- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

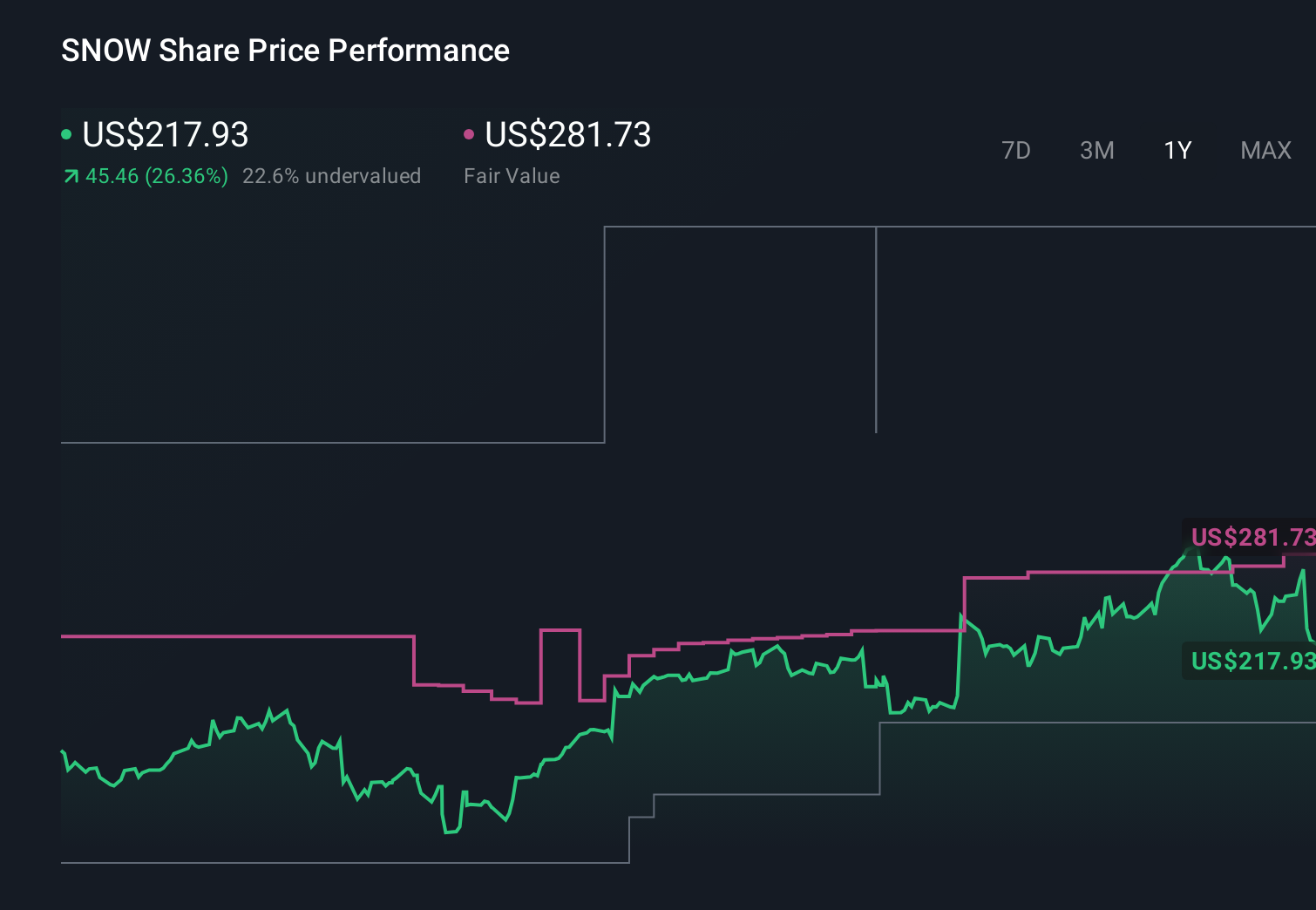

Do Snowflake’s (SNOW) New AI Data Cloud Integrations Clarify or Complicate Its Governance Narrative?

- In recent days, partners including AVEVA, Dataiku, Tealium, Bedrock Data, Valid Systems, ManageMy and Zeta Global have announced new integrations and open-source collaborations built on Snowflake’s AI Data Cloud, expanding how enterprises unify, govern and activate data for AI agents and real-time decisioning across multiple regulated industries.

- At the same time, a shareholder proposal seeking a shift to majority voting for directors and Snowflake’s opposition to it highlight ongoing debates over governance practices just as the company’s AI ecosystem and industrial, financial and marketing use cases broaden.

- Against this backdrop, we’ll examine how Snowflake’s expanding partner-built AI agents and zero-copy integrations could influence its existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Snowflake Investment Narrative Recap

To own Snowflake, you need to believe its AI Data Cloud will stay central to how enterprises run data and AI workloads, even as competition and migration tailwinds evolve. In the near term, the key swing factor is whether newer AI products and partner-built agents convert into meaningful, sustainable consumption; the biggest risk remains that AI-native or bundled cloud rivals compress Snowflake’s pricing and growth. The latest partner and governance news does not materially change that near term setup.

Among the recent updates, AVEVA’s zero copy integration with Snowflake stands out for how directly it speaks to the AI workload thesis. It shows Snowflake’s platform being used to unify operational and enterprise data for governed industrial AI agents in heavily regulated sectors, which aligns closely with the idea that more real time, mission critical workloads can build on Snowflake rather than on separate AI-native stacks.

Yet beneath this AI partner momentum, there is a governance and profitability story investors should be aware of...

Read the full narrative on Snowflake (it's free!)

Snowflake's narrative projects $9.0 billion revenue and $689.7 million earnings by 2029. This requires 24.5% yearly revenue growth and about a $2.0 billion earnings increase from -$1.3 billion today.

Uncover how Snowflake's forecasts yield a $232.74 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$8.8 billion by 2029 and still no profits, so while recent AI tie ups may pressure those views, you should recognize that opinions differ widely and that more bearish voices see rising AI native rivals and compliance costs as real headwinds.

Explore 13 other fair value estimates on Snowflake - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Snowflake research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Snowflake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Snowflake's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com