Nasdaq

Nasdaq 华尔街日报

华尔街日报How Investors Are Reacting To Immatics (IMTX) $125 Million Follow-On Equity Offering

- Immatics N.V. recently announced a follow-on equity offering, issuing 12,500,000 ordinary shares at US$10.00 each to raise about US$125,000,000 in gross proceeds, with the deal expected to close on December 8, 2025, subject to customary conditions.

- The involvement of Jefferies, Leerink Partners, and Cantor as joint book-running managers highlights the scale of the financing and the company’s access to capital markets.

- We’ll now examine how this sizeable capital raise, and the associated share issuance, could shape Immatics’ broader investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

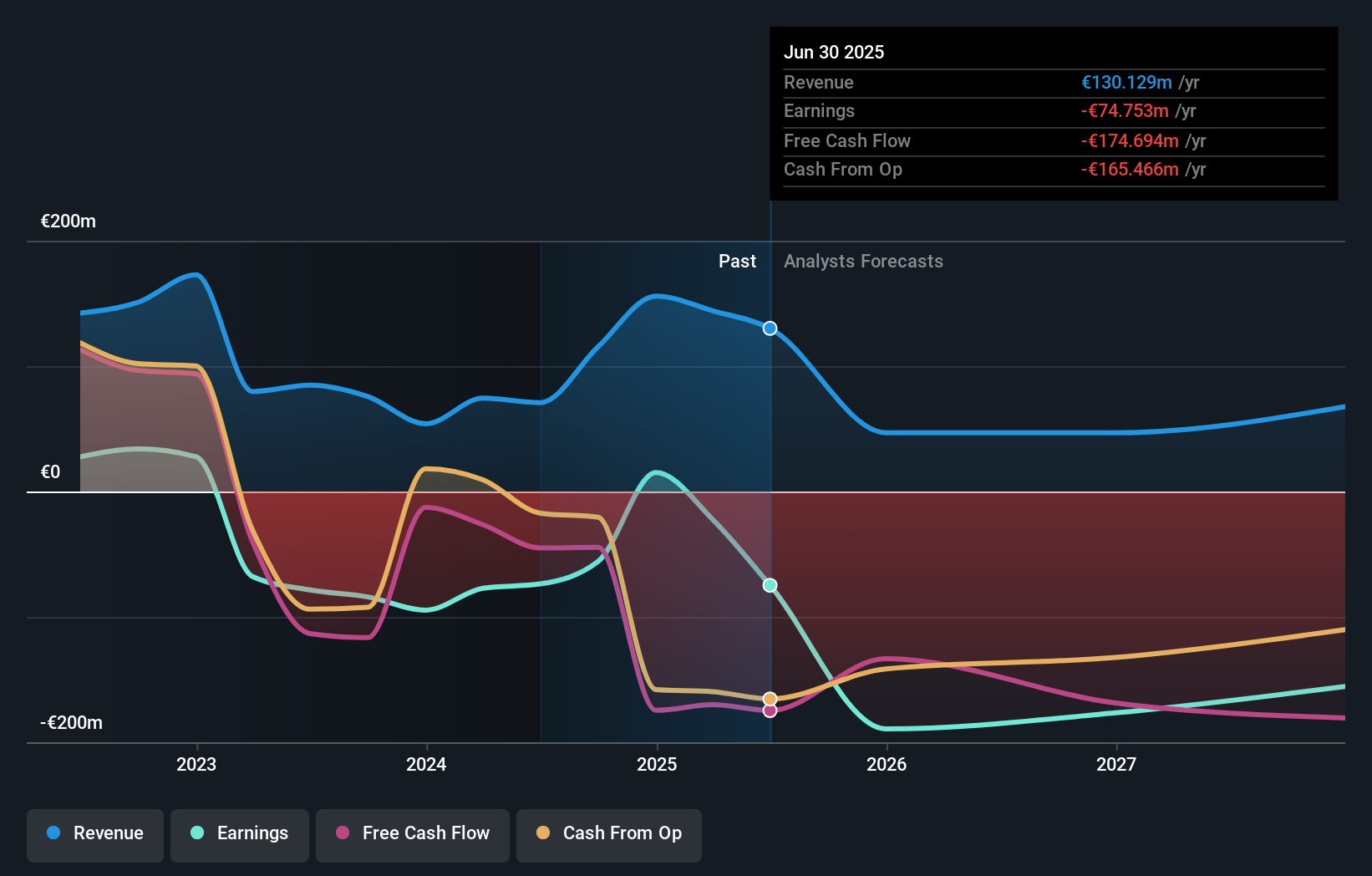

What Is Immatics' Investment Narrative?

To own Immatics today, you really have to believe that its T-cell therapies can eventually justify heavy ongoing losses and a rich revenue multiple, and that the recent equity raise simply buys more time to prove that out. The new US$125,000,000 offering meaningfully extends the cash runway at a moment when quarterly net losses have widened sharply, which could ease near term financing risk even as it dilutes existing holders. That extra capital may help keep clinical and partnership catalysts on track rather than forcing program cuts, but it also raises the bar for future data and deal updates to support the larger share base. In other words, the story becomes less about survival and more about execution risk from here.

However, this improved funding position brings its own dilution and execution risks that investors should understand. The valuation report we've compiled suggests that Immatics' current price could be inflated.Exploring Other Perspectives

Explore 4 other fair value estimates on Immatics - why the stock might be worth less than half the current price!

Build Your Own Immatics Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Immatics research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Immatics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Immatics' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com