Nasdaq

Nasdaq 华尔街日报

华尔街日报Is Dutch Bros Share Price Justified After Strong Multi Year Run In 2025?

- If you are wondering whether Dutch Bros at around $61 a share is a caffeine fueled bargain or just pricey buzz, this article is for you. We are going to unpack what the current market price really implies about its future.

- The stock has quietly kept the momentum going, up about 5% over the last week, 12.3% over the past month, and roughly 12.9% over the last year, compounding into an 87.2% gain over three years.

- Behind those moves, Dutch Bros has been steadily expanding its store footprint across new and existing markets while doubling down on its drive thru focused model. Many investors see this as a scalable growth engine. At the same time, ongoing menu innovation and brand building campaigns have helped keep traffic resilient even as consumers become more value conscious.

- Despite that growth story, Dutch Bros only scores 1/6 on our valuation checks, suggesting the market may already be pricing in a lot of optimism. Next, we will walk through different valuation approaches to see whether that score is justified, before finishing with a more holistic way to think about what this stock is truly worth.

Dutch Bros scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

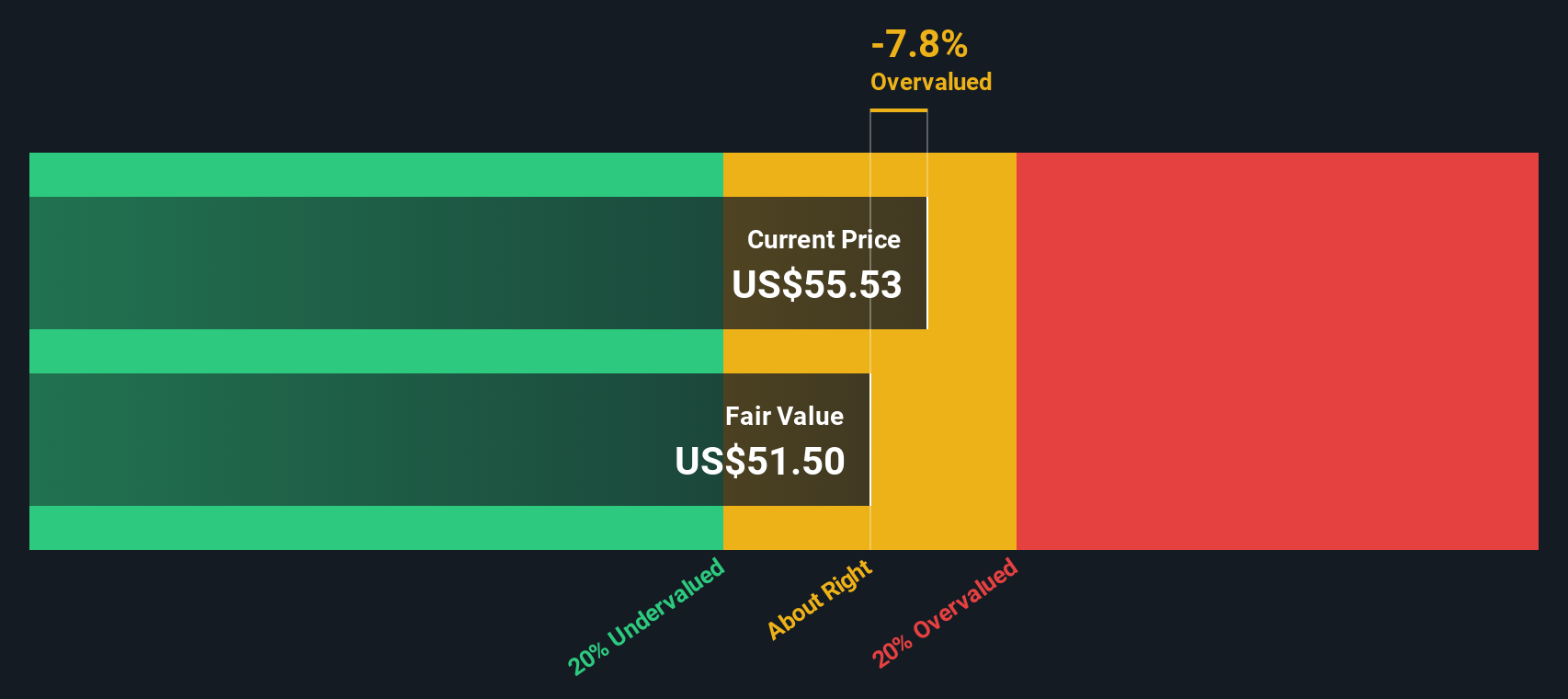

Approach 1: Dutch Bros Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today using a required rate of return.

