Nasdaq

Nasdaq 华尔街日报

华尔街日报Assessing OSG (TSE:6136)’s Valuation After Its Recent Share Price Momentum

OSG (TSE:6136) has quietly pushed higher, with the stock up about 4% over the past week and more than 14% in the past 3 months, catching the attention of value-focused investors.

See our latest analysis for OSG.

That recent 3 month share price return of 14.08% builds on solid year to date momentum of 28.40% and a robust 1 year total shareholder return of 41.86%. This suggests investors are steadily pricing in OSG’s earnings resilience rather than chasing short lived spikes.

If OSG’s move has you thinking more broadly about where capital goods demand might surprise next, it could be worth exploring fast growing stocks with high insider ownership as a potential fresh ideas list.

Yet with OSG trading slightly above analyst targets but still showing a sizeable intrinsic discount, the key question is whether the market is overlooking further upside or has already priced in its next leg of growth.

Price-to-Earnings of 14.5x: Is it justified?

OSG’s last close of ¥2,353.5 equates to a 14.5x price to earnings multiple, which screens as slightly expensive versus peers and the wider machinery sector.

The price to earnings ratio compares what investors pay today for each unit of current earnings. It can be a useful gauge for mature, profitable industrial businesses like OSG. With earnings forecast to grow in the mid single digits per year and return on equity expected to remain below 10%, the current premium multiple suggests the market is paying up for stability rather than rapid expansion.

However, that premium looks stretched when set against the benchmarks. OSG trades on 14.5x earnings compared with a 13.4x fair price to earnings level implied by our fair ratio work, a 12.7x average for the Japanese machinery industry and a 14.1x peer average. This points to investors assigning OSG a richer valuation than both its own fundamentals and sector norms might justify.

Explore the SWS fair ratio for OSG

Result: Price-to-Earnings of 14.5x (OVERVALUED)

However, risks remain, including softer global capital spending or weaker automotive and aerospace demand, which could pressure OSG’s mid single digit growth assumptions.

Find out about the key risks to this OSG narrative.

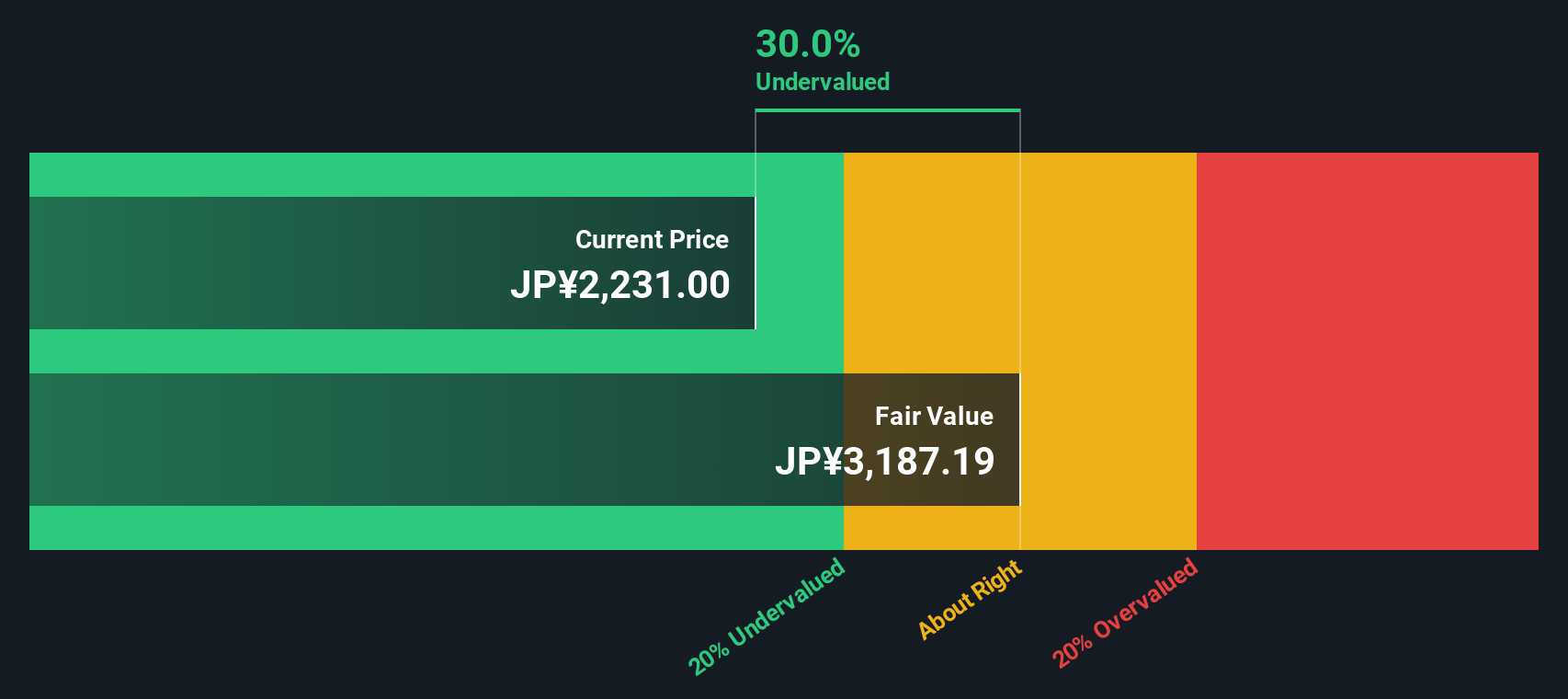

Another View: What Does Our DCF Say?

While the 14.5x price to earnings ratio hints at a rich valuation, our DCF model paints a different picture, suggesting fair value of ¥3,102.77 versus a market price of ¥2,353.5. That 24.1% gap implies the market may be underestimating OSG’s cash flow durability, not overhyping it.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OSG for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 903 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OSG Narrative

If you see the story differently or want to stress test these assumptions with your own inputs, you can construct a custom view in under three minutes with Do it your way.

A great starting point for your OSG research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

OSG might be compelling, but you will regret stopping here when you could quickly uncover fresh opportunities tailored to your strategy with the Simply Wall St Screener.

- Capitalize on mispriced opportunities by scanning these 903 undervalued stocks based on cash flows that the market has not fully appreciated yet.

- Ride the AI transformation wave by targeting these 26 AI penny stocks poised to benefit from accelerating adoption across industries.

- Strengthen your passive income stream by focusing on these 13 dividend stocks with yields > 3% that can potentially support long term wealth building.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com