Nasdaq

Nasdaq 华尔街日报

华尔街日报Does CEC Deal And Data Center Demand Shift The Bull Case For Sterling Infrastructure (STRL)?

- Sterling Infrastructure recently highlighted strong demand across mission-critical markets such as data centers, e-commerce, and manufacturing, alongside its completed acquisition of CEC Facilities Group, which enhances its electrical services capabilities and supports longer-term project visibility through an expanded backlog and pipeline.

- An interesting angle for investors is how CEC’s integration could shift Sterling’s earnings mix toward higher-value, electrical-heavy work with potential for improved margins and deeper, multi-year customer relationships.

- We’ll now assess how the CEC acquisition, and its potential to lift margins via more integrated services, may influence Sterling’s existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Sterling Infrastructure Investment Narrative Recap

To own Sterling Infrastructure today, you need to believe its focus on mission-critical projects like data centers and advanced manufacturing can support durable, high-margin growth, and that CEC’s integration will deepen that advantage. The recent surge in demand and stronger backlog visibility appear supportive of the near term earnings trajectory, while the biggest risk now is whether margins and project execution can keep pace with elevated expectations after a 90% year to date share price move.

Among recent announcements, the expanded US$400 million share repurchase program stands out alongside the CEC acquisition, as it signals confidence in cash generation while the business shifts toward more complex, higher-value E-Infrastructure work. For investors, that combination of disciplined capital returns and a growing, multi-year backlog in mission-critical markets ties directly into the main catalyst: continued proof that Sterling can convert its order book into sustained, high quality earnings.

Yet, despite the strong backlog and heightened optimism, investors should also be aware of how sensitive the story is to...

Read the full narrative on Sterling Infrastructure (it's free!)

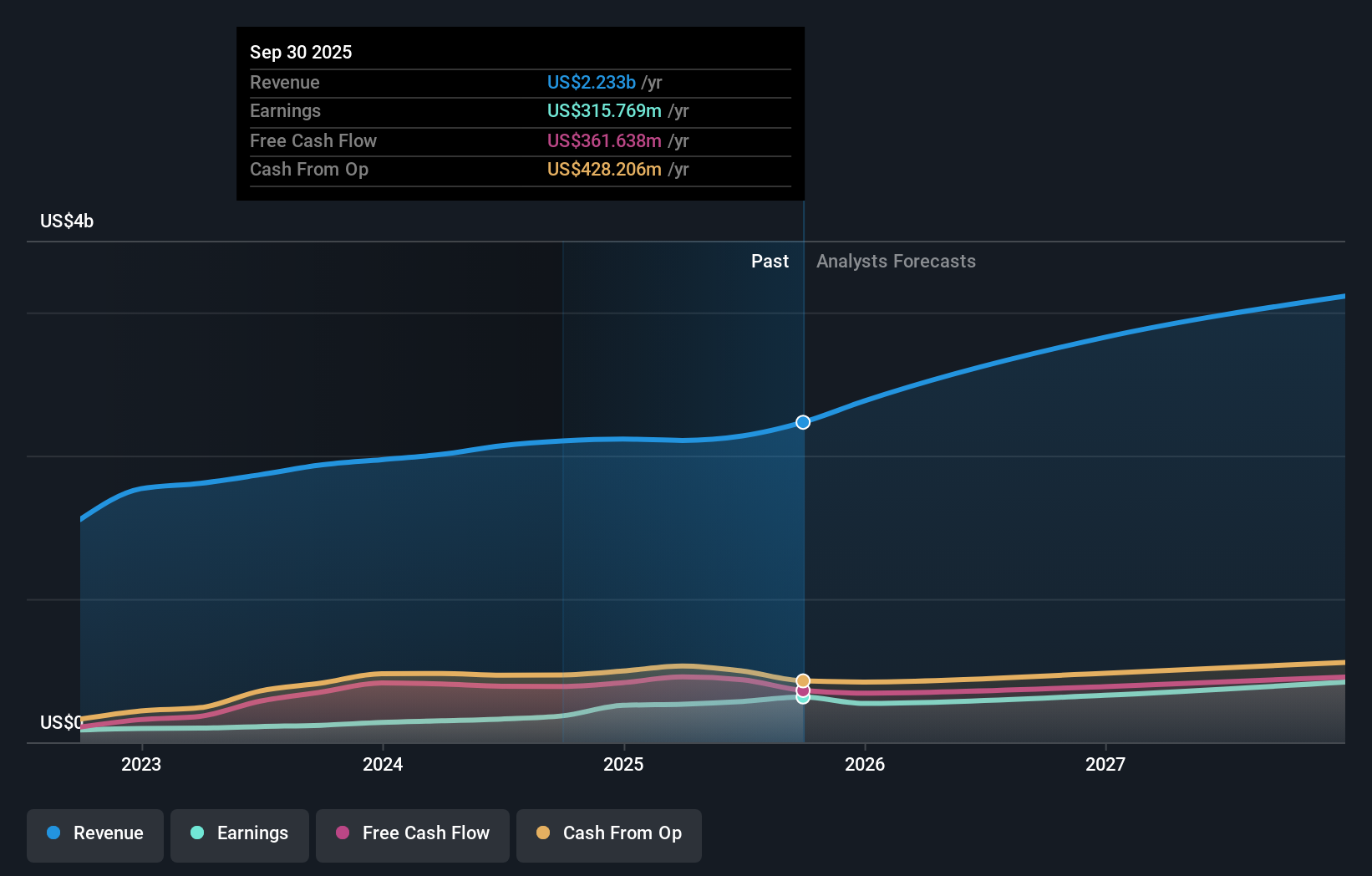

Sterling Infrastructure's narrative projects $2.6 billion revenue and $276.4 million earnings by 2028.

Uncover how Sterling Infrastructure's forecasts yield a $453.33 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span roughly US$114 to US$453 per share, showing how far apart individual views can be. When you set that spread against the importance of Sterling’s growing E Infrastructure backlog as a key earnings driver, it underlines why checking several viewpoints before forming an opinion on the company’s prospects can be so valuable.

Explore 6 other fair value estimates on Sterling Infrastructure - why the stock might be worth less than half the current price!

Build Your Own Sterling Infrastructure Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sterling Infrastructure research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Sterling Infrastructure research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sterling Infrastructure's overall financial health at a glance.

No Opportunity In Sterling Infrastructure?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com