For Dutch Bros, the latest twelve month Free Cash Flow is slightly negative at about $6 million, reflecting heavy reinvestment in new shops rather than mature, steady cash generation. Analysts expect this to turn around quickly, with Free Cash Flow projected to reach roughly $81 million by 2026 and, based on Simply Wall St extrapolations, rising toward about $696 million by 2035.

When those future cash flows are discounted back using a 2 Stage Free Cash Flow to Equity model, the estimated intrinsic value comes out at about $47.40 per share. With the stock currently trading around $61, that implies Dutch Bros is roughly 29.1% overvalued on this DCF view.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dutch Bros may be overvalued by 29.1%. Discover 912 undervalued stocks or create your own screener to find better value opportunities.

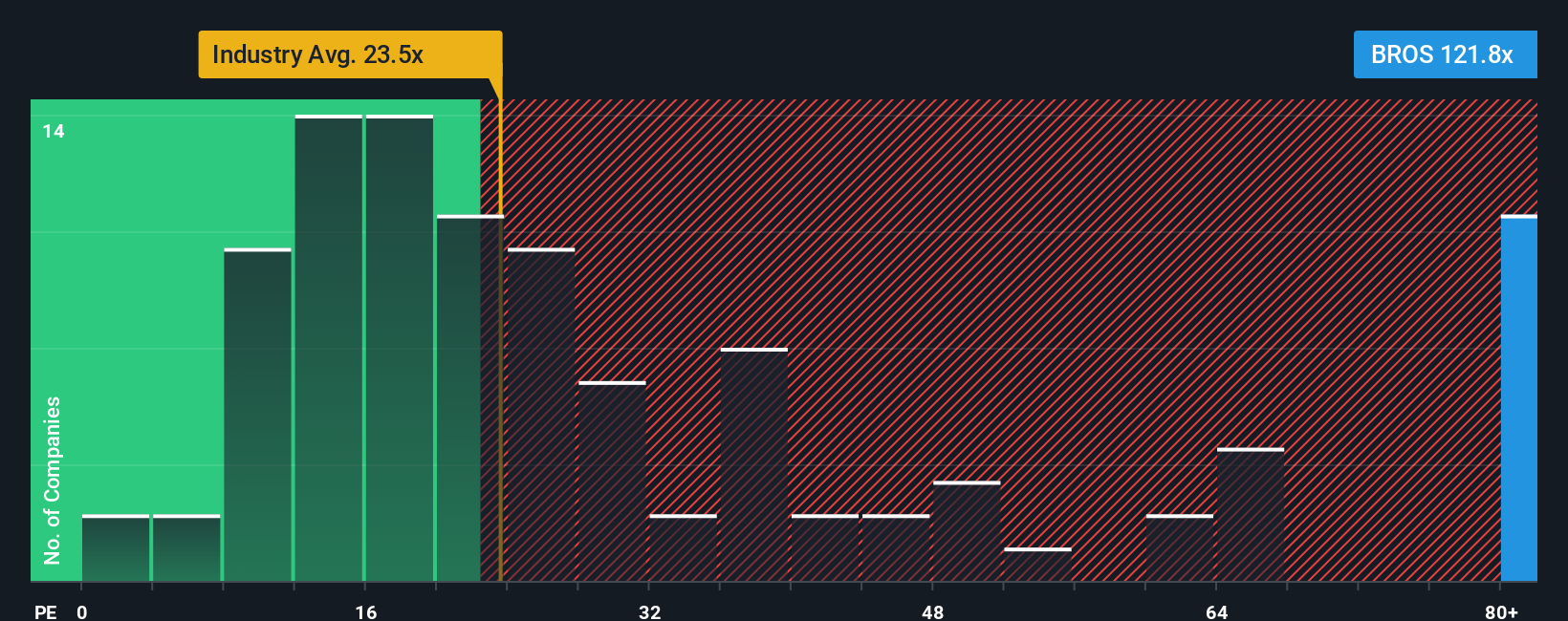

Approach 2: Dutch Bros Price vs Earnings

For a profitable company like Dutch Bros, the Price to Earnings, or PE, ratio is a useful yardstick because it links what investors are paying directly to the profits the business is generating today. In general, faster growth and lower risk justify a higher PE, while slower or more volatile earnings usually deserve a lower one.

