Nasdaq

Nasdaq 华尔街日报

华尔街日报Is Clorox Offering Value After a 35% Slide and DCF Upside in 2025?

- If you have been wondering whether Clorox at around $105 is a contrarian value play or a value trap, you are not alone. That is exactly what we are going to unpack here.

- The stock is down about 2.4% over the last week, 3.6% over the past month, and a steep 35.0% year to date. This has many investors rethinking both the downside risk and the upside potential.

- Recent headlines have focused on Clorox navigating a slower demand environment in key categories and working through cost pressures, which has kept sentiment cautious. At the same time, analysts and industry observers have been highlighting the company’s brand strength and pricing power in staples, framing the current share price weakness as a possible reset rather than a structural decline.

- On our checks, Clorox scores a 4 out of 6 valuation score, suggesting the market might be undervaluing several aspects of the business. Next we will dig into what different valuation approaches say about that score, and later in the article we will look at an even better way to think about what Clorox is really worth.

Find out why Clorox's -34.9% return over the last year is lagging behind its peers.

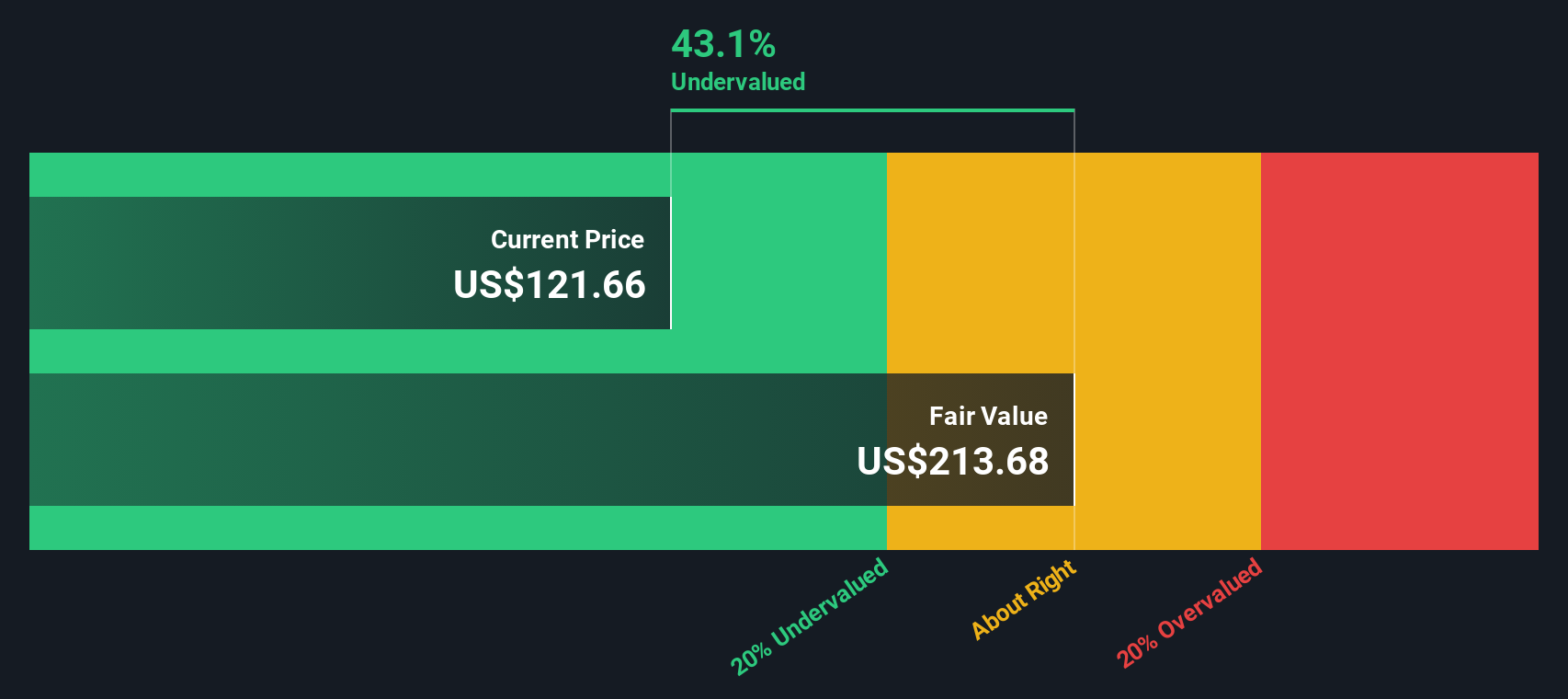

Approach 1: Clorox Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to the present.

