Nasdaq

Nasdaq 华尔街日报

华尔街日报How Investors Are Reacting To Graco (GGG) Dividend Hike And Expanded Share Buyback Plan

- In early December 2025, Graco Inc. announced a 7.3% increase in its regular quarterly dividend to US$0.295 per share, payable on February 4, 2026, to shareholders of record as of January 19, 2026.

- Alongside this dividend increase, Graco’s board authorized a substantial new share repurchase program of up to 15 million shares, supplementing an existing buyback plan that still has nearly 8 million shares available.

- Next, we’ll examine how Graco’s expanded share repurchase authorization could influence its investment narrative and expectations for shareholder returns.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

Graco Investment Narrative Recap

To own Graco, you generally need to believe in its ability to keep generating solid cash flows from niche fluid handling and contractor equipment while managing tariff and margin pressures. The dividend hike and larger buyback support the existing narrative but do not materially change the near term catalysts around new Contractor product launches or the key risk that weaker professional paint and EMEA demand could pressure volumes and pricing.

The expanded authorization to repurchase up to 15 million shares, on top of nearly 8 million remaining under the 2018 plan, directly ties into the existing catalyst that active buybacks can support earnings per share. How effectively this capital return interacts with acquisitions, tariff mitigation actions and inventory management will be important for investors tracking margin resilience and the durability of shareholder returns.

But investors also need to be aware that exposure to softer professional paint demand and EMEA markets could still...

Read the full narrative on Graco (it's free!)

Graco's narrative projects $2.7 billion revenue and $641.7 million earnings by 2028. This requires 7.9% yearly revenue growth and about a $159 million earnings increase from $482.6 million today.

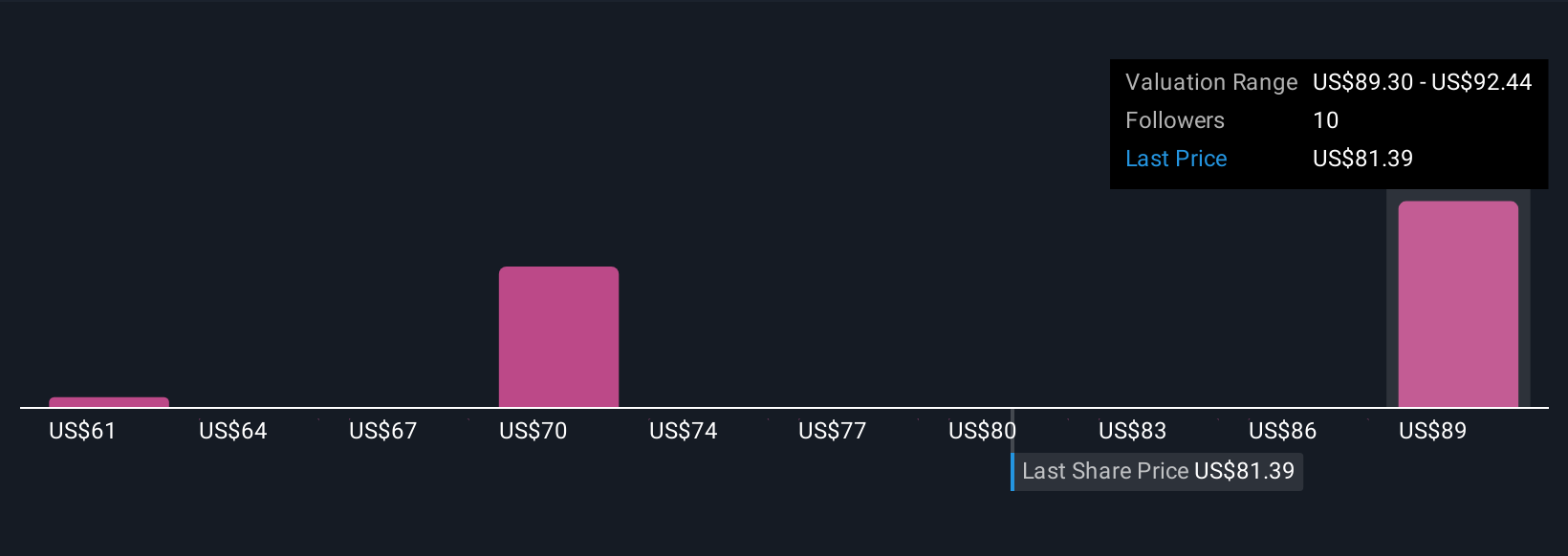

Uncover how Graco's forecasts yield a $92.44 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$61 to about US$92 per share, showing how far apart views can be. Set against this, concerns over tariff impacts and margin pressure remind you to weigh those opinions against the operational risks that could affect Graco’s ability to sustain shareholder returns.

Explore 4 other fair value estimates on Graco - why the stock might be worth 27% less than the current price!

Build Your Own Graco Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Graco research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Graco research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Graco's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com