- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

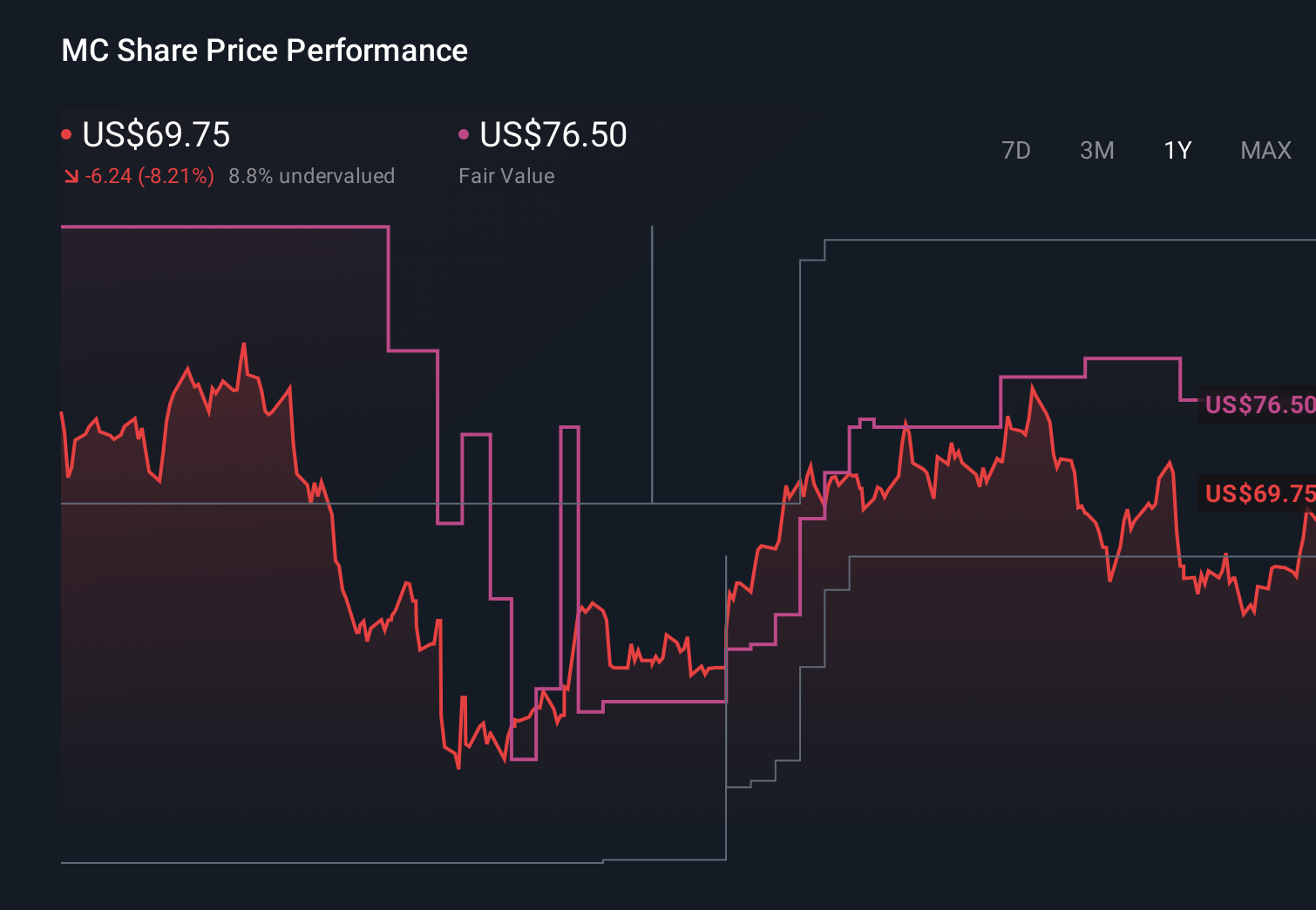

Moelis (MC) Is Down 8.9% After Earnings Dip And Capital Returns Update Has The Bull Case Changed?

- Moelis & Company recently reported first-quarter 2026 net income of US$38.43 million, down from US$50.27 million a year earlier, while also confirming a quarterly dividend of US$0.65 per share payable on June 18, 2026.

- Alongside these results, Moelis completed two share repurchase tranches totaling nearly US$53.64 million and filed a US$38.70 million employee stock ownership plan-related shelf registration for Class A common stock, highlighting an active approach to capital returns and equity issuance.

- Against this backdrop, we’ll explore how the affirmed US$0.65 dividend and recent buybacks reshape Moelis’s previously outlined investment narrative.

Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

Moelis Investment Narrative Recap

To own Moelis today, you need to be comfortable with a transaction-heavy advisory model that can swing with deal activity, while trusting that expansion into areas like Private Capital Advisory and technology can offset that volatility over time. The Q1 2026 earnings dip to US$38.43 million does not appear to change the near term catalyst of converting a strong mandate pipeline into fees, but it does keep margin pressure and compensation costs firmly in focus as the key risk.

The most relevant recent development is the combination of ongoing buybacks and the new US$38.70 million ESOP related shelf for Class A stock. On one hand, Moelis has just completed around US$53.64 million of repurchases in early 2026, which can support per share metrics if deal activity holds up. On the other, the ESOP filing points to continued equity issuance alongside capital returns, which matters when you are weighing how much earnings growth will actually accrue to each share.

Yet against this backdrop of steady dividends and active buybacks, investors should still consider how exposed Moelis remains to sudden slowdowns in transaction volumes and...

Read the full narrative on Moelis (it's free!)

Moelis' narrative projects $2.1 billion revenue and $381.7 million earnings by 2028. This requires 15.3% yearly revenue growth and a $183.6 million earnings increase from $198.1 million today.

Uncover how Moelis' forecasts yield a $76.50 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts see a much harsher setup for Moelis than the consensus, even before this latest quarter and capital actions are digested. While the baseline view leans on expansion into PCA and tech to support fees, the bearish cohort was already flagging that rising regulatory complexity could slow deals and lift costs, and expected earnings of about US$462.9 million by 2029 only if margins improved from here. That gap in expectations shows how differently you can read the same business and why it can be useful to compare several narratives side by side as new information arrives.

Explore 3 other fair value estimates on Moelis - why the stock might be worth as much as 42% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Moelis research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com