Nasdaq

Nasdaq 华尔街日报

华尔街日报Assessing Vizsla Silver (TSX:VZLA)’s Valuation Following Its Positive Panuco Feasibility Study Announcement

Vizsla Silver (TSX:VZLA) has jumped back onto investors radar after highlighting a positive feasibility study for its Panuco silver gold project in Mexico, even as the latest quarter showed another net loss.

See our latest analysis for Vizsla Silver.

The feasibility study buzz has helped keep sentiment upbeat, and despite the latest quarterly loss the 30 day share price return of 10.84% and standout 1 year total shareholder return of 175.38% suggest momentum is still building around Vizsla’s long term growth story.

If this kind of speculative upside has your attention, it could be worth exploring fast growing stocks with high insider ownership for more fast moving names with strong alignment between insiders and shareholders.

With the shares up sharply and trading at a modest discount to analyst targets despite ongoing losses, the market clearly likes Panuco’s potential, but is Vizsla Silver still mispriced or already reflecting years of future growth?

Price-to-Book of 4x: Is it justified?

Based on a price-to-book ratio of 4x at the last close of CA$7.16, Vizsla Silver trades richer than the broader Canadian metals and mining space but cheaper than its closest high growth peers.

The price-to-book multiple compares the company’s market value to its net assets, a common yardstick for asset heavy miners where earnings are still negative. For an early stage explorer developer like Vizsla, a premium multiple often signals that investors are already capitalising future discoveries and production rather than current balance sheet strength.

In Vizsla’s case, the 4x price-to-book sits well above the Canadian metals and mining industry average of 2.8x. This implies the market is assigning a sizable premium for the Panuco project and its growth prospects. Yet that same 4x multiple remains meaningfully below the 13.4x average of its closest peers. This suggests investors are willing to pay up for the story, but not at the extremely elevated levels seen elsewhere in the high growth exploration cohort.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-book of 4x (ABOUT RIGHT)

However, investors should still weigh permitting or development delays and ongoing net losses, any of which could quickly erode confidence in the current valuation.

Find out about the key risks to this Vizsla Silver narrative.

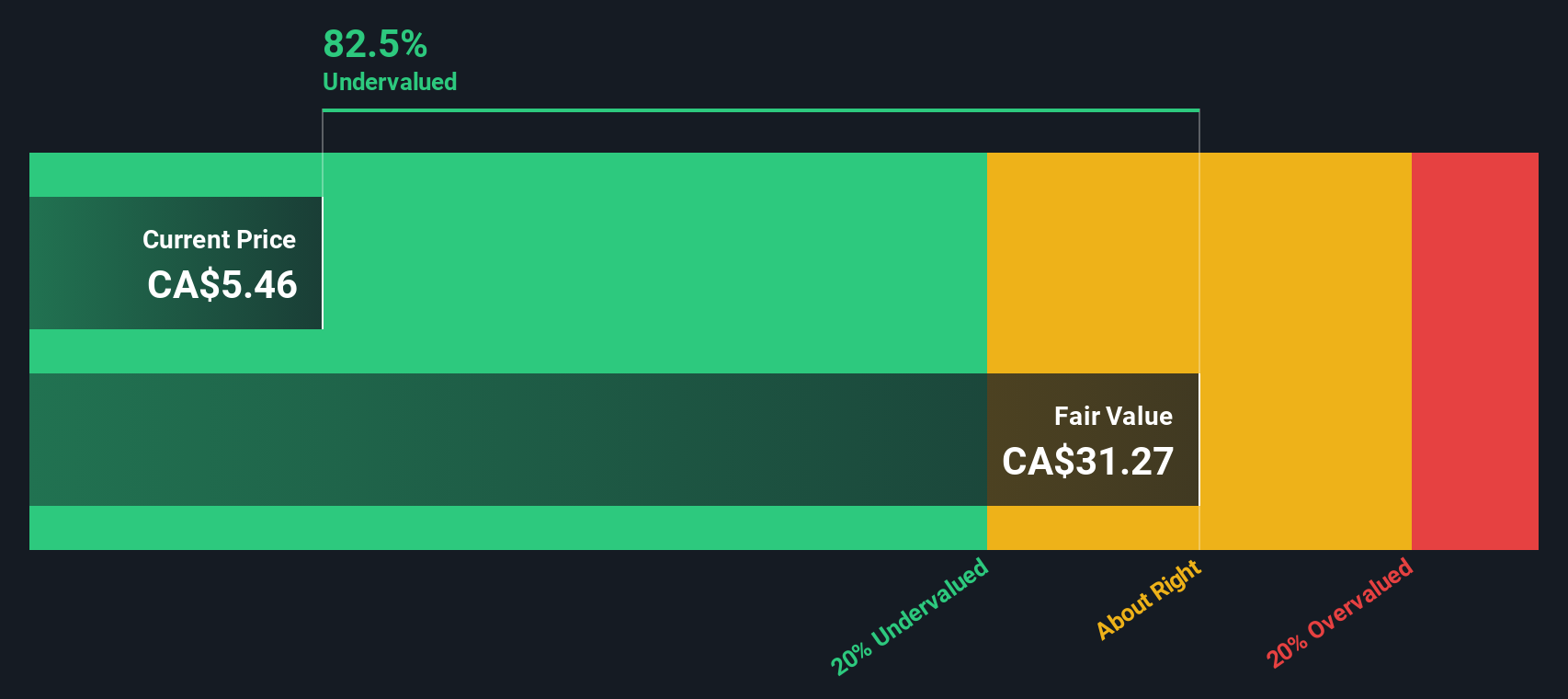

Another View: DCF Points to Deeper Value

While the 4x price to book suggests Vizsla Silver is roughly fairly priced against peers, our DCF model presents a different view, indicating fair value around CA$24.90, or roughly 71% above today’s CA$7.16 share price. Is the market underestimating Panuco’s long term cash potential?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Vizsla Silver for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Vizsla Silver Narrative

If you see the numbers differently or want to dig into the details yourself, you can build a personalised view in just minutes: Do it your way.

A great starting point for your Vizsla Silver research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by scanning a few targeted stock lists on Simply Wall Street that could sharpen your portfolio edge.

- Capture early stage potential by reviewing these 3612 penny stocks with strong financials that pair tiny market caps with balance sheets strong enough to support the next leg of growth.

- Position your money where innovation meets healthcare outcomes by using these 30 healthcare AI stocks to focus on companies applying intelligent tools to real medical problems.

- Strengthen your income stream by targeting these 13 dividend stocks with yields > 3% that offer yields above 3% without throwing risk management out the window.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com