- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Ardent Health (ARDT) Valuation After Shareholder Rights Probe and Accounting Adjustments

Ardent Health (ARDT) is back in the spotlight after law firm Johnson Fistel launched a shareholder rights investigation, following disclosures of a $43 million revenue reduction and a $54 million boost to professional liability reserves.

See our latest analysis for Ardent Health.

The latest investigation comes after a sharp reset in sentiment. The 30 day share price return of negative 38.96 percent and year to date share price return of negative 47.83 percent have left longer term total shareholder returns similarly under pressure, suggesting momentum is still fading despite Ardent's underlying revenue and earnings growth.

If this kind of volatility has you rethinking your watchlist, it could be worth comparing Ardent's profile with other hospital and care providers using our healthcare stocks as a fresh set of ideas.

With the stock now trading well below analyst targets despite solid top line and earnings growth, the key question becomes: is Ardent Health meaningfully undervalued, or is the market already pricing in its long term risks and future growth?

Most Popular Narrative: 37% Undervalued

With Ardent Health last closing at $8.79 against a narrative fair value near $13.96, the gap points to sizable upside if forecasts prove accurate.

The analysts have a consensus price target of $19.273 for Ardent Health based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $23.0, and the most bearish reporting a price target of just $12.0.

Want to see what kind of revenue runway, margin rebuild, and future earnings power could justify that valuation gap? The narrative’s financial roadmap might surprise you.

Result: Fair Value of $13.96 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, several risks could derail that upside, including heavier than expected Medicaid funding cuts and prolonged margin pressure from rising labor costs and payer denials.

Find out about the key risks to this Ardent Health narrative.

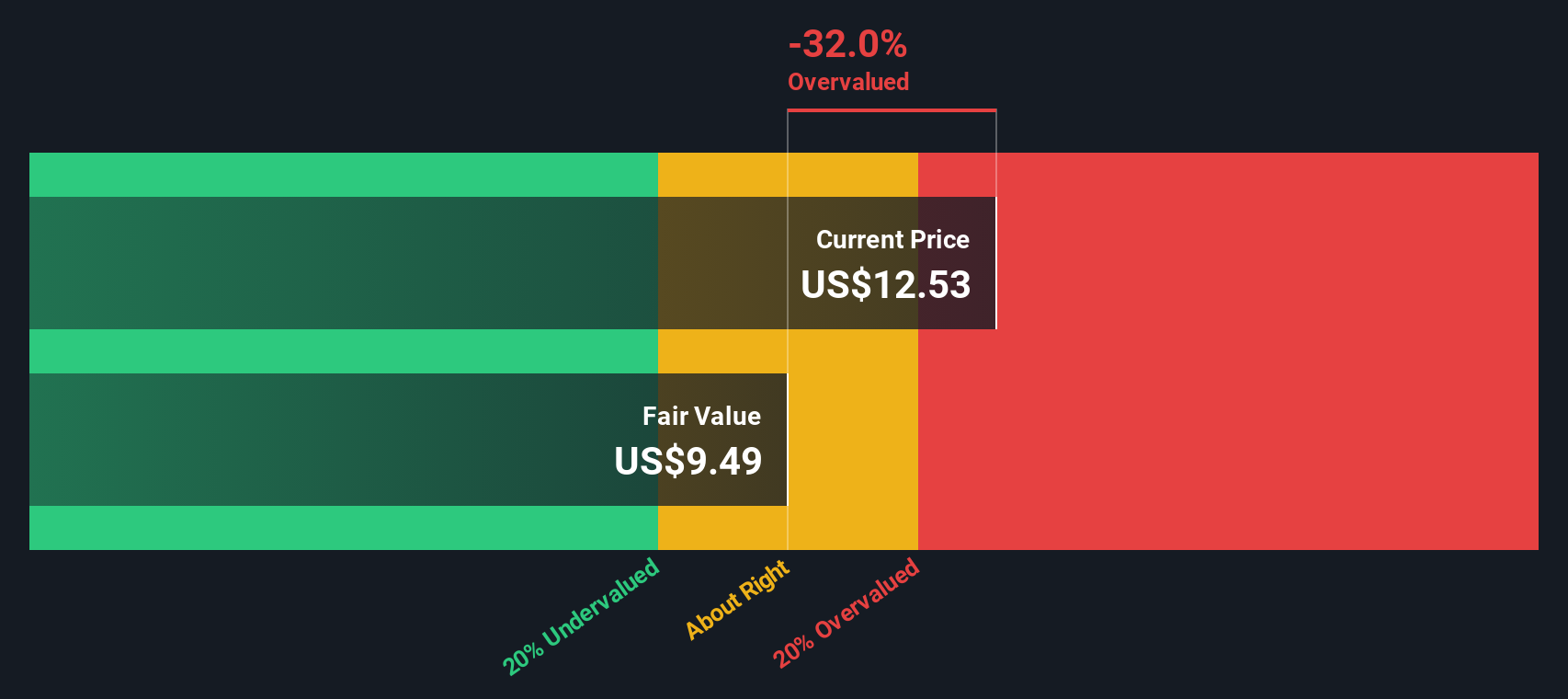

Another View: Cash Flows Paint a Tougher Picture

While analyst targets and narratives suggest upside, our DCF model is more cautious. Based on those cash flow assumptions, Ardent’s fair value sits near $7.02, below the current $8.79 price, which implies the stock may actually be overvalued today. Which story do you trust more: sentiment or cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ardent Health for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 903 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Ardent Health Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a tailored narrative in just minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Ardent Health.

Looking for more investment ideas?

Do not stop with Ardent. Put Simply Wall Street’s powerful screeners to work now and uncover opportunities that other investors may only notice months from today.

- Target powerful income potential by reviewing these 15 dividend stocks with yields > 3% that can help anchor your portfolio with reliable cash returns.

- Capitalize on structural growth trends through these 27 AI penny stocks at the forefront of automation, data analytics, and machine learning.

- Position yourself ahead of deep value hunters with these 903 undervalued stocks based on cash flows that look attractively priced relative to their cash flow prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com