Nasdaq

Nasdaq 华尔街日报

华尔街日报Is Amentum Holdings Attractively Priced After Its Recent 28.2% Share Price Surge?

- Wondering if Amentum Holdings at around $28.72 is a bargain or a value trap? You are not alone. This stock has been catching the eye of investors looking for mispriced opportunities.

- After a sharp 28.2% jump over the last month, the share price has cooled with a 4.3% pullback in the past week. It still sits up 32.6% year to date and 18.3% over the past year.

- Recent headlines have focused on Amentum's positioning in government and mission critical services, with investors weighing how its long term contracts and defense exposure might support more durable cash flows. There has also been growing discussion about how shifting government priorities and modernization programs could reshape its pipeline and risk profile.

- Right now, Amentum scores just 2/6 on our valuation checks, which indicates that some metrics hint at undervaluation while others flash caution. Next, we will examine the different valuation approaches behind that score and then look at an additional way to think about what the stock might really be worth.

Amentum Holdings scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Amentum Holdings Discounted Cash Flow (DCF) Analysis

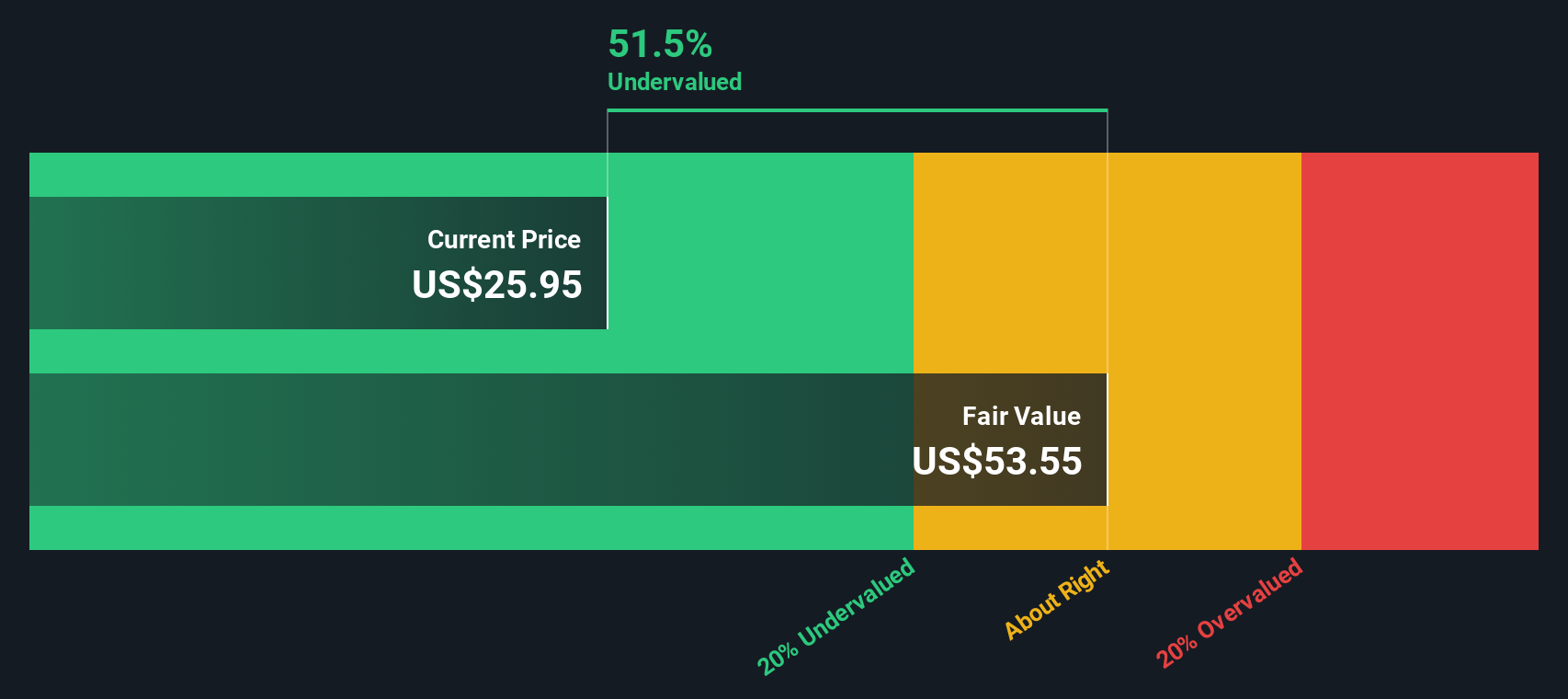

A Discounted Cash Flow model estimates what a business is worth by projecting its future cash flows and then discounting those back to today in dollar terms. For Amentum Holdings, the model starts with last twelve month free cash flow of about $519.4 million and then applies a 2 stage Free Cash Flow to Equity approach.

