Nasdaq

Nasdaq 华尔街日报

华尔街日报How Activist Demands To Halt Deals And Oust CEO At KeyCorp (KEY) Has Changed Its Investment Story

- On December 5, 2025, activist investor Holdco Asset Management urged KeyCorp to halt acquisitions, prioritize share buybacks, overhaul its board, and replace Chairman and CEO Christopher Gorman, citing value destruction from the 2016 First Niagara deal and calling for an independent capital allocation committee.

- By openly contemplating a proxy contest or even a sale of KeyCorp to larger peers, Holdco has put unusual public pressure on the bank’s 200-year-old franchise and its current leadership.

- We’ll now examine how Holdco’s push for a no-acquisition policy and concentrated capital return could reshape KeyCorp’s investment narrative.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

KeyCorp Investment Narrative Recap

To own KeyCorp, you need to believe in a regional bank that can grow earnings while keeping credit quality and capital levels under control. Holdco’s activism raises near term uncertainty around leadership and capital allocation, but it does not directly change the core fundamental catalyst of earnings growth or the key risk of asset quality and higher capital requirements.

The most relevant recent update alongside this activism is KeyCorp’s reaffirmation of its common dividend at US$0.205 per share throughout 2025, signaling ongoing capital return even as its capital framework comes under fresh scrutiny. How management balances dividend continuity, potential buybacks and any higher regulatory buffers is likely to sit at the center of the coming debate with Holdco and other shareholders.

Yet investors should be aware that rising regulatory capital demands could still constrain payouts and growth if...

Read the full narrative on KeyCorp (it's free!)

KeyCorp's narrative projects $7.7 billion revenue and $2.4 billion earnings by 2027. This requires 10.5% yearly revenue growth and about a $1.7 billion earnings increase from $716.0 million today.

Uncover how KeyCorp's forecasts yield a $21.51 fair value, a 12% upside to its current price.

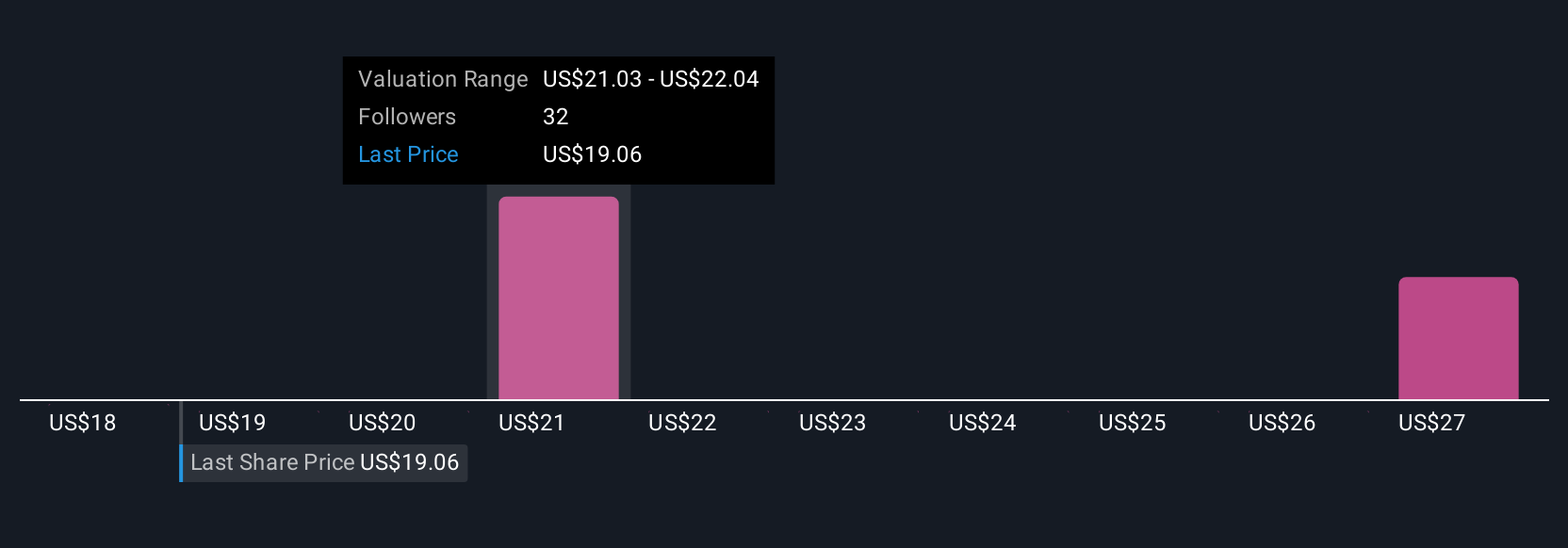

Exploring Other Perspectives

Three members of the Simply Wall St Community see fair value for KeyCorp between US$21.51 and US$31.94, showing a broad range of expectations. You may want to weigh those views against the risk that higher stress capital buffers could limit KeyCorp’s flexibility on dividends and buybacks in the years ahead.

Explore 3 other fair value estimates on KeyCorp - why the stock might be worth just $21.51!

Build Your Own KeyCorp Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your KeyCorp research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free KeyCorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate KeyCorp's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com