For Clorox, the latest twelve month Free Cash Flow is about $646 million, and analysts expect this to grow steadily over time. Based on a 2 Stage Free Cash Flow to Equity model, cash flows are projected to rise toward roughly $1.1 billion by 2030, with the first few years guided by analyst forecasts and later years extrapolated using more modest growth assumptions by Simply Wall St.

When all of those future cash flows are discounted back into today’s dollars, the model arrives at an intrinsic value of about $213.56 per share. Compared with the current share price around $105, the DCF implies the stock is approximately 50.8% undervalued. This indicates the market may be overly pessimistic about Clorox’s long term cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Clorox is undervalued by 50.8%. Track this in your watchlist or portfolio, or discover 918 more undervalued stocks based on cash flows.

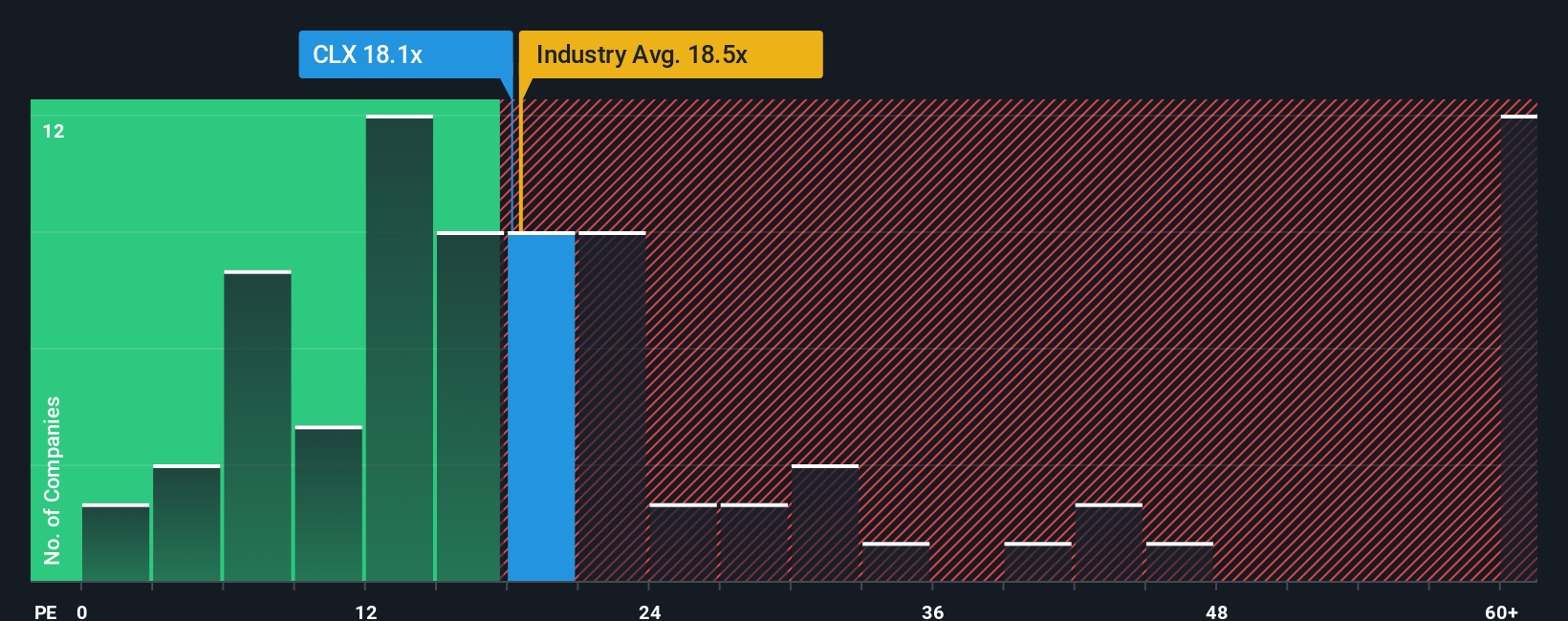

Approach 2: Clorox Price vs Earnings

For a profitable, established business like Clorox, the Price to Earnings (PE) ratio is a practical way to gauge valuation because it links what investors pay today to the company’s current earnings power. In general, faster and more reliable earnings growth justifies a higher PE, while slower or riskier earnings streams call for a lower, more conservative multiple.