Analysts provide detailed forecasts for the next few years, with free cash flow expected to rise to roughly $557.6 million in 2026 and $657.9 million in 2027, before reaching around $756.1 million by 2028. Beyond that point, Simply Wall St extrapolates the trend out to 2035, where projected free cash flow climbs to roughly $1.15 billion, with each year discounted back to reflect risk and the time value of money.

Adding up these discounted cash flows results in an estimated intrinsic value of about $66.96 per share. Compared with the recent share price near $28.72, the DCF suggests Amentum may be around 57.1% undervalued based on current assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Amentum Holdings is undervalued by 57.1%. Track this in your watchlist or portfolio, or discover 932 more undervalued stocks based on cash flows.

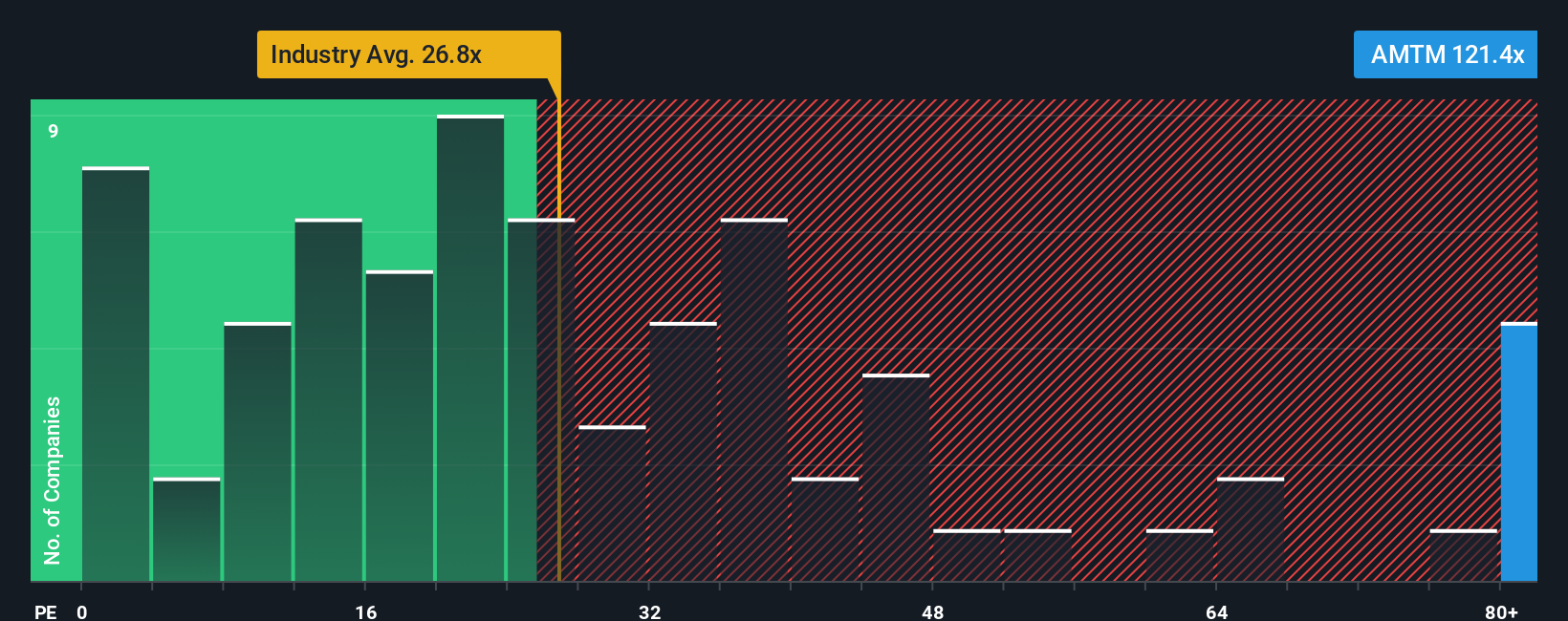

Approach 2: Amentum Holdings Price vs Earnings

For profitable companies like Amentum Holdings, the price to earnings (PE) ratio is a useful way to gauge how much investors are willing to pay today for each dollar of current earnings. In general, faster growing, less risky businesses can justify a higher PE, while slower growth or higher uncertainty usually calls for a lower, more conservative multiple.

