Nasdaq

Nasdaq 华尔街日报

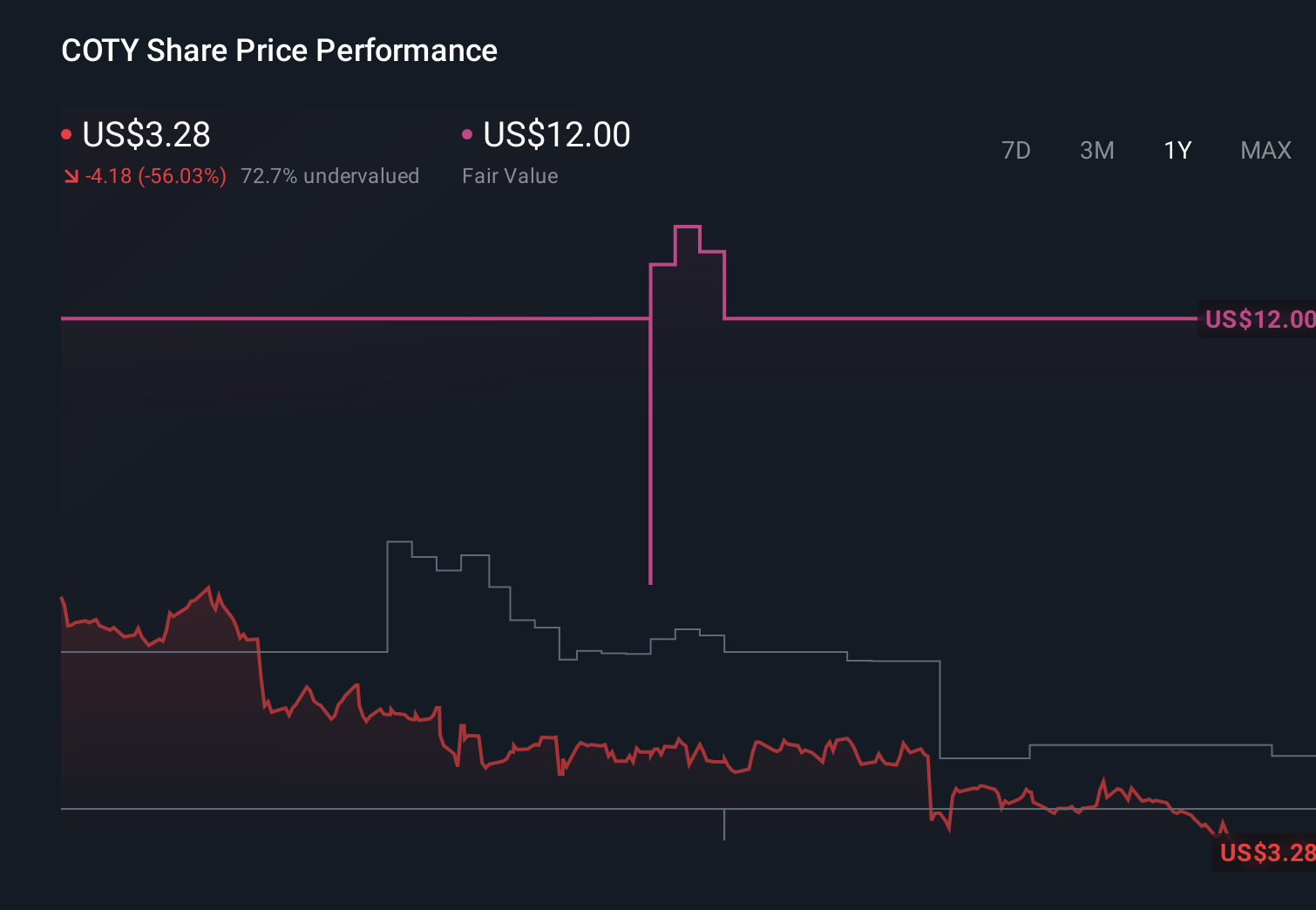

华尔街日报Coty (COTY) Is Down 6.7% After Leadership Shake-Up Raises Questions On Long-Term Strategy

- Coty’s controlling shareholder JAB Holdings has moved to overhaul the beauty group’s leadership, prompting chair Peter Harf to step down and signaling the expected departure of CEO Sue Nabi after a period of weak performance.

- This reshuffle raises fresh questions about how quickly new leadership can clarify Coty’s long-term direction, particularly around its ongoing strategic review and category growth priorities.

- Next, we’ll examine how this leadership shake-up might influence Coty’s investment narrative, including its plan to restore profitable growth.

Find companies with promising cash flow potential yet trading below their fair value.

Coty Investment Narrative Recap

To own Coty today, you need confidence that its fragrance and beauty brands can return to profitable growth despite recent losses, inventory destocking, and high competition. The JAB-driven leadership overhaul heightens uncertainty around execution in the near term, but does not yet change the key short term catalyst of stabilizing sales trends or the main risk around balance sheet flexibility and margins.

The most relevant recent update is management’s guidance that sales and EBITDA should improve in the second half of 2026, helped by cost savings from the All-in to Win program and ongoing fragrance innovation. How the incoming leadership team treats this plan, especially around cost discipline and brand investment, will be central to whether Coty can move from pressured earnings to the profitability trajectory many investors are hoping for.

But while those upside drivers are important, investors should also be aware of the risk that high debt levels and refinancing needs could...

Read the full narrative on Coty (it's free!)

Coty’s narrative projects $6.1 billion revenue and $302.1 million earnings by 2028.

Uncover how Coty's forecasts yield a $4.83 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community value Coty between US$3.69 and US$9.35 per share, highlighting very different expectations. You can weigh those views against the execution risk around Coty’s leadership transition and its plan to restore profitable growth.

Explore 5 other fair value estimates on Coty - why the stock might be worth over 2x more than the current price!

Build Your Own Coty Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com