- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Did Zacks’ Upgrade and North Reef’s Stake Just Shift Ameris Bancorp’s (ABCB) Investment Narrative?

- Earlier in 2026, North Reef Capital disclosed a passive 5.04% stake in Ameris Bancorp, while Zacks recently upgraded the bank’s shares to a Rank #2, reflecting an improved earnings outlook and coinciding with supportive commentary from KBW.

- Taken together, the Zacks upgrade and continued bullish analyst views point to rising confidence in Ameris Bancorp’s earnings trajectory and business fundamentals.

- Next, we’ll examine how the Zacks Rank upgrade, signaling improving earnings estimates, may influence Ameris Bancorp’s existing investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Ameris Bancorp Investment Narrative Recap

To own Ameris Bancorp, you need to believe the bank can keep expanding profitably in its core Southeastern markets while managing deposit costs, credit quality and regional concentration. The Zacks Rank upgrade and KBW’s supportive stance reinforce the current earnings story, but they do not materially change the key near term catalyst, which remains execution on disciplined loan and deposit growth, or the main risk around margin pressure from tougher competition for funding.

The most relevant recent development here is the Zacks Rank upgrade to #2, which reflects rising earnings estimates. That aligns with Ameris’s recent results, where net interest income and earnings have grown, and supports the idea that the market is gaining confidence in its fundamentals, even as investors continue to watch loan growth in more cyclical segments and the impact of interest rate moves on net interest margins.

But while sentiment has improved, investors should be aware that the growing competition for deposits and loans could...

Read the full narrative on Ameris Bancorp (it's free!)

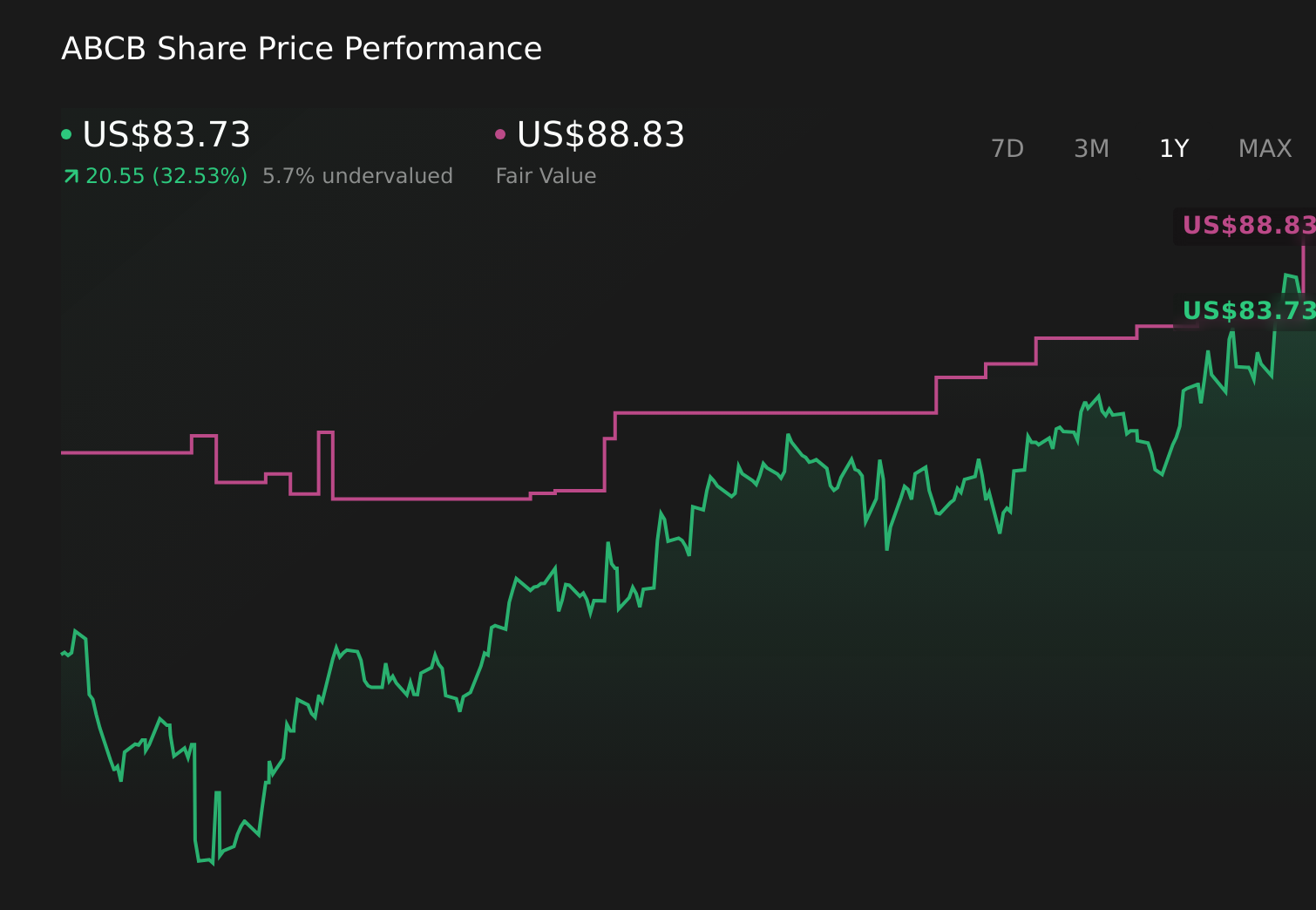

Ameris Bancorp's narrative projects $1.5 billion revenue and $492.5 million earnings by 2029. This requires 9.6% yearly revenue growth and a roughly $57.8 million earnings increase from $434.7 million today.

Uncover how Ameris Bancorp's forecasts yield a $89.93 fair value, a 9% upside to its current price.

Exploring Other Perspectives

One valuation submitted by the Simply Wall St Community places Ameris Bancorp’s fair value at US$89.93, underlining how differently individual investors can view the same bank. You should weigh that against the risk that rising competition for deposits and loans may tighten margins and influence how Ameris’s recent earnings momentum translates into future performance.

Explore another fair value estimate on Ameris Bancorp - why the stock might be worth as much as 9% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ameris Bancorp research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Ameris Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ameris Bancorp's overall financial health at a glance.

No Opportunity In Ameris Bancorp?

Our top stock finds are flying under the radar-for now. Get in early:

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com