Amentum currently trades at about 106.0x earnings, which is far richer than the Professional Services industry average of roughly 24.2x and also well above the peer group average near 20.2x. At face value, that large premium might suggest the stock is priced for very strong growth or unusually resilient earnings.

Simply Wall St also calculates a proprietary Fair Ratio for Amentum of around 43.4x, which reflects what the PE should be given its earnings growth profile, margins, industry, market cap and risk factors. This Fair Ratio is more informative than a simple comparison with peers or the sector, because it explicitly incorporates the company specific fundamentals that drive what a reasonable multiple should be. With Amentum trading at 106.0x versus a Fair Ratio of 43.4x, the stock screens as materially overvalued on this measure.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

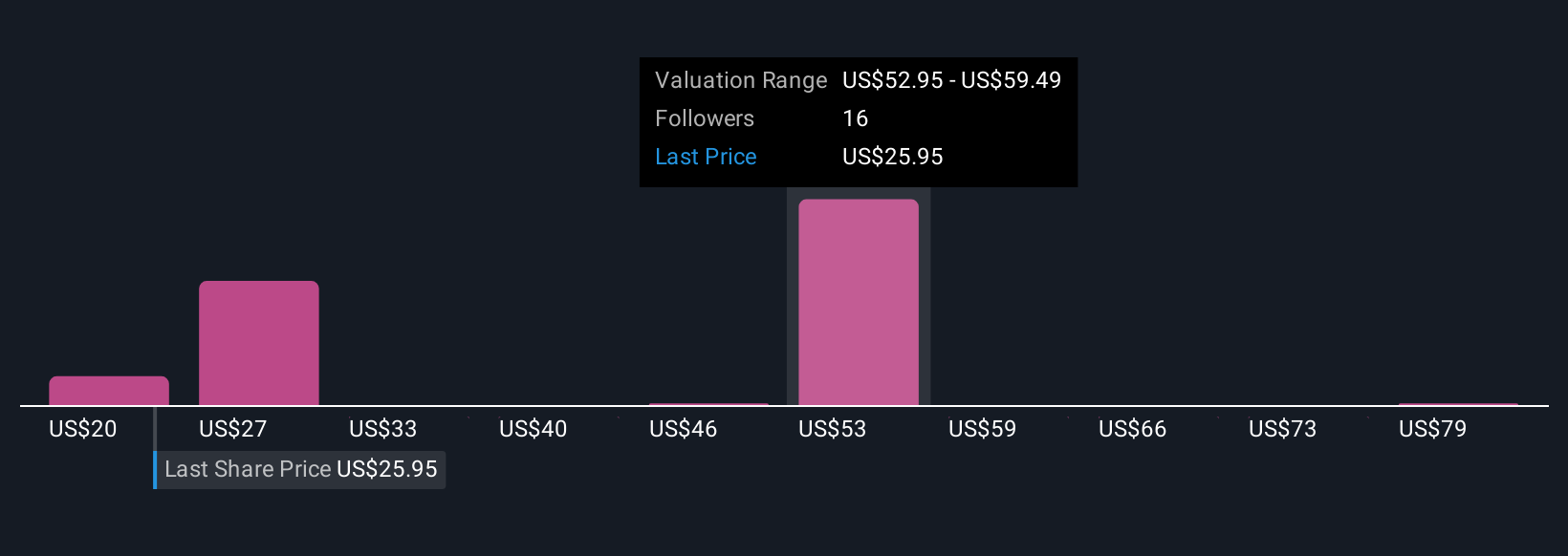

Upgrade Your Decision Making: Choose your Amentum Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a smarter, more flexible way to invest that goes beyond static ratios. A Narrative is simply your story about a company, where you spell out what you believe about its future revenue, earnings and margins, and link that story directly to a financial forecast and a fair value estimate. On Simply Wall St, millions of investors use Narratives on the Community page to turn their views into numbers, so they can easily compare a company’s Fair Value to its current share price and decide whether it looks like a buy, hold or sell. Because Narratives are updated dynamically when new information arrives, such as earnings results or major contract wins, your fair value stays aligned with the latest data rather than going stale. For Amentum Holdings, for example, one investor Narrative might assume accelerating government contract growth and strong margin expansion, while another might build in slower contract awards and tighter margins, leading to very different fair values and decisions.

Do you think there's more to the story for Amentum Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com