Nasdaq

Nasdaq 华尔街日报

华尔街日报Q3 Revenue and EBITDA Beat Might Change The Case For Investing In Marqeta (MQ)

- In its most recent Q3 update, Marqeta reported year-on-year revenue growth of 27.6% and outperformed analyst estimates for both revenue and EBITDA, supported by stronger-than-expected total payment volume.

- This outperformance underscores how Marqeta’s card-issuing platform can convert higher transaction activity into improving profitability metrics, an important signal for long-term scalability.

- We’ll now examine how Marqeta’s better-than-expected Q3 revenue and EBITDA performance may influence its existing investment narrative and outlook.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 36 companies in the world exploring or producing it. Find the list for free.

Marqeta Investment Narrative Recap

To own Marqeta, you need to believe its card issuing platform can scale efficiently as digital payment volumes grow, while customer concentration and competition remain manageable. The Q3 beat on revenue and EBITDA reinforces the near term catalyst of profit improvement from higher transaction volumes, but it does not meaningfully change the key risk that a major client could still reduce or shift its business.

The Klarna Card expansion into 15 new European markets, supported by Visa’s Flexible Credential technology, is particularly relevant here, as it highlights how new and existing partners can drive additional total payment volume on Marqeta’s rails. If these newer relationships deepen and diversify revenue, they could gradually offset reliance on legacy anchor customers and influence how investors weigh the recent Q3 upside.

Yet, while recent results look encouraging, investors should be aware that customer concentration risk remains...

Read the full narrative on Marqeta (it's free!)

Marqeta's narrative projects $900.6 million revenue and $47.9 million earnings by 2028.

Uncover how Marqeta's forecasts yield a $6.18 fair value, a 31% upside to its current price.

Exploring Other Perspectives

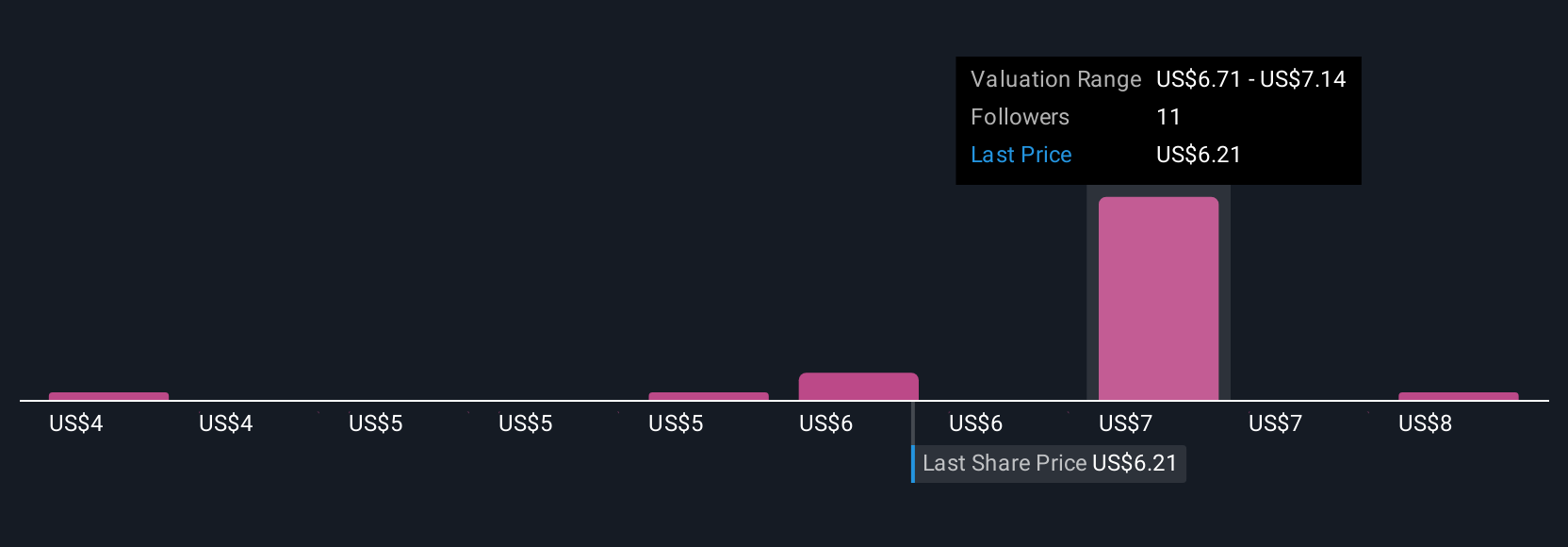

Six fair value estimates from the Simply Wall St Community span US$3.70 to US$8.00, showing how differently investors can view Marqeta’s potential. When you set that against Marqeta’s reliance on a few key customers, it underlines why you might want to compare several viewpoints before deciding how much of its recent progress feels sustainable.

Explore 6 other fair value estimates on Marqeta - why the stock might be worth 22% less than the current price!

Build Your Own Marqeta Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find companies with promising cash flow potential yet trading below their fair value.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com