Nasdaq

Nasdaq 华尔街日报

华尔街日报Should Unum’s New US$1 Billion Buyback Amid Earnings Miss Require Action From Unum Group (UNM) Investors?

- In December 2025, Unum Group announced that its Board had approved a share repurchase program of up to US$1.00 billion of its outstanding common stock, shortly after reporting third-quarter 2025 operating net income of US$2.09 per share that missed analyst expectations due to higher expenses and weaker benefit ratios.

- This combination of an earnings miss and a large buyback authorization highlights management’s effort to balance near-term profitability pressures with a continued focus on returning capital to shareholders.

- We’ll now examine how Unum’s sizable new buyback authorization may reshape its existing investment narrative around growth, margins, and capital deployment.

Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

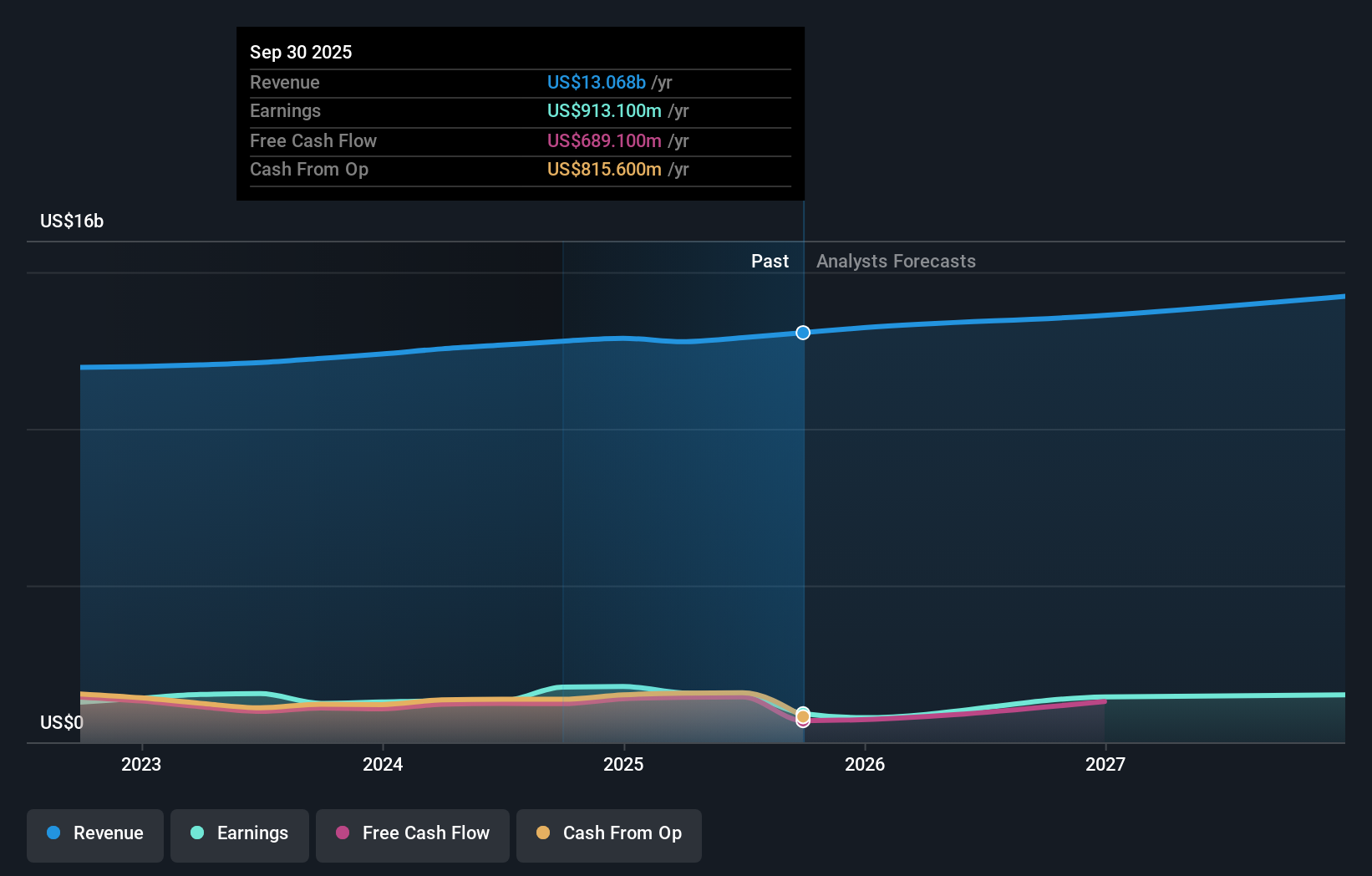

Unum Group Investment Narrative Recap

To own Unum Group, you need to be comfortable with a traditional insurance business that converts steady premium income into capital returns, while managing benefit and claims volatility. The new US$1.00 billion buyback, announced alongside an earnings miss tied to higher expenses and weaker benefit ratios, does not materially change the near term story: the key catalyst remains stabilizing benefit ratios, while the biggest risk is that elevated claims trends continue to pressure margins.

The most relevant recent development alongside the buyback is Unum’s pattern of dividend increases, including the ~10% bump to US$0.460 per share in mid 2025. Together, rising dividends and a sizable repurchase authorization signal that management is continuing to allocate substantial capital to shareholders even as earnings come under pressure from weaker benefit ratios and softer near term expectations.

Yet investors should also be aware that if elevated benefit ratios persist for longer than expected, it could...

Read the full narrative on Unum Group (it's free!)

Unum Group's narrative projects $14.5 billion revenue and $1.6 billion earnings by 2028.

Uncover how Unum Group's forecasts yield a $93.08 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community span roughly US$93 to US$166 per share, showing how far apart individual assessments can be. Set against this wide range, the current pressure from higher expenses and weaker benefit ratios invites you to weigh how such margin risks could influence Unum’s future performance and to compare several different viewpoints before deciding what the stock is worth.

Explore 5 other fair value estimates on Unum Group - why the stock might be worth over 2x more than the current price!

Build Your Own Unum Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Unum Group research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Unum Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Unum Group's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com