Nasdaq

Nasdaq 华尔街日报

华尔街日报RIAS (CPH:RIAS B) Will Pay A Smaller Dividend Than Last Year

RIAS A/S' (CPH:RIAS B) dividend is being reduced from last year's payment covering the same period to DKK26.00 on the 26th of January. However, the dividend yield of 3.9% is still a decent boost to shareholder returns.

RIAS' Projected Earnings Seem Likely To Cover Future Distributions

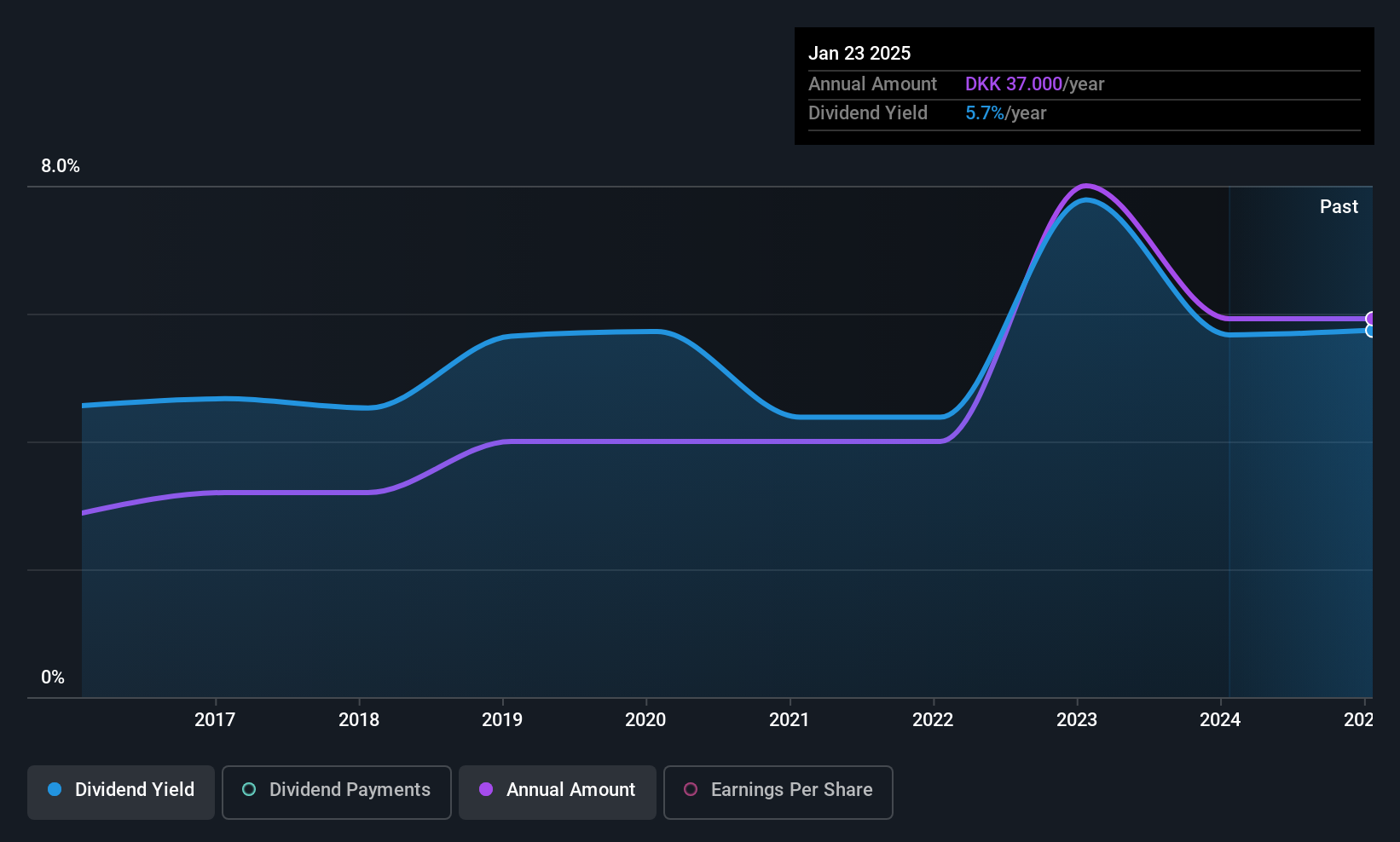

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. RIAS was earning enough to cover the previous dividend, but it was paying out quite a large proportion of its free cash flows. The company is clearly earning enough to pay this type of dividend, but it is definitely focused on returning cash to shareholders, rather than growing the business.

If the trend of the last few years continues, EPS will grow by 2.3% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio will be 66%, which is in the range that makes us comfortable with the sustainability of the dividend.

View our latest analysis for RIAS

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The dividend has gone from an annual total of DKK20.00 in 2015 to the most recent total annual payment of DKK26.00. This works out to be a compound annual growth rate (CAGR) of approximately 2.7% a year over that time. Modest growth in the dividend is good to see, but we think this is offset by historical cuts to the payments. It is hard to live on a dividend income if the company's earnings are not consistent.

Dividend Growth May Be Hard To Achieve

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Earnings per share has been crawling upwards at 2.3% per year. Growth of 2.3% may indicate that the company has limited investment opportunity so it is returning its earnings to shareholders instead. While this isn't necessarily a negative, it definitely signals that dividend growth could be constrained in the future unless earnings start to pick up again.

In Summary

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. While RIAS is earning enough to cover the dividend, we are generally unimpressed with its future prospects. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, RIAS has 3 warning signs (and 1 which is a bit unpleasant) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.