Nasdaq

Nasdaq 华尔街日报

华尔街日报Did ITOCHU's (TSE:8001) Live Oak E‑Methane Role Just Recast Its Energy Transition Story?

- TotalEnergies, TES, Osaka Gas, Toho Gas, and ITOCHU recently signed a Joint Development and Operating Agreement giving the Japanese firms a combined 33.3% stake in the Live Oak e-methane project in Nebraska, which targets 250 MW of electrolysis and 75 ktpa of methanation capacity with commercial operations planned by 2030.

- The deal highlights ITOCHU’s role as coordinator among Japanese partners to secure carbon-neutral gas supplies for Japan using existing LNG infrastructure and biogenic CO2 from U.S. bioethanol plants.

- We’ll now assess how ITOCHU’s coordinating role in Live Oak’s large-scale e-methane export project may reshape its investment narrative.

We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

ITOCHU Investment Narrative Recap

To own ITOCHU, you need to believe it can steadily compound earnings from a diversified portfolio while managing exposure to resource cycles, currency swings, and one off gains. The Live Oak e methane stake looks incremental in the near term, but it slightly strengthens the case that energy transition projects can offset some future volatility in traditional resource businesses.

Among recent announcements, the July to September 2025 share buyback tranche, with ¥58,220.68 million spent to repurchase about 0.51% of shares, most directly intersects with current catalysts. Together with Live Oak, it frames a story of ITOCHU trying to balance long term decarbonization investments with capital returns, even as questions linger over how sustainable earnings will be without one off gains.

Yet against this backdrop, the risk that earnings rely too heavily on one off gains is something investors should be aware of as...

Read the full narrative on ITOCHU (it's free!)

ITOCHU’s narrative projects ¥16,471.1 billion in revenue and ¥981.5 billion in earnings by 2028.

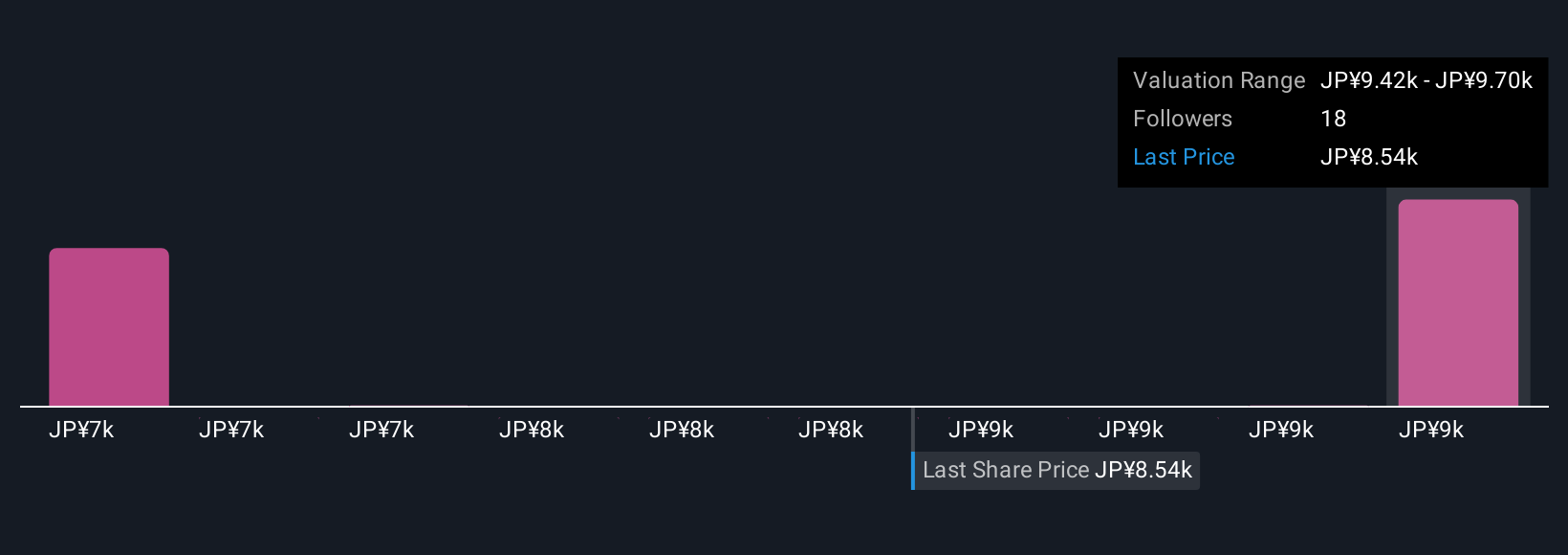

Uncover how ITOCHU's forecasts yield a ¥9770 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span roughly ¥7,444 to ¥9,770, underscoring how far apart individual views on ITOCHU can be. Set against concerns about earnings quality and reliance on one off gains, this spread invites you to compare multiple scenarios for how resilient profits might be over time.

Explore 3 other fair value estimates on ITOCHU - why the stock might be worth as much as 6% more than the current price!

Build Your Own ITOCHU Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ITOCHU research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ITOCHU research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ITOCHU's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com