Right now Dutch Bros trades on a hefty PE of about 125.24x, well above both the broader Hospitality industry average of roughly 21.20x and an average of close peers at around 29.85x. That signals the market is baking in very strong growth and relatively low perceived risk compared with typical operators in the space.

Simply Wall St also calculates a proprietary Fair Ratio, which estimates what a reasonable PE should be for Dutch Bros given its specific earnings growth outlook, profitability, industry, market cap and risk profile. This tends to be more informative than a simple comparison with peers, because it adjusts for how different Dutch Bros really is from the average coffee or restaurant chain. On that basis, the Fair Ratio is 34.96x, far below the current multiple, suggesting the shares look richly valued on earnings.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

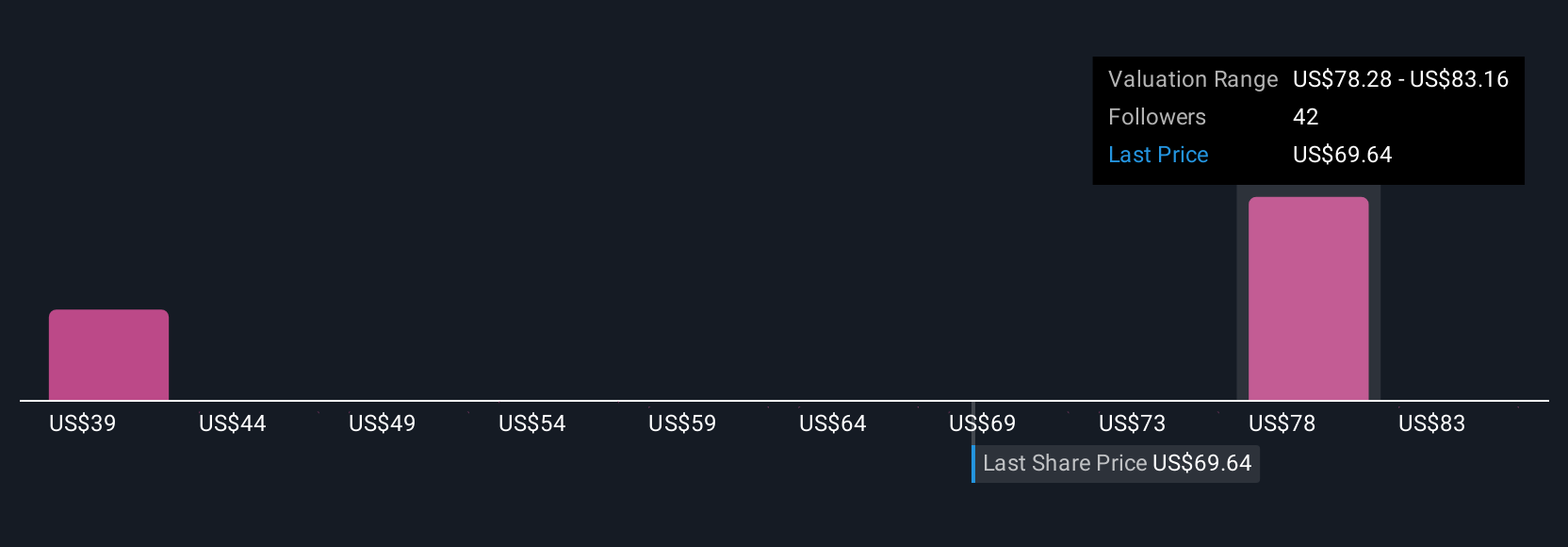

Upgrade Your Decision Making: Choose your Dutch Bros Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simple stories investors create on Simply Wall St’s Community page to connect their view of a company’s future revenues, earnings, and margins with a concrete forecast and fair value estimate. This can then be compared to today’s share price to decide whether to buy, hold, or sell, and it automatically updates as new news or earnings arrive. You can see, for example, how one Dutch Bros investor might build a bullish Narrative around aggressive store expansion, resilient demand, and a higher fair value closer to $92, while another builds a more cautious Narrative focused on margin pressure, competition, and health trends that leads to a lower fair value near $73. This makes it easy to see which story you believe and what that implies for your own decision at the current price.

Do you think there's more to the story for Dutch Bros? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com