Nasdaq

Nasdaq 华尔街日报

华尔街日报Is AWS Security Hub Integration Reshaping The Investment Case For Varonis Systems (VRNS)?

- In early December 2025, Varonis Systems, Inc. announced a new integration with AWS Security Hub designed to unify risk visibility, automate remediation, and strengthen data-centric threat detection across AWS environments and broader data estates.

- This integration highlights how Varonis is deepening its role in cloud and unstructured data security by cutting alert noise and directly fixing misconfigurations, a combination that could be particularly important for resource-constrained security teams.

- Now we’ll examine how this AWS Security Hub integration, especially its automated remediation capabilities, may influence Varonis’ evolving investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Varonis Systems Investment Narrative Recap

To own Varonis, you need to believe its data security platform can turn strong SaaS ARR and product breadth into durable profitability despite ongoing losses and dilution. The new AWS Security Hub integration supports that thesis by sharpening its cloud value proposition, but it does not materially change the near term pressure from negative margins and the risk that larger security platforms and hyperscalers squeeze its growth and pricing power.

Among recent announcements, the FedRAMP authorization for Varonis’ cloud native data security posture management stands out as particularly relevant, because it anchors the same end to end, data centric story behind the AWS integration. Together, these steps reinforce a key catalyst: if enterprises increasingly consolidate data security budgets around platforms that can both find and fix risk in automated fashion, Varonis’ expanded coverage across regulated and cloud workloads could become more important to its long term growth case.

But against that opportunity, investors should be aware that growing pressure from larger platform vendors could...

Read the full narrative on Varonis Systems (it's free!)

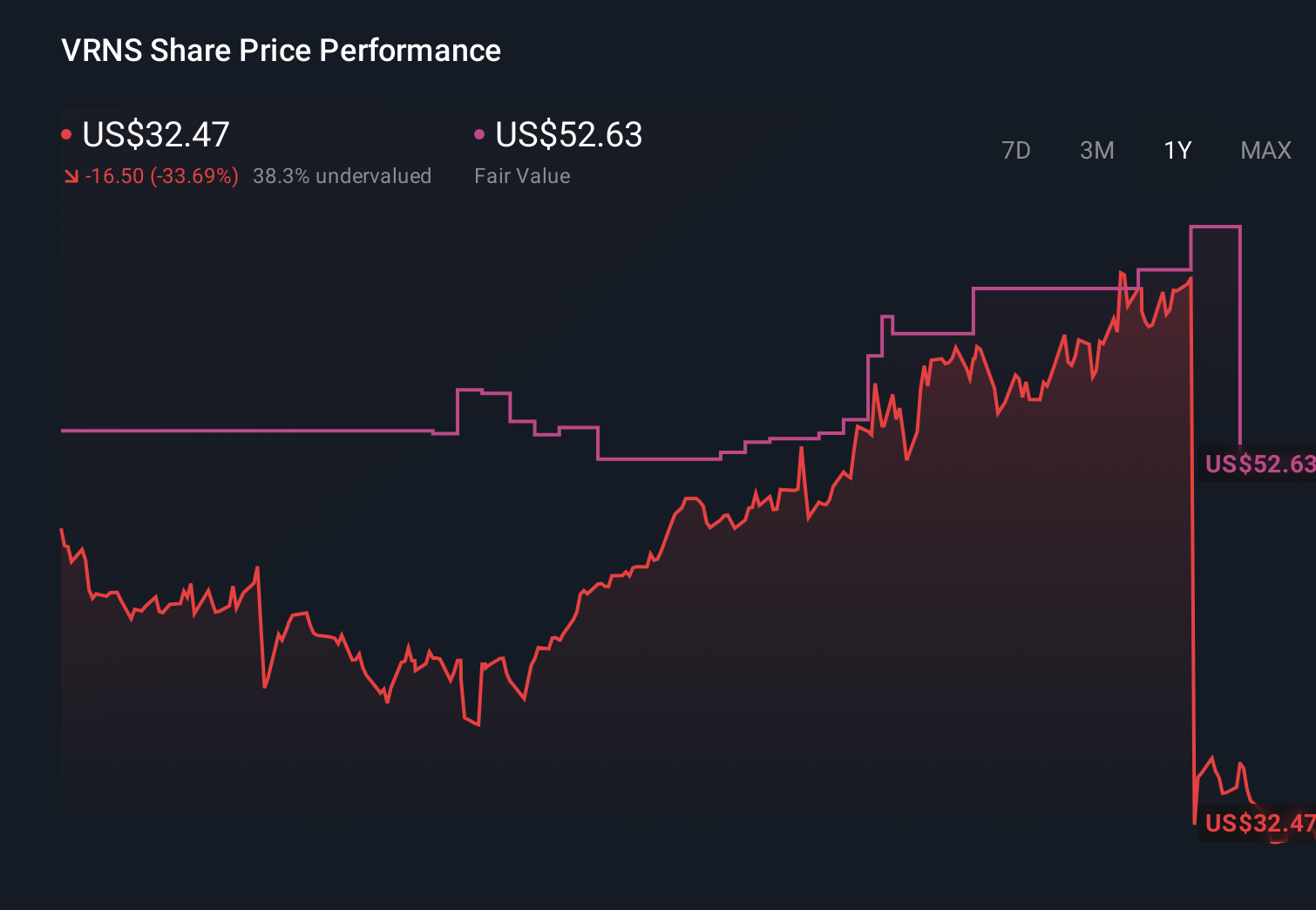

Varonis Systems’ narrative projects $911.4 million revenue and $119.3 million earnings by 2028.

Uncover how Varonis Systems' forecasts yield a $52.63 fair value, a 67% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates cluster between US$52.63 and US$70, suggesting many see upside from recent prices. You should weigh these views against the risk that sector wide budget consolidation toward larger security platforms could limit how fully Varonis converts product momentum into future earnings power.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth just $52.63!

Build Your Own Varonis Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Varonis Systems research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com