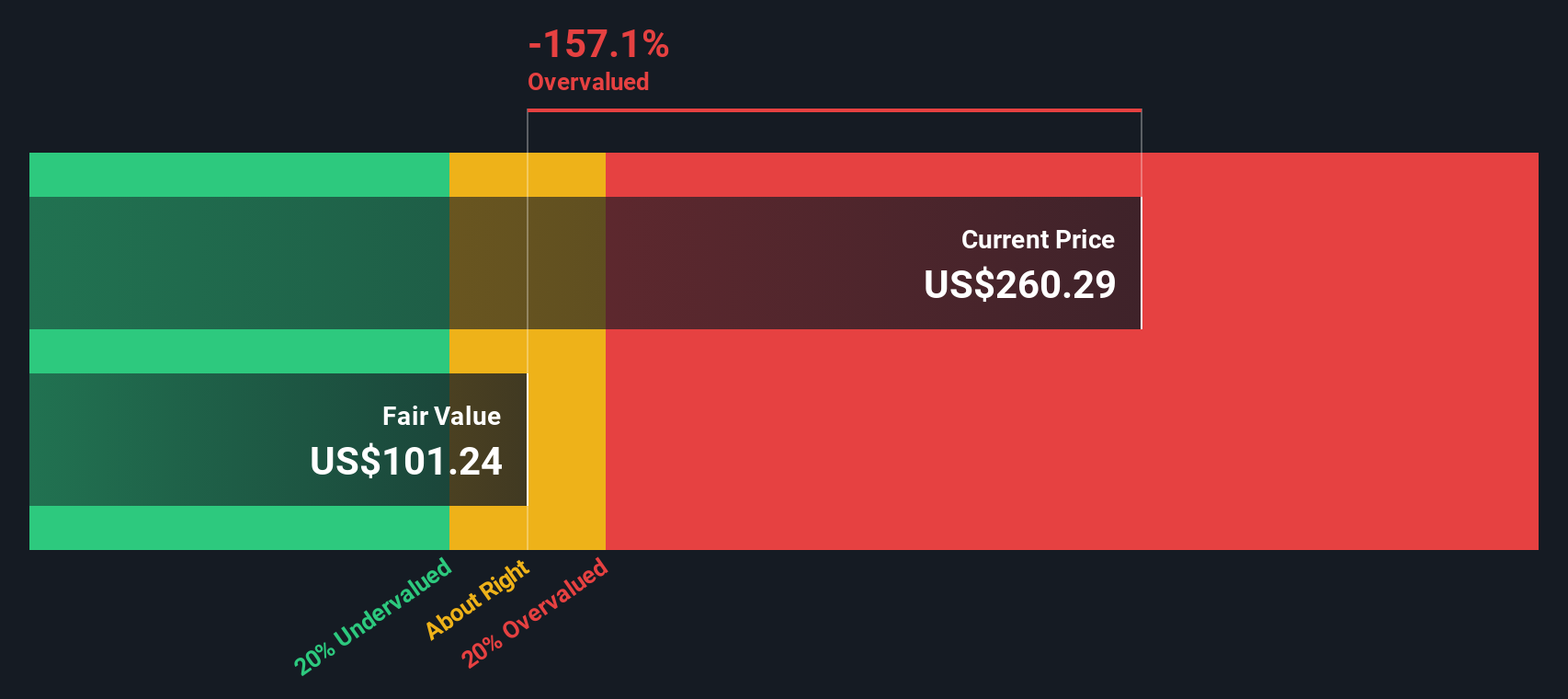

Another View: DCF Paints a Harsher Picture

While the earnings multiple makes Morningstar look only modestly expensive, our DCF model is far less forgiving. It suggests fair value closer to $94 versus the current $214. That implies the stock could be materially overvalued and raises the question of which lens investors should trust.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Morningstar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Morningstar Narrative

If you see the story differently or would rather reach your own conclusions from the numbers, you can build a personalized view in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Morningstar.

Looking for more investment ideas?

If Morningstar feels fully priced, consider using focused screeners to upgrade your watchlist with higher conviction ideas rather than waiting while other opportunities move.

- Target potential multi baggers early by scanning these 3612 penny stocks with strong financials that already show real businesses, real revenue, and improving fundamentals.

- Ride structural growth in automation and data by filtering for these 26 AI penny stocks positioned to monetize AI adoption instead of just talking about it.

- Seek attractive entry points with these 908 undervalued stocks based on cash flows that flag quality companies the market is currently mispricing based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com