Nasdaq

Nasdaq 华尔街日报

华尔街日报Why Paymentus Holdings (PAY) Is Up 6.7% After Fresh Analyst Upgrades On Its SaaS Bill-Pay Platform

- Recently, Freedom Capital Markets initiated coverage on Paymentus Holdings with a Buy rating, while other brokerage firms also raised their views on the cloud-based bill payment provider’s Software-as-a-Service platform.

- This wave of analyst enthusiasm highlights growing attention on Paymentus’ role in enabling electronic bill presentment and payments across multiple industries and channels.

- Next, we’ll explore how this fresh analyst coverage could influence Paymentus’ investment narrative, particularly around its perceived growth runway.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Paymentus Holdings Investment Narrative Recap

To own Paymentus, you need to believe electronic bill payment will keep expanding and that its SaaS platform can convert that shift into durable transaction growth and improving profitability. The recent wave of analyst upgrades, including Freedom Capital Markets’ new coverage, mostly reinforces existing optimism rather than changing the key near term story, which still hinges on sustaining high growth while managing margin pressure from larger, price sensitive enterprise customers.

The upcoming appearance by CEO Dushyant Sharma and CFO Sanjay Kalra at the Wolfe Research Small and Mid-Cap Conference may give investors more color on how Paymentus plans to balance rapid enterprise wins with profitability, especially given its premium valuation multiples. Any clearer commentary on contribution margins or pricing trends could matter more for the stock’s near term narrative than the analyst ratings themselves.

Yet while enthusiasm is rising, investors should be aware that growing reliance on large enterprise clients...

Read the full narrative on Paymentus Holdings (it's free!)

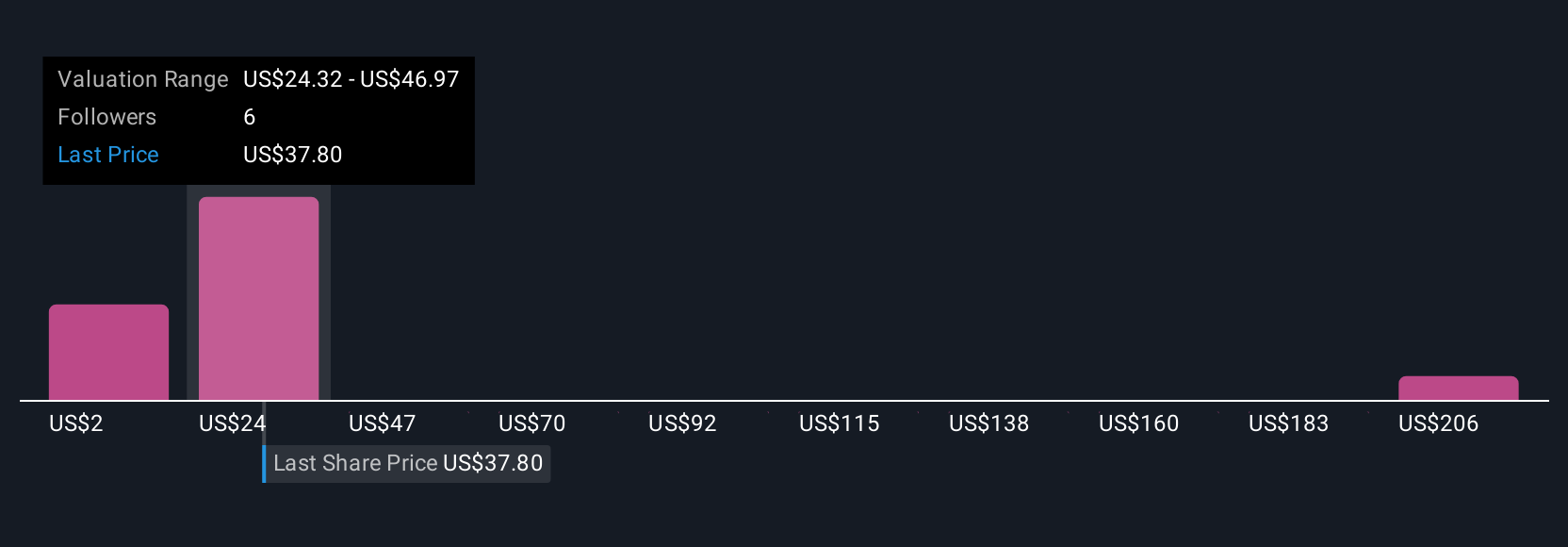

Paymentus Holdings' narrative projects $1.8 billion revenue and $125.3 million earnings by 2028. This requires 19.0% yearly revenue growth and about a $69 million earnings increase from $56.1 million today.

Uncover how Paymentus Holdings' forecasts yield a $38.00 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently place Paymentus’ fair value anywhere between about US$2.88 and US$228.15, underscoring how far apart views can be. Set against this, the recent focus on Paymentus’ ability to serve large, high volume billers highlights why some investors are watching margin resilience just as closely as top line growth.

Explore 4 other fair value estimates on Paymentus Holdings - why the stock might be worth less than half the current price!

Build Your Own Paymentus Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Paymentus Holdings research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Paymentus Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paymentus Holdings' overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com