Clorox currently trades on a PE of about 16.2x, which is slightly below the broader Household Products industry average of roughly 17.4x and also below the peer group average of around 20.5x. Simply Wall St’s proprietary Fair Ratio for Clorox is 16.1x. This is the PE level that would typically be expected given the company’s earnings growth profile, margins, industry positioning, size and risk characteristics.

This Fair Ratio framework is more informative than a simple peer or industry comparison because it adjusts for Clorox’s specific fundamentals instead of assuming all household product companies deserve the same multiple. With the current PE of 16.2x sitting very close to the 16.1x Fair Ratio, the market appears to be pricing Clorox almost exactly in line with what its fundamentals warrant.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

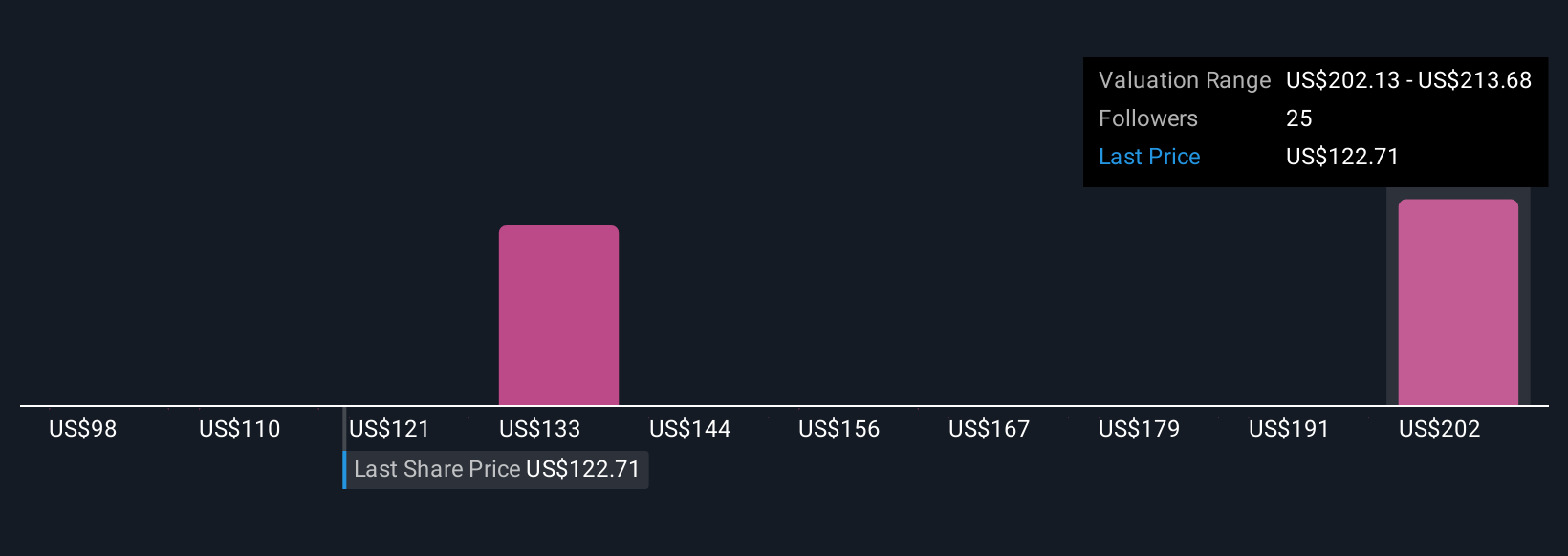

Upgrade Your Decision Making: Choose your Clorox Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your story about a company linked directly to a set of numbers, such as your assumptions for future revenue, earnings, margins and fair value.

On Simply Wall St’s Community page, Narratives are an easy, guided tool used by millions of investors to connect a company’s story to a financial forecast and then to an explicit fair value so you can quickly see whether your view says Clorox is worth more or less than today’s price.

Once you set up a Narrative, the platform continuously updates it as new information like earnings results or major news comes in. This helps you reassess whether the gap between your Fair Value and the current share price suggests it is time to buy, hold, or sell.

For example, one Clorox Narrative built around strong margin recovery, ERP efficiencies and premium product growth might justify a fair value closer to the bullish $166 target. A more cautious Narrative focused on weak category growth, pricing pressure and brand risk could land nearer the bearish $115 target.

Do you think there's more to the story for Clorox? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com