Nasdaq

Nasdaq 华尔街日报

华尔街日报Is V.F (VFC) Turning Sector Tailwinds and Philanthropy Into a Stronger Brand Moat?

- Earlier this week, VF Corp benefited from stronger sector sentiment after Zara-owner Inditex reported 2.7% sales growth over the first nine months of its fiscal year, reinforcing evidence of resilient consumer demand for apparel.

- Separately, the VF Foundation’s nearly US$3 million in global Giving Tuesday grants underscored the company’s focus on social impact, sustainability, and community engagement as part of its broader brand positioning.

- We’ll now examine how renewed confidence in apparel demand, reflected in Inditex’s results, may influence VF Corp’s existing investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

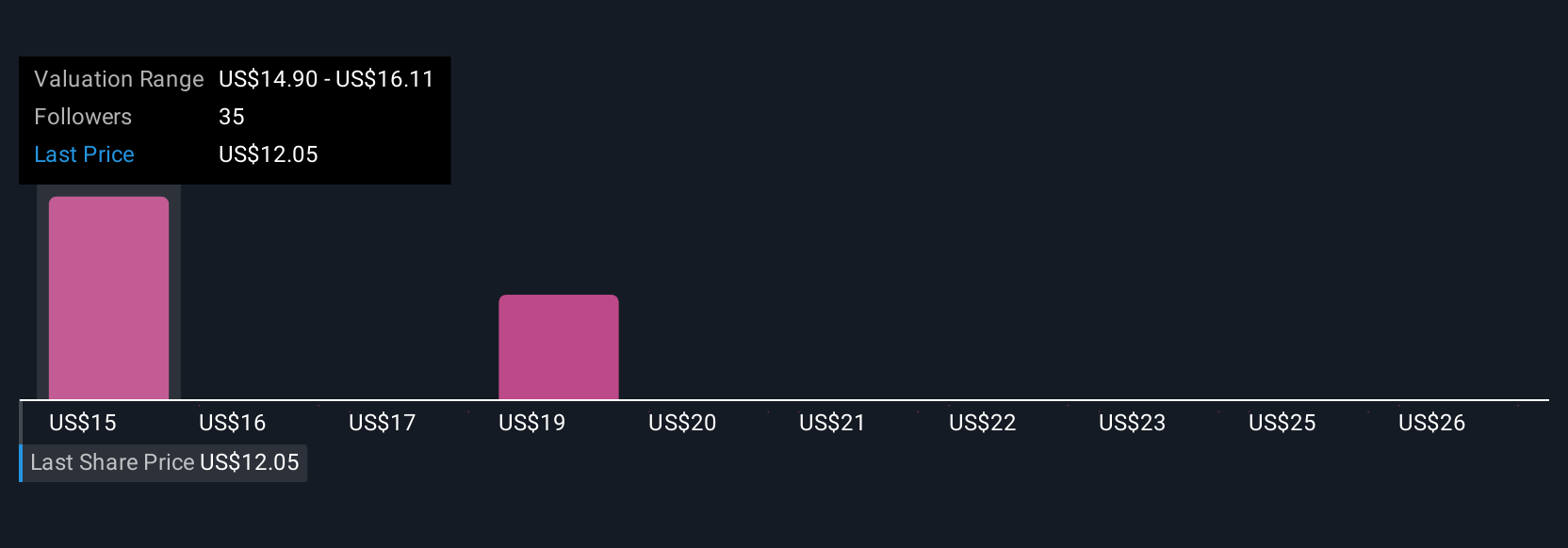

V.F Investment Narrative Recap

To own V.F. Corp, you need to believe its core outdoor and lifestyle brands can offset Vans’ drag and that execution on its turnaround and cost reset will stick. Inditex’s resilient sales support the idea that apparel demand is holding up, but this does not meaningfully change the near term focus on fixing Vans and managing leverage, which remain the key catalyst and risk.

The VF Foundation’s nearly US$3 million Giving Tuesday commitment is most relevant here, because it reinforces brand equity and consumer trust at a time when V.F. is trying to refocus on higher quality, more profitable growth channels and rebuild momentum across its strongest franchises.

Yet investors should also weigh how ongoing tariff headwinds and already pressured margins could interact with...

Read the full narrative on V.F (it's free!)

V.F's narrative projects $10.3 billion revenue and $571.3 million earnings by 2028. This requires 2.6% yearly revenue growth and about a $466 million earnings increase from $104.9 million today.

Uncover how V.F's forecasts yield a $16.05 fair value, a 16% downside to its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community currently see V.F. Corp’s fair value between US$10 and about US$27.85, underlining how far views can stretch. Against that backdrop, concerns about Vans’ persistent double digit revenue declines take on added importance for anyone assessing the company’s longer term earnings power.

Explore 8 other fair value estimates on V.F - why the stock might be worth 48% less than the current price!

Build Your Own V.F Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your V.F research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free V.F research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate V.F's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com