- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Lakeland Financial (LKFN) Valuation After Record Q1 Earnings Beat And Dividend Increase

Lakeland Financial (LKFN) drew fresh attention after reporting record first quarter net income of US$26.5 million, stronger than expected earnings, a higher dividend, and increased net charge offs compared with the same period last year.

See our latest analysis for Lakeland Financial.

The earnings beat, higher dividend and completion of a multi year buyback have been reflected in a 9.02% 1 month share price return. The 3 year total shareholder return of 43.75% points to momentum that has built over time.

If you are looking for similar ideas beyond regional banks, this is a good moment to widen your search with 1 top founder-led companies

With the share price up over the past month, record earnings on the table, a higher dividend, and shares trading about 6% below the average analyst target, the question is simple: is there still value here, or is the market already pricing in future growth?

Preferred P/E of 14x: Is it justified?

Lakeland Financial shares last closed at $61.67, and on a P/E of 14x they change hands at a higher earnings multiple than many US banks, despite trading below some intrinsic value estimates.

The P/E ratio compares the current share price to earnings per share, so it effectively shows how much investors are paying for each dollar of earnings. For a regional bank with high quality earnings and a long operating history, this is a common way for the market to weigh profit durability and income potential against sector peers.

Here, the picture is mixed. On one side, LKFN is described as trading at a 38.3% discount to an estimated fair value based on the SWS DCF model, and it is also considered good value relative to a peer average P/E of 24.5x. On the other side, the shares are labelled expensive compared with the US Banks industry average P/E of 11.5x and the estimated fair P/E ratio of 9.9x, a level the market could move towards if enthusiasm for the stock cools.

This leaves investors weighing a premium to sector P/E and fair ratio levels against a discount to one intrinsic cash flow estimate and to higher valued peers. This combination points to a valuation that is neither obviously stretched nor clearly cheap when viewed through a single lens.

Explore the SWS fair ratio for Lakeland Financial

Result: Price-to-Earnings of 14x (ABOUT RIGHT)

However, you still need to watch for rising net charge offs and any shift in analyst sentiment that could pressure the current P/E premium and share price.

Find out about the key risks to this Lakeland Financial narrative.

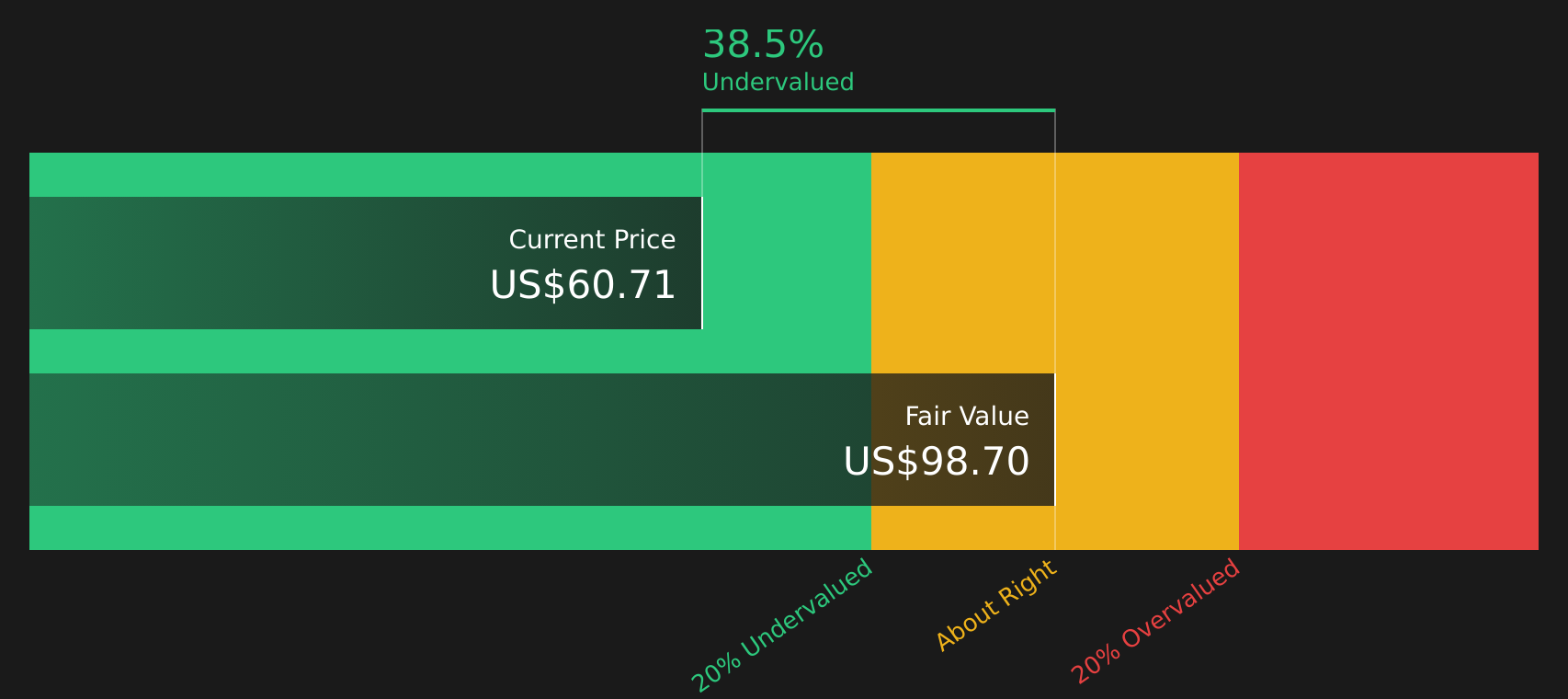

Another View: Cash Flow Tells a Different Story

While the 14x P/E suggests the shares sit somewhere in the middle ground on earnings, the SWS DCF model paints a contrasting picture. With an estimated future cash flow value of $99.92 per share versus a market price of $61.67, the model points to Lakeland Financial trading about 38.3% below that estimate. If earnings say one thing but cash flows say another, which lens should you rely on when judging value?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lakeland Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and sentiment, this is the time to look through the numbers yourself and decide what they add up to for you. To help frame that view, take a closer look at the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Lakeland Financial has sharpened your thinking, do not stop here. Broaden your watchlist with structured ideas so you are ready when opportunities line up.

- Start hunting for companies that combine price and quality by scanning the 53 high quality undervalued stocks and see which ones deserve a closer look.

- Strengthen the income side of your portfolio by reviewing the 14 dividend fortresses that could help support more consistent cash flows.

- Focus on resilience by filtering for the 1 resilient stocks with low risk scores and keep an eye on businesses that may hold up better when conditions get tougher.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com