Nasdaq

Nasdaq 华尔街日报

华尔街日报How Rising Short Interest At F.N.B (FNB) Has Changed Its Investment Story

- Recently released data show that F.N.B. Corp’s short interest climbed, with about 15.36 million shares sold short, representing 5.69% of its free float.

- This rise in bearish positioning highlights growing investor skepticism, which can fuel both downside pressure and the potential for sharper reversals if sentiment shifts.

- With short interest now meaningfully higher, we’ll explore how this changing sentiment interacts with F.N.B.’s existing investment narrative and risk profile.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

F.N.B Investment Narrative Recap

To own F.N.B., you need to believe that its regional banking model, digital investments and diversified fee income can offset concentration, CRE and cost pressures over time. The recent rise in short interest does not materially change the core near term story, but it does heighten the risk of sentiment driven volatility around credit quality and regional economic data.

Against this backdrop, the board’s decision on 12 November 2025 to affirm another US$0.12 quarterly dividend is especially relevant, as it signals ongoing confidence in earnings and capital strength. For investors, that dividend track record sits alongside the main catalysts of digital expansion and Southeast market growth, but it also has to be weighed against the persistent risks from commercial real estate exposure and higher technology related expenses.

Yet beneath the surface, the concentration in Mid Atlantic and Southeast markets is a risk investors should be aware of as...

Read the full narrative on F.N.B (it's free!)

F.N.B's narrative projects $2.2 billion revenue and $775.6 million earnings by 2028. This requires 13.0% yearly revenue growth and about a $308.6 million earnings increase from $467.0 million today.

Uncover how F.N.B's forecasts yield a $18.56 fair value, a 10% upside to its current price.

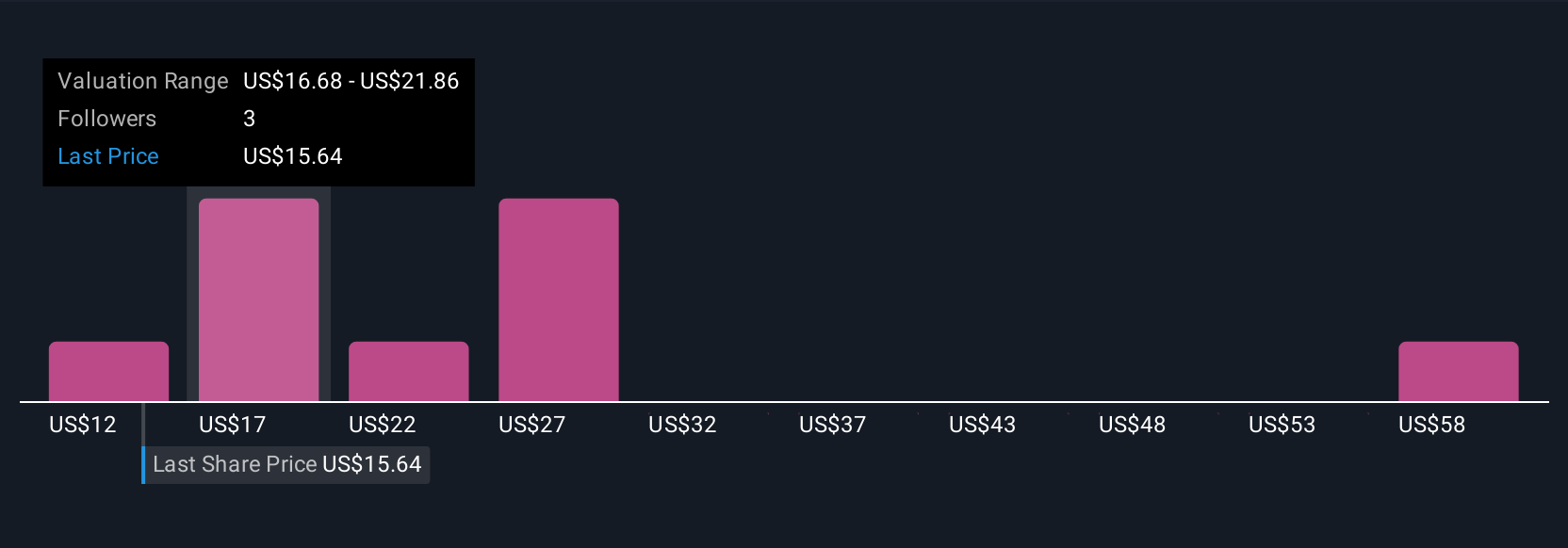

Exploring Other Perspectives

Four members of the Simply Wall St Community currently see F.N.B.'s fair value between US$18.56 and US$63.31, reflecting very different expectations. Set those views against the bank's ongoing exposure to commercial real estate and regional economic swings, and you can see why it pays to compare several perspectives before deciding where F.N.B. might fit in your portfolio.

Explore 4 other fair value estimates on F.N.B - why the stock might be worth over 3x more than the current price!

Build Your Own F.N.B Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your F.N.B research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free F.N.B research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate F.N